Crypto 2024 SOTU Summary — State of Frontier Assets

(Any views expressed in the below are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

Here’s a recap summary of the 8DC Crypto State of the Union Event we hosted recently in Utah.

Where Brad explored Bitcoin and Foundational Assets, I’m going to focus on the other 9,999+ coins on CoinMarketCap. In thinking about Frontier Assets, I wanted to start with a couple helpful frameworks for thinking about how value accrues to crypto assets.

Valuing anything is part science, part art. Valuing crypto projects can be scary — is this a scam? Is this valuation too high? Where are the cash flows?

One note throughout this presentation, is that you’ll notice some sky high valuations. Projects that are still finding product market fit that have $5B+ market caps. Don’t let these scare you.

Crypto is an exponential technology, and since we have a global 24/7 price scoreboard it makes sense that the valuations will also be exponential. We believe this asset class is on it’s way from $1T to $10T, so even billion dollar projects have ample room for growth.

You don’t have to buy the meme coin for pennies, or get in on the early stage valuation at $1M. Crypto has democratized VC investing. Last cycle, you could have bought Binance (BNB) at a $1B valuation and still seen a 100x. There are compelling opportunities for the right assets even when valuations seem high.

One way to think about valuing tokens is using a framework that consists of Current Utility Value (UV) and Discounted Expected Utility Value or Speculative Value (SV). This is as true for $AAPL as it is for $SOL. With a public equity like $AAPL perhaps you’ll do some analysis on cashflows and earnings and determine the UV. Then there will be some amount of modeling and guesswork done to determine what utility is expected into the future — this is the Speculative Value.

This same process happens with cryptoassets, but perhaps a bit more exterme because the technology is early and the promise of what crypto can be bring is so unknown and anticipated. But similar to valuing stocks, we can take a token like $ETH and look at transaction and fee revenue, inflation and token burn schedules, etc. and determine current UV. We then look at technological developments, market growth, etc. to make guesses at the future — this is SV.

It’s important to note, that the amount of SV changes throughout a market cycle. In Peak Bear, fear is rampant, and little speculative value exists, most of the token price is comprised of UV. In Peak Bull — it’s the opposite. Everyone disregards fundamentals, greed abounds, and most of the token price is comprised of SV.

Here’s a similar framework that applies this concept but across the broader market. Over time, we’re strong believers in this green line — that crypto and blockchain technology will continue to improve, that communities will grow, and it’s impact on the world will be more and more powerful.

But, we’re opportunistic investors that try to take advantage of the red line. When Peak Bull is in full swing, SV is rampant, and everyone thinks crypto will solve world peace, it’s the time to be prudent, patient and take some profits. During Peak Bear, the opposite is true.

So, a lot of playing with Frontier Assets, is understanding these two frameworks, and where we are in any given cycle.

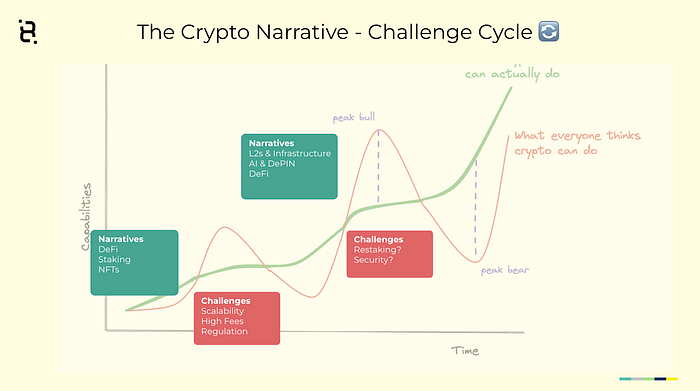

Furthering this concept, I’m going to focus today on a few narratives that we feel are important during this cycle. Each cycle brings with it certain narratives that drive interest and speculation. These narratives ultimately end up getting overtraded, things blow up, which then turn into challenges. During the bear market, builders do what they do best and build to solve these challenges, and the new tech that emerges leads to new narratives for the next cycle.

There are many narratives we could highlight as relevant to this cycle, but today we’ll focus on: L2s and Infrastructure, AI & DePIN, and DeFi.

It’s important to note that we’re still very much in the road building phase in crypto. Everyone is looking for crypto’s killer app — it will come. But just as a comparison… what do we most commonly use the internet for today? Video streaming. Whether netflix, or tiktok or cat videos on youtube. This tech wasn’t even ready for ~20 years after the advent of the WWW.

So, as we go through this, if you don’t understand monolithic vs modular blockchains, or zero-knowledge proofs. It’s fine, 99% of the world doesn’t understand all the infrastructure that exists underneath their facebook app.

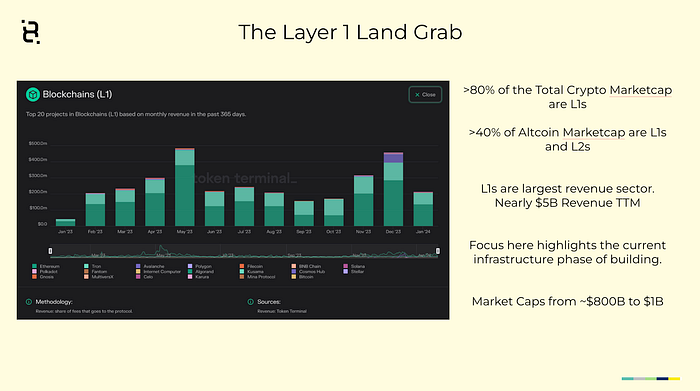

This “road building phase” is evidenced in how much of the total crypto marketcap are L1s. We’re still in the Land Grab phase of this new “crypto world” where everyone wants to claim the land so they can get a piece of all the action that happens on top of it.

From a utility value perspective, impressive to note that L1s generated $5B in Fees Revenue over the last twelve months. Clearly there is a demand for block space.

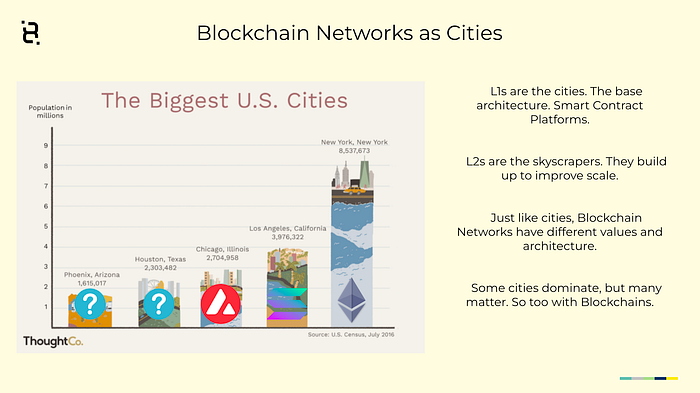

To understand what L1s and L2s are, we can use the analogy of a city. Cities are constrained by a certain geographical region. People come to a city seeking financial gain, social interaction, etc. People and businesses build in the city which then attracts more people to come and so on. Eventually the city is crammed, and they have to figure out how to accomodate more people who want to come. One option is to build up — skyscrapers. Cities are L1s. Skyscrapers are L2s. L2s improve the capacity of a city. I can live in my high rise and avoid all the congestion that’s happening in the streets below. However, I have to come down to the city (L1) at some point, and still deal with the traffic to go from one skyscraper (L2) to another.

So, at some point, people build new cities. And ultimately, these new cities will attract different types of people and will value different things. The same is true of blockchains. The Ethereum city values decentralization, the Solana city values speed, etc.

The question often arises, will there be one chain to rule them all? A better analogy perhaps is to think of blockchain networks as cities. Will there be one city? No. There will be some dominant cities, and many that matter.

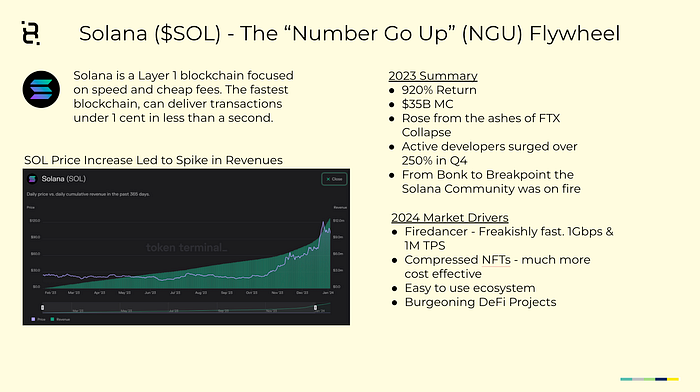

Solana is one example of a Layer 1 Blockchain. $SOL was one of the best performing assets in 2023 — up over 900%.

We looked at Solana in the previous cycle, when much of it’s value was SV vs UV. After it crashed and burned losing over 95% of its value… builders stepped in and turned challenges into opportunities. 2023 saw it rise from the ashes of the FTX collapse and Sam coins.

Higher prices beget more interest beget still higher prices. Developer growth surged in Q4. And one takeaway from the Solana story is to highlight that Blockchains are more than just the tech.

We don’t trade memes, and wouldn’t advise you to, but BONK becoming the most valuable memcoin briefly in 2023 highlighted the fact the Solana community was on fire.

In 2024 — we look forward to the launch of Firedancer. Basically enabling lightning fast high frequency trading on chain. And just like we talked about with cities — every city needs a fire department, and a police station etc. Every L1 will have a DeFi ecosystem and Solana’s has been exploding.

Solana definitely stole the spotlight in 2023 and it might even continue to outperform ETH over this cycle, we’ll see. But Don’t Sleep on ETH…

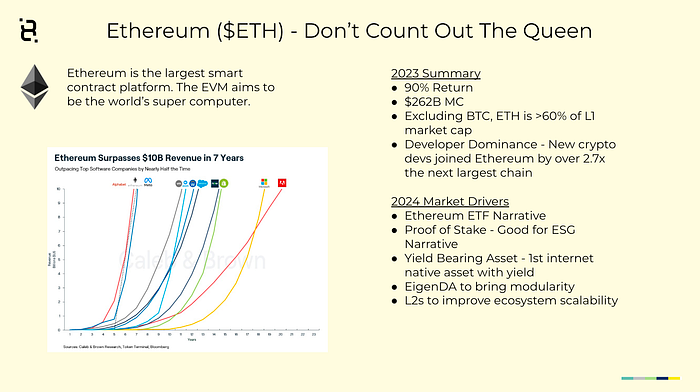

ETH is the 2nd fastest “company” to reach $10B in revenue — outpacing some of the largest tech companies on the planet

You’ll notice it’s 2023 performance (albeit 90% is pretty good) lagged other tokens. But Ethereum still dominates the developer ecosystem. New devs to crypto joined the Ethereum ecosystem at a rate of over 2.7x the next largest chain.

And 2024 has several narratives that will drive interest:

- We all saw what the ETF speculation did to Bitcoin price in 2023. Now we get to play the same game with ETH in 2024 with expected Ethereum ETF approvals in May. In fact the day of the Bitcoin ETF launch, ETH actually outperformed which just shows how fast the narrative shifts.

- This is ETH’s first cycle as a POS asset. While many like to critique Bitcoin for “using more energy than the country of greenland” we think ETH’s POS narrative will resonate with many ESG conscious investors.

- Also with staking — ETH becomes the first digital asset with yield baked in. We can now start to have a yield curve for internet assets. This is huge.

I’ll try not to bore you with too many charts, but we’ve been sharing this chart for months. This wedge that ETH broke out of recently has a mid-term target between 3.5–4K. We think 2024 is the year that ETH could play a lot of catch up .

As mentioned in the beginning in talking about narratives and challenges… one of the biggest problems last cycle was that the Ethereum networked ground to a halt due to high fees and low throughput. Since then L2s (remember, think skyscrapers) have been building like crazy, and have drastically decreased the cost of transacting in the Ethereum Ecosystem as you can see from the chart on the left.

This is our first real cycle to see L2s on the scene, and in 2023 they delivered higher beta on ETH. When ETH would have a good trading day, ARB and OP would rally 2–3x ETH’s move.

This is why we think ultimately the ETH ecosystem continues to accrue value, but perhaps ETH’s % of that value decreases as L2s appreciate.

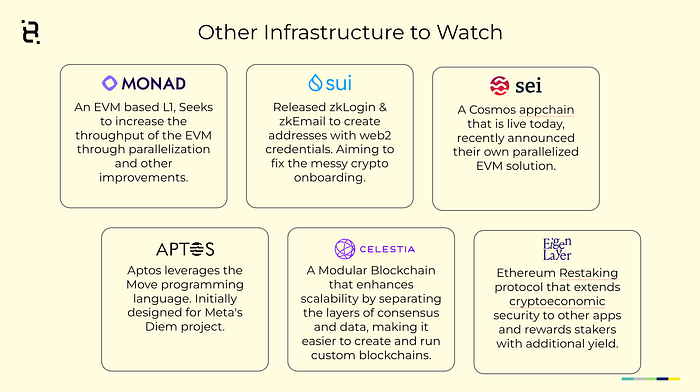

There’s lots of new projects to watch. These are some of the projects that just launched or will be launching in 2024.

All different versions of how to build blockchains, whether that’s Celestia’s approach to modular blockchains for more bespoke solutions, or EigenLayer, maybe the most anticipated launch in 2024, which is extending ETH staking security to the broader ecosystem.

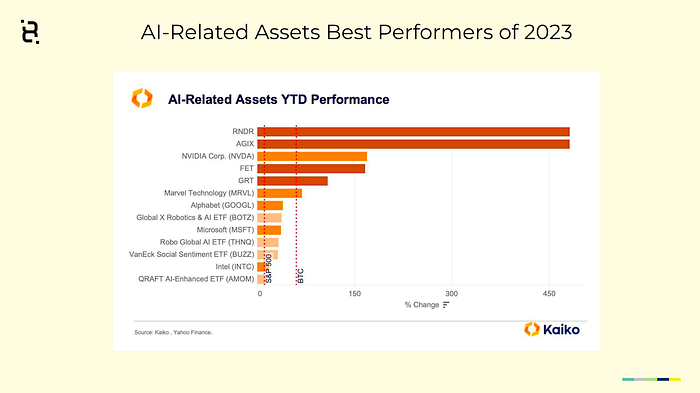

We all know 2023 was the year of AI. ChatGPT become the fastest app ever to reach 100M users. And anything even remotely related to AI soared in price. Speaking of Speculative Value, the PE ratio of NVDA going from 61 in 2022 and soaring to 148 today certainly seems to fit the realm of speculation. And you’ll notice crypto had it’s fair share of AI speculation in the likes of RNDR, AGIX and FET.

We even saw some people and VCs jumping ship from crypto to AI claiming that crypto was old and boring, and all new opportunities existed in AI. We say.. not so fast.

We think there are many ways in which Crypto & AI will grow together and ehance one another over time.

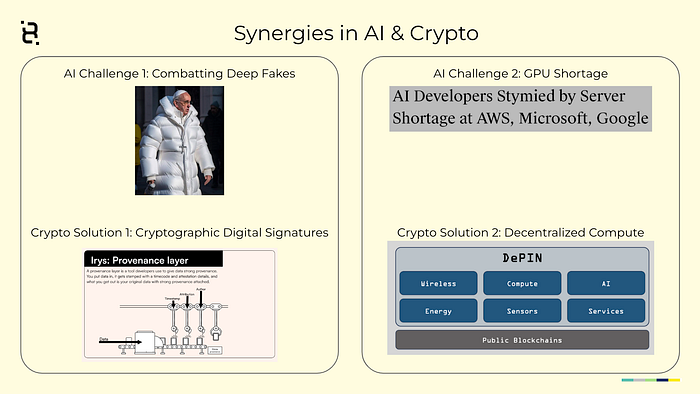

When AI allows us infinite creative abilities, it’s imperative that we know where things come from, what’s “real”. Whether it’s the Balenciaga Pope deep fake or something more more impactful, knowing the source of digital information will be increasingly more important.

Enter cryptographic digital signatures. Arweave and Irys are working to create a Digital Provenance Layer so that we can track the authenticity of all digital items that exist

Secondly, just like humans need to consume a lot of dead plant material, AI needs to consume a lot of GPU compute power. So much so, that the traditional Web2 companies are running short on supply.

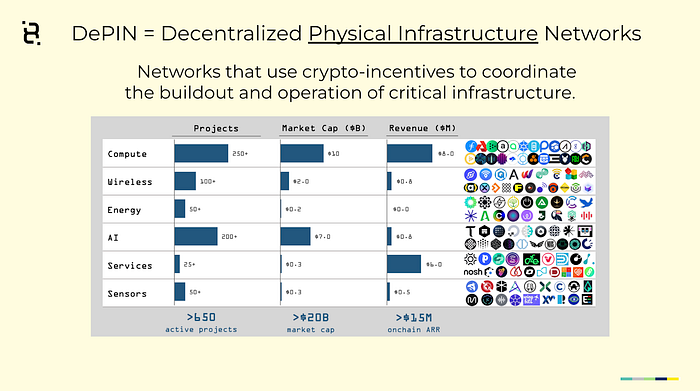

Enter DePIN. There’s a massive supply of compute and storage power that exists on people’s laptops and personal computers. Crypto networks can provide the necessary incentives to convert this into usable infrastructure.

DePIN is really coming into its first cycle, and there are a whole heap of companies focused in this area.

Again, DePIN is using crypto-incentives to bootstrap critical infrastructure. Whether that’s incentivizing people to put dashcams in their car and drive around to map roads with Hivemapper, or rent their extra laptop storage space to the Storj Network.

DePIN can roughly be broken down into these 6 categories, each one disrupting a $1T market

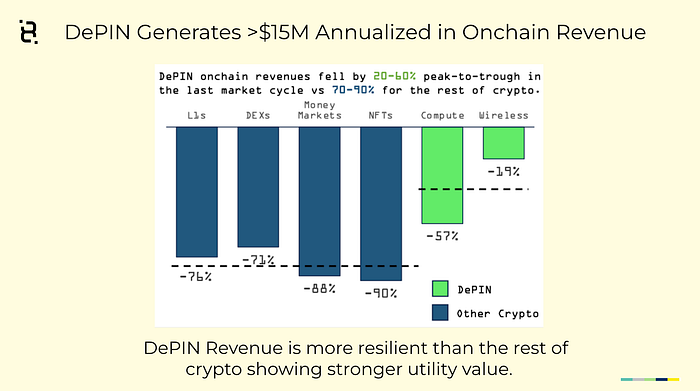

DePIN also differentiates in that it is largely supply shortage driven as opposed to demand driven. This results in DePIN revenue being more resilient as shown in this slide. Because DePIN revenue is tied to real world infrastructure, there’s more utility value vs speculative value compared to other crypto sectors.

We saw this play out during the bear market as other crypto sectors from DeFi to L1s to NFTs lost 70–90% of revenue from peak to trough. DePIN revenue was much more resilient by comparison.

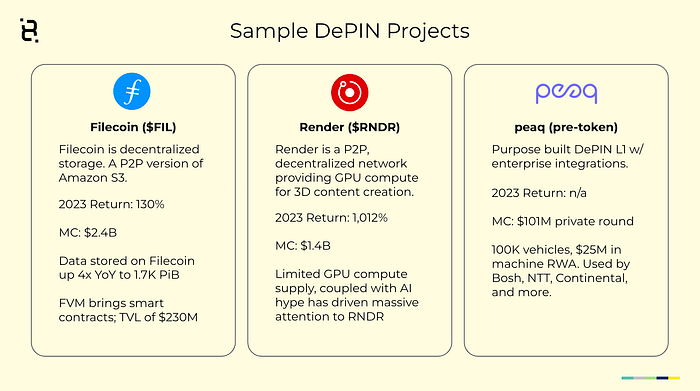

Here’s a quick overview of some sample DePIN projects

- Filecoin — been around a few years, big valuation, but they continue to innovate and grow. Releasing the Filecoin Virtual Machine (FVM) in 2023 which opens up new innovation within their ecosystem.

- Render — was up over 10x last year alone on the promise of near unlimited rendering capabilities unlocking GPU compute power.

- peaq — an early stage project we got connected with through our network that is expected to launch a token later this year. They built a DePIN specific blockchain that already has over 100K vehicles for ride sharing, and a host of enterprise partnerships.

DeFi has exploded from a niche area to an expansive category with real revenues and real product market fit. Coming into its second cycle, and we’ve seen how the market has separated the wheat from the chaff.

There are so many different sectors in DeFi now…

- Lending/Borrowing

- DEXes

- Payments

- Stablecoins

I’m going to highlight just a few themes, but you could spend a whole presentation on just one of these sectors.

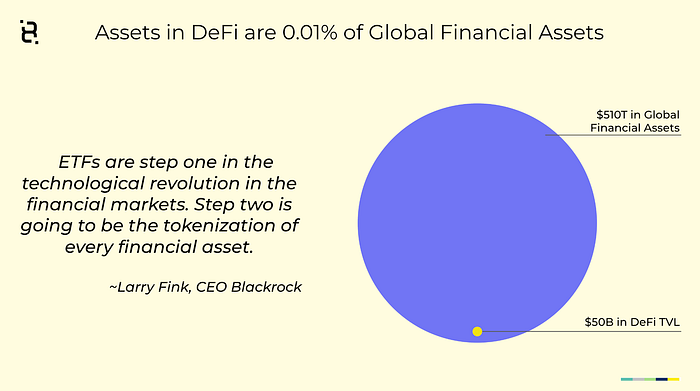

Just to zoom out on where we’re going… We just saw the Bitcoin ETF approved, and Blackrocks CEO has this to say about tokenization.

Can you see that little yellow dot? We have a long ways to go as an asset class before all assets are tokenized and part of the crypto ecosystem.

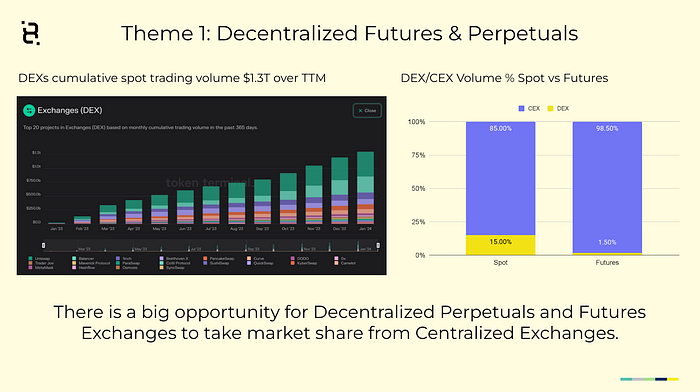

DEXs are one of the best businesses in DeFi. Last year cumulative DEXs traded over $1.3T in volume.

One of the biggest innovation in DEXs have been AMMs (Automated Market Makers). Connecting buyers and sellers online is very tricky, but with AMMs you can incentivize investors to park liquidity in a big bucket, and now allow traders to buy and sell against that big bucket of liquidity.

In 2022, when centralized exchanges were blowing up and losing trust, we saw spot DEX volume take off. Investors fled from Voyager to Uniswap. You can see this in the Spot DEX/CEX Volume %.

Decentralized perpetuals and futures have been a different story. The Futures DEX/CEX Volume % is only about 1.5%. We feel that this gap in terms of DEX/CEX volume in the Futures/Perpetuals market represents a compelling opportunity for Decentralized Perp Exchanges.

What is a perpetual? Another of the biggest innovations in crypto are perpetuals — which is essentially an option that never expires. When the pool has more longs than shorts, longs pay a premium and vice versa.

Here’s the lay of the land in Perp DEX ecosystem. dYdX has historically dominated this space, but a lot of up and coming players are competing for trading volume as well.

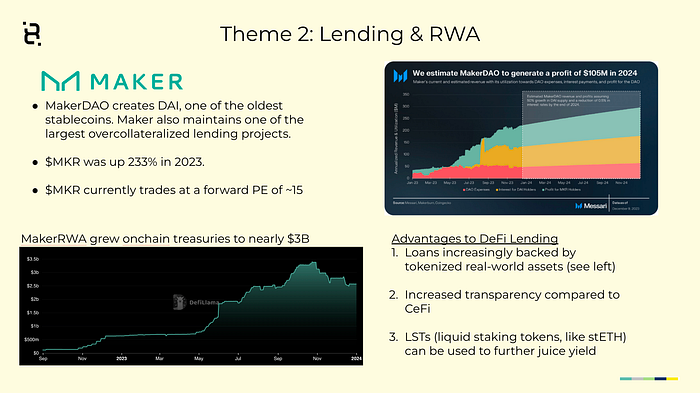

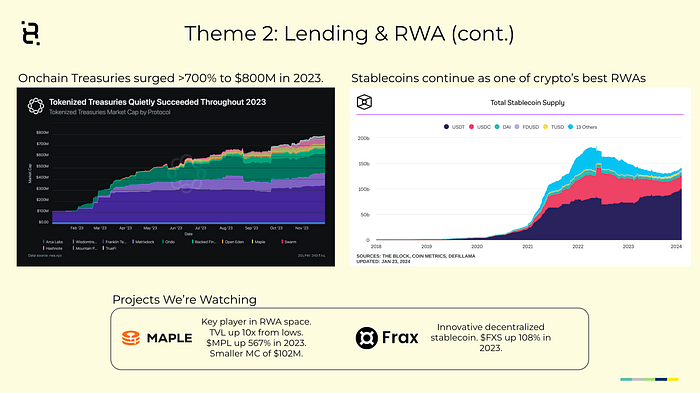

Another theme worth following is in Lending & RWA (Real World Assets). Overcollateralized Lending is sort of the bread and butter of DeFi, and has improved even further as the tokenization of real — world assets continues to proliferate.

Also worth noting a lot of these OG DeFi players are throwing off some serious revenue and profits with MakerDAO currently trading at a forward PE of ~15.

We’ve continued to see Stablecoins (the largest real-world asset) play a big role in the crypto ecosystem. In the west where money just works, we tend to take for granted many use cases that are hugely valuable for other parts of the world where hyperinflation is rampant. Savers in Africa can now access the dollar via stablecoins with just an internet connection — this is a game changer.

Thanks to increased interest rates from the Fed, many crypto projects took advantage and started offering unique onchain treasury options. The total tokenized treasury space soared to over $800M last year. Maple has been a project we’ve been involved with for a long time, and Frax is an interesting project more on the Decentralized side offering up a decentralized stablecoin product.

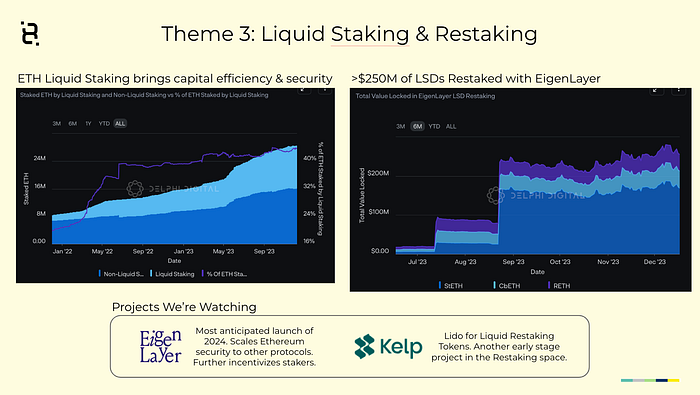

Finally, Staking and Restaking as a crucial theme for this next cycle. Staking is an interesting example of a challenge that was built during the bear market (2022 ETH merge launch) and is now emerging as a core narrative this cycle.

You’ll notice that since the ETH Merge in 2022, and ETH Staking has slowly been increasing. This currently represents a staking rate of 23.7% against the total supply of 120.2M ETH. Which is headed toward that 27% of total supply mark which is around the optimal security level.

Restaking is a new narrative for this cycle. Eigenlayer softlaunched in 2023 and is set to fully launch later this year. This expands the utility of staked ETH by using it to not only secure Ethereum, but also other pieces of infrastructure like bridges, appchains, rollups and other projects.

Last cycle we saw the Total MC 3x from $300B to $3T before we pulled back to below $1T. We’ve been consolidating at the $1T market cap for a while, and having just broke out we anticipate another 3x over this cycle. Obviously, this is crypto, so buckle your seatbelts for volatility along the way — but $10T here we come!