I launched 5 different AI-Generated Portfolios into the market. Here’s what happened over the past week.

Does AI give investors an unfair edge?

A Quick Recap on Last Week’s Article and Methodology

Last week, we initiated a real-world paper trading experiment to gauge the effectiveness of different trading strategies, including those generated by ChatGPT. The test involved three core approaches: the good old Buy and Hold, a ChatGPT-derived strategy, and optimized versions of both. Our goal was simple: to determine whether AI-generated strategies could be a disruptive force in trading.

The experiment was configured to be uncomplicated yet robust. Using technical indicators, we established five portfolios:

- Control: Buy and Hold of SPY, an ETF tracking the S&P 500.

- ChatGPT-Generated Portfolio: Developed based on a strategy crafted by ChatGPT.

- Optimized Portfolio One and Done: A one-time optimization of the ChatGPT strategy.

- Sliding Window and Expanding Window: Two continually-optimized portfolios using different windows of past data.

Our initial hypotheses were formed based on backtests, which showed promising results, particularly for the optimized portfolios. For more details about the experiment, check out the previous article where we launched the experiment.

Caveats to Keep in Mind

As a reminder, the trading strategies we are testing are simplistic, involving one asset and basic technical indicators. This simplicity serves as both a limitation and a potential avenue for further improvement.

Unveiling the Re-Optimization Process

As mentioned last week, a key aspect of our experiment involves re-optimizing some of our portfolios. For this week, however, they have not been re-optimized and, as a result, performed identically.

The optimized portfolios were re-optimized on Saturday, and as a result, we expect them to perform differently during the following week.

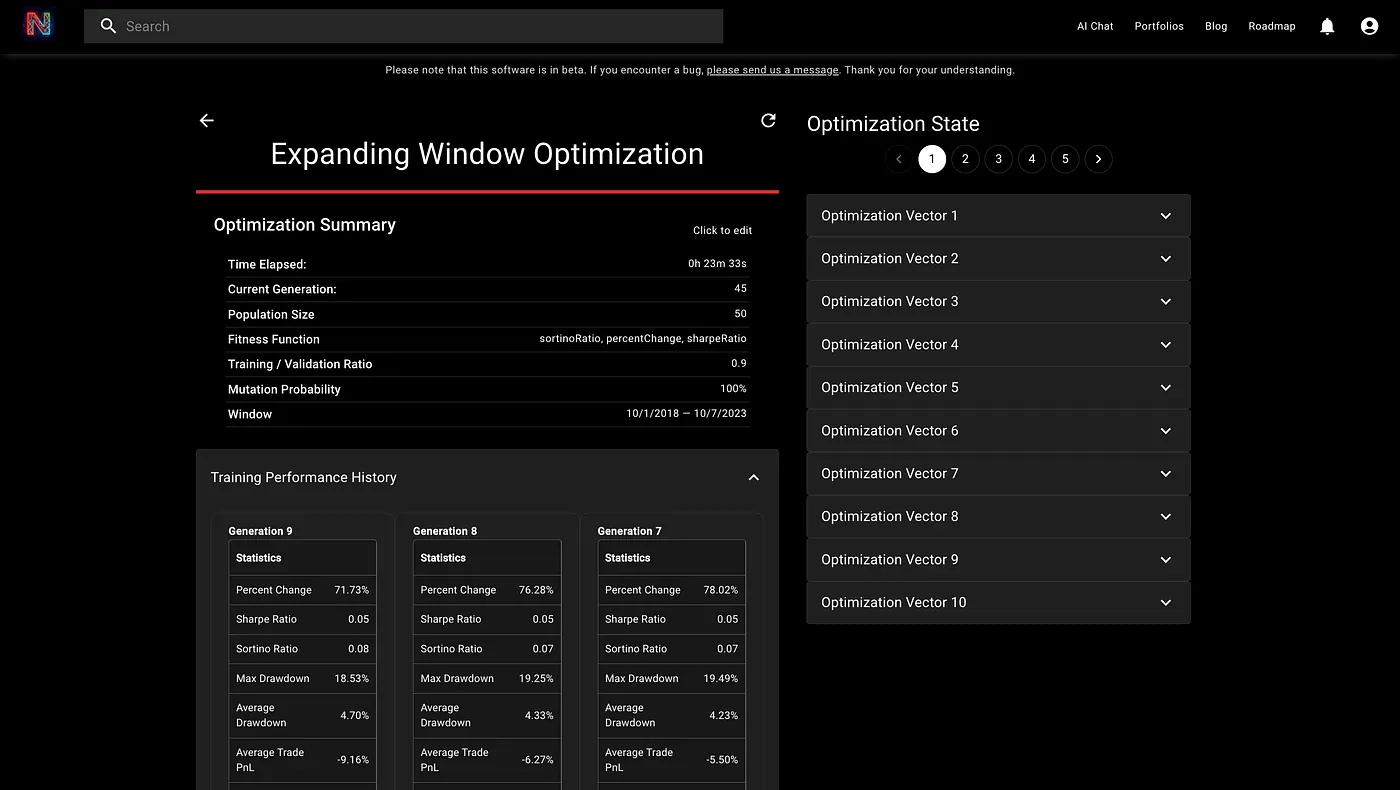

Expanding Window Optimized Portfolio

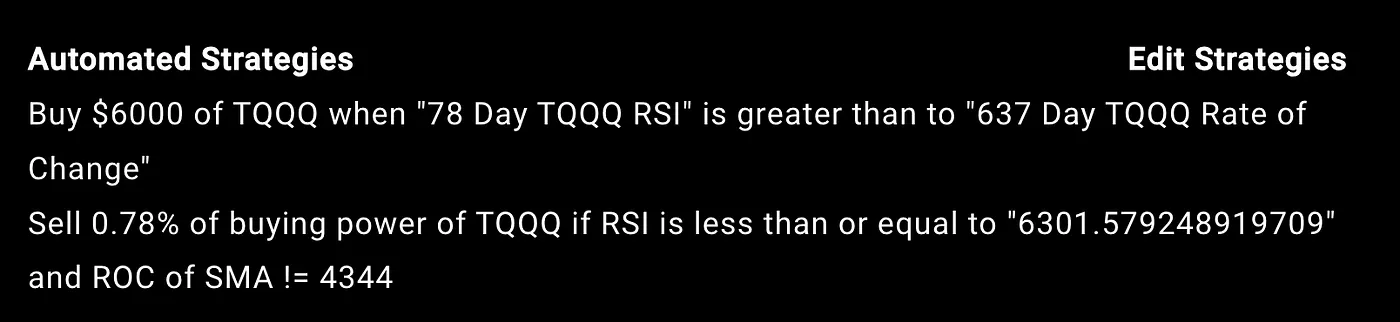

The Expanding Window Portfolio was re-optimized to have the same start date but a later end date. The result of this was a portfolio with two new rules that make it drastically different than the One-and-Done Optimized Portfolio.

Sliding Window Optimized Portfolio

In contrast, the Sliding Window Optimized Portfolio incremented the start date of the optimization and the end date. Interestingly, the sliding window portfolio generated similar strategies to the Expanding Window Portfolio

Both of these portfolios are incredibly bullish; a lot more so than the original One and Done Optimized portfolio.

It’ll be interesting to see what happens over the following week!

Performance Metrics: One Week In

SPY Buy and Hold

Our SPY Buy and Hold strategy, the benchmark for the experiment, recorded a loss of 1.05% over the week.

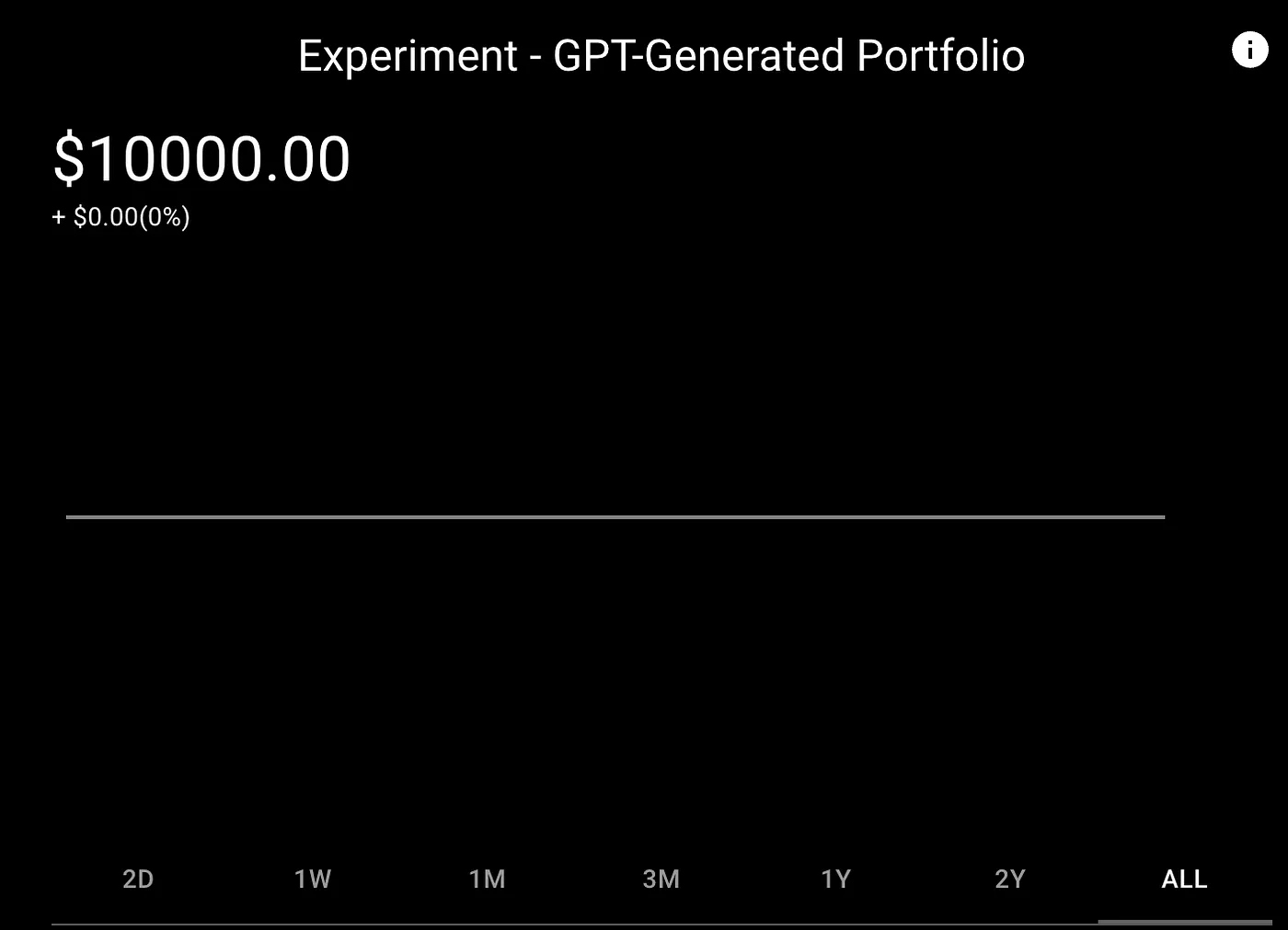

ChatGPT-Designed Portfolio

The ChatGPT-crafted portfolio stayed dormant, making no trades, and thus neither gaining nor losing any value.

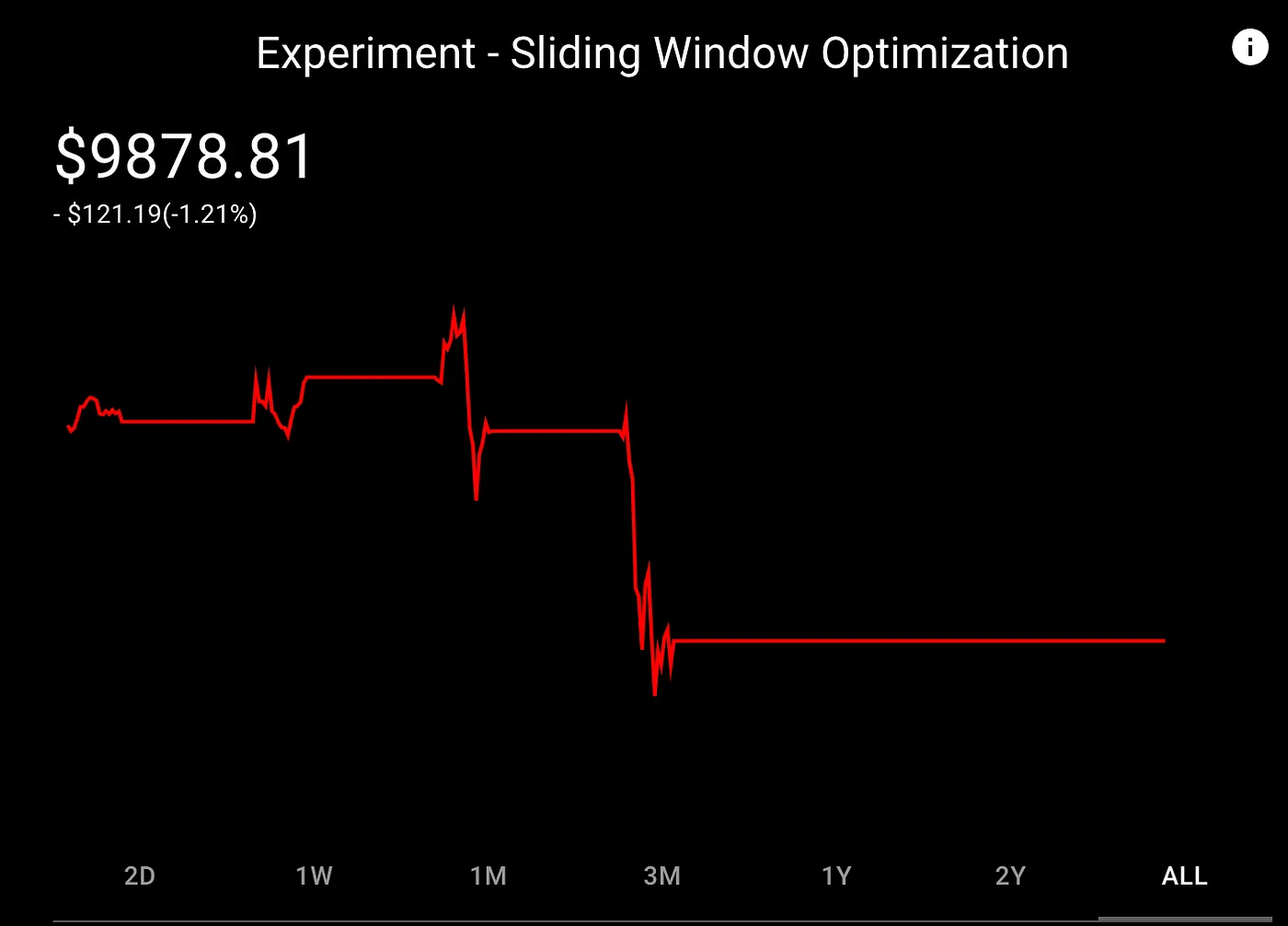

Optimized Portfolios

All optimized portfolios, which have yet to be re-optimized, registered a loss of 1.21%.

What’s Next? Stay Tuned for More!

The first week was an eye-opener but far from conclusive. The GPT-Generated portfolio remained inactive, while the optimized portfolios await their first re-optimization. All this sets the stage for an intriguing journey ahead.

Thanks for reading! Subscribe below to see how these portfolios fare over the upcoming weeks!