Ian MulheirnProductivity politicsAnaemic productivity growth is storing up fiscal problemsMay 15May 15

Ian MulheirnParochial economicsThe global economy is weighing on growth and bending our politics out of shape. We should talk about it.Mar 18Mar 18

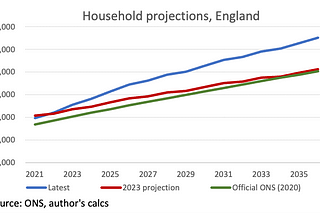

Ian MulheirnDon’t panic!What the ONS’s new population projections mean for household formation and housing needFeb 3Feb 3

Ian MulheirnLopsided macroeconomic policyA combination of OBR optimism and Bank pessimism on the outlook for the economy is screwing up macroeconomic policyDec 1, 20232Dec 1, 20232

Ian MulheirnA loan not a giftThere’s a lot of focus on whether the government is really cutting taxes after the Chancellor’s Autumn Statement today. Overall, they’re…Nov 22, 2023Nov 22, 2023

Ian MulheirnA four-point plan to reform fiscal managementFiscal tricks served up for voters at the Budget are bad for democracy, growth and the public finances. It’s time for an overhaul.Mar 22, 2023Mar 22, 2023

Ian MulheirnHousing affordability since 1979Rented housing has become increasingly expensive in recent decades. Why?Jan 18, 2023Jan 18, 2023

Ian MulheirnWhere did all that wealth come from?And what should we do about it?Nov 27, 20203Nov 27, 20203