Asset Protection Strategy: Double Irish Dutch Sandwich

People are often got lost with their financial planning not because they don’t understand the importance of having a plan for the future; most of the times, it’s because they don’t have access to legitimate information from trusted sources. The problem is, financial advisors often don’t make things clearer for their clients. Some of them use jargons that make them look ‘cool’ but don’t help their clients much.

We believe that financial advisors should educate clients, as doing so will help them win more business from the clients — and new referrals, as well.

One of the jargons that are obscure to asset holders is “Double Irish with a Dutch Sandwich” or any similar version of it. It’s an important concept every asset holder should know about to understand the true power of offshore asset protection strategy. To learn how the strategy works, focus on what U.S. corporations are doing in protecting their massive assets, pay fewer taxes in the process — and doing so legally.

In this article, we’ll tell you everything you need to know about the biggest tax avoidance strategy used by some of the biggest names in American business. This tax avoidance strategy is called the Double Irish with a Dutch Sandwich, and it’s being used by Google, Apple, Microsoft, and Facebook. It has been placed under scrutiny in recent years, and law changes abroad could change the face of the tax avoidance strategy that’s saving American businesses trillions in taxes.

What’s a Double Irish Dutch Sandwich?

When it comes to taxation, U.S. corporations typically look for the best advantages possible. The money saved in tax liability can be used for a number of things, including growth in the form of resources, facility, and human resources.

There is a fine line between tax evasion and tax avoidance, and while there are hefty consequences for tax evasion, smart tax avoidance techniques can be used to legally circumvent the loss of vast amounts of money in taxes paid to the IRS.

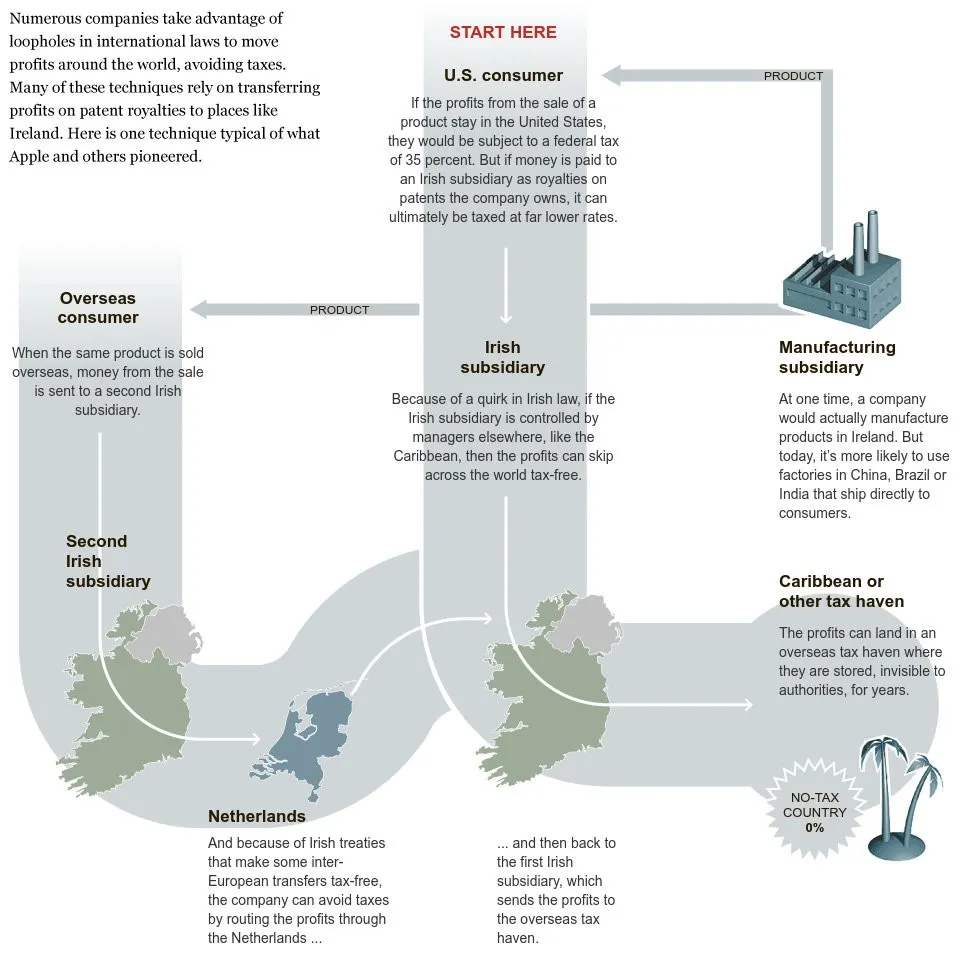

Double Irish with a Dutch sandwich — it sounds like a fancy meal, but it’s actually a tax strategy leveraging a combination of Irish and Dutch subsidiaries.

Essentially, American businesses can use these subsidiaries to move money around to tax jurisdictions and favorable scenarios that lend to lowered taxes. In many cases, taxes can even be eliminated with this strategy. By sending profits through a first Irish company, then to a Dutch company, then to a second Irish company working from a tax haven, the tax liability can be reduced or even eliminated without hurting profits.

There are many international tax avoidance strategies out there, all of which are legal and transparent. The Double Irish with a Dutch Sandwich is one of the most aggressive ones, however, and it’s the most widely used when it comes to drastically reducing tax liability for U.S. corporations.

Why Do Some U.S. Corporations Use a Double Irish with a Dutch Sandwich Strategy?

In the U.S., domestic corporations are held to a worldwide tax. This means that they are taxed on all income, no matter if it’s earned in the U.S. or abroad. This leaves corporations seeking ways to reduce their tax liability.

As you can imagine, companies like Google, Apple, and Facebook have huge profits to be taxed. The lower their tax liability is, the less tax they pay. With more of a bottom line, these domestic corporations have more money to spend and grow their workforce and invest into the overall growth of their companies.

While a Double Irish with a Dutch Sandwich certainly isn’t a great fit for all U.S. corporations, it’s a critical strategy for some.

How a Double Irish with a Dutch Sandwich Works

There’s something called a Double Irish Structure at the core of this strategy, and we’ll start by explaining that situation.

A Double Irish Structure occurs when a U.S. domestic corporation creates two Irish subsidiaries. The first one is an Irish subsidiary under Irish law, but it’s managed in a low-tax country. Irish law tends to determine tax residency based on the country where the company is managed, and that’s where this unique dynamic begins. As you can see, this first Irish company is treated as an Irish company by U.S. tax, and there’s no tax under Irish law.

Then, there’s a second company owned by the first. This company is managed solely in Ireland, and the second company’s payments to the first are put on the books as royalties for the use of the first company’s IP in Ireland. The second company turns around and deducts the royalty payments they made as a trading expense. Any income left over on the second company’s end is taxed. The first company would usually be located somewhere with no taxes, such as the Cayman Islands.

Back in the U.S., the second company is treated as a disregarded entity for tax purposes, and both companies treated as Irish companies.

Now, we add in the Dutch component. Dutch has minimal taxes on outbound royalty payments, but any EU country could be used. This company is added to avoid withholding taxes by licensing the first company’s IP to it, and then the third company sub-licenses to the second company. The Dutch company is treated as a disregarded entity, and royalty payments between the second company and the Dutch company have no Irish withholding taxes — payments made between EU countries can’t be taxed.

Conclusion

The Double Irish with a Dutch Sandwich is a powerful tax strategy that is highly beneficial for the company’s who use it. In 2015, the Irish finance minister closed these loopholes, but grandfathered-in companies can still use the strategy until 2020. Regardless, corporations will always find loopholes to protect their assets — perhaps in a different fancy-named strategy, but the same purpose.