Delta Neutral GLP Strategy

Hi all, this is the Neutra Finance team.

We are here to introduce Neutra Finance’s first strategy, the nGLP Vault : Delta Neutral GLP vault.

If you have any inquiries, feedbacks, partnership proposals feel free to contact the team at official@neutra.finance !

Contents

- GMX

- GLP

- What makes GLP special

- What we can solve for investors

- Introducing GLP Market Neutral Vault

- TL;DR

- Overview

- How is the Delta Neutral state achieved?

- How is the Delta Neutral state maintained? : Rebalancing

- Our Rebalancing : Tolerance Band — Volatility Model

- Backtesting

*Risk calculation & deriving the rebalancing threshold

*Performance Data

*GLP investment vs. nGLP Vault - Ending Remarks

1. GMX

What is GMX?

Anyone who is interested in DeFi should all probably know GMX by now. GMX is a decentralized perpetual exchange, and is one of the hottest DeFi projects.

Currently, GMX has surpassed 170K user wallets, a cumulative transaction volume of $69B, and cumulative fees of $92M. The project is showing successful progress within the market. You can check out their stats at https://stats.gmx.io/

If you want to know more about GMX, check out this article!

2. GLP

Now let’s look into the factor that is so essential to GMX and what makes it special, their liquidity pool token GLP. Simply put, all trades within GMX — swapping and perpetual trading — take place through the GLP pool. Users can invest in GLP and receive protocol fees as rewards for providing liquidity.

The strengths of GLP can be summarized by the following

- GMX’s huge volume and fee

- No impermanent loss

- Profits proven by history

3. What makes GLP Special

Fee

GMX’s fee structure gives 70% of protocol fees to GLP holders. Currently an average of 3M~4M daily volume is being created, resulting in around 500K~600K fees per day.

The graph above shows daily fees converted into APR. As this is based on the time of writing, there may be a small difference from the current values.

Even considering that, we can see that an attractive APR of 30~40% is being given to GLP investors.

No IL(Impermanent Loss)

Existing DEXs use the AMM pricing mechanism to enable trades between assets. Such a model requires liquidity providers, who receive tokens and trading fees as rewards. However, there are many instances where LPs are facing more losses than returns due to a well known limitation called impermanent loss.

Rather than using the standard AMM model, GLP uses oracles to bring in prices from major CEXs, which means there is no impermanent loss when providing liquidity to GMX.

Profits proven by History

It can be said that traders’ PnL is one of the aspects that makes GLP an attractive investment. As traders make their trades against the GLP pool, if they win, their profits are taken out of the pool. If they lose, their losses are deposited into GLP, leading to GLP profit.

This may seem risky for GLP holders, but first let’s have a look at some historical data and see the results. (You can check the stats at https://stats.gmx.io/)

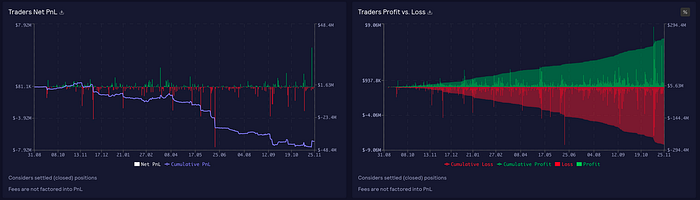

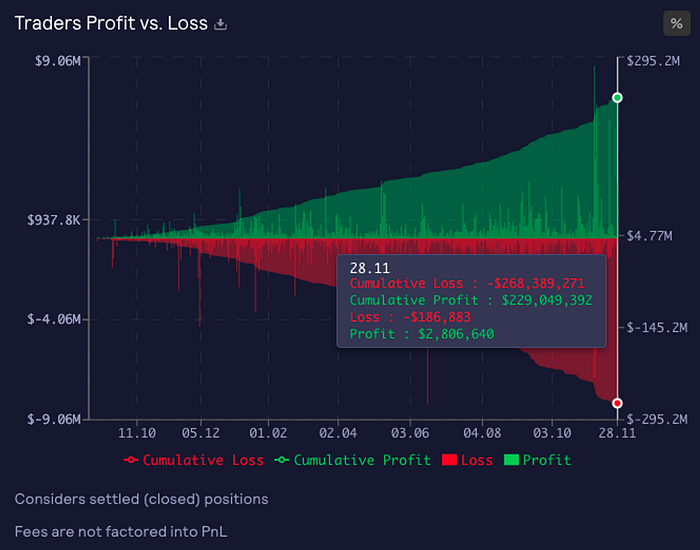

Below is the all time cumulative PnL of traders. The graphs show how traders have performed to this day.

Since GMX’s launch in August 2021, the cumulative PnL has always seen more loss than profit.

Here we can see that throughout GMX’s operating period of 1 year and 3 months, cumulative loss has exceeded cumulative profit by up to $40M. This has all been counted into GLP profits, of course all the while earning the high APR mentioned above.

4. What we can solve for investors

While GLP is such an attractive investment, there is one factor that may make one hesitant: the market condition.

The current crypto winter and the ongoing credibility issues regarding the crypto market have boosted DeFi users’ demand for safe and long-term investment. Prices have fallen, and we have seen cases where the market situation has been determined by particular players.

As such, though GLP boasts high returns, it may not be considered a completely safe asset. Because even with these rewards, the prices of the assets composing GLP have fallen.

What if there was a way to invest in GLP without being affected by the market?

- High APR created by high volume and large fees

- No losses from IL

- Profits from traders’ PnL

Based on these advantages, the size of the asset will increase steadily.

5. Introducing Delta Neutral GLP Strategy

TL;DR

- Open long position via GLP investment & open short position through GMX Perp Trading

- Maintain asset delta neutrality through a unique rebalancing mechanism

- Performance data shows up to 10% yearly APR

- Using GMX 100% helps to improve security and synergy with GMX

- Coming soon. ~2023. Q1 🔥

Delta Neutral GLP Vault (nGLP Vault)

Overview

- DAI is deposited as input token into the vault.

- The money invested in the vault is used for purchasing GLP and Perp Trading.

- Through holding GLP and short positions, users’ funds become delta neutral.

- We use a unique rebalancing trigger algorithm to maintain delta neutrality.

- The vault returns GLP APR rewards.

How is the Delta Neutral state achieved?

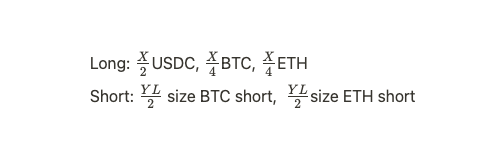

Let’s assume that Bob is our user.

Should Bob simply buy and hold GLP, he will be exposed to price fluctuations of BTC and ETH, the portion of non-stable assets that compose GLP.

*We have excluded tokens with insignificant influence from calculation, consider stablecoins are equal to $1, and assume that GLP’s composition ratio is BTC:ETH:USDC = 1:1:2

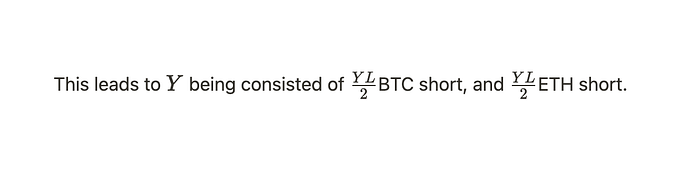

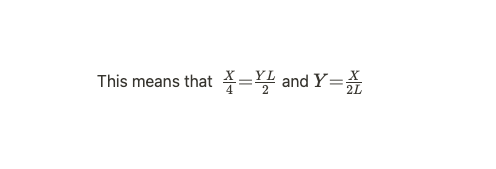

To achieve delta neutrality for BTC and ETH price fluctuations, a certain percentage of assets must be used to open perpetual short positions so that the long exposure to ETH and BTC are balanced out.

If X amount from the principal is used to buy GLP,

Y, the remaining assets from the principal excluding X, is allocated to Perp Trading and used for opening leveraged ETH and BTC short positions.

L = Leverage

If you look at Bob’s current assets right now,

When assets in the long position and short position are the same size, the overall position is in a delta neutral state.

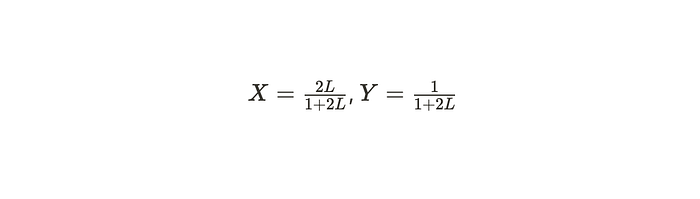

By using that X+Y=1 , both X and Y can be simplified for L

How is the Delta Neutral state maintained? — Rebalancing

Now, Bob’s assets are delta neutral to market price changes.

However, this delta-neutral state is applicable for only a certain point in time: namely, when GLP’s assets are 1:1:2, long position:short position = 1:1, and when liquidation risk is low.

GLP configuration changes dynamically with market conditions, various trading activity within the platform, and GLP purchases/sales.

When the weight of assets within GLP fluctuates and a portion of the position is exposed to delta, the strategy vault sells some GLP to open more short positions, or closes a part of the short position to buy more GLP.

This process of adjusting the position with changing conditions to return the position to a neutral state is called rebalancing.

The success or failure of a strategy that pursues delta neutrality is determined by two factors.

- Is delta neutrality continuously maintained through rebalancing?

- Is the strategy still profitable even considering the costs used for rebalancing?

In other words, maintaining delta neutrality as stably and efficiently as possible through rebalancing is the key and goal of the strategy.

Our Rebalancing — Tolerance Band — Volatility Model

There are mainly two known models for rebalancing. Calendar rebalancing, which rebalances periodically at set time intervals, and the Tolerance Band model, which rebalances when asset weights reach a certain threshold.

Calendar rebalancing has been excluded, since there is no “optimal” timing in an ever-changing market. Not rebalancing often enough will of course be a problem, but rebalancing too frequently also negatively affects the strategy, since the costs of rebalancing will outweigh profits from rewards. This model creates further inefficiencies because it simply rebalances with passage of time, even in cases where rebalancing is unnecessary.

The Tolerance Band model offers a more efficient solution, since it rebalances based on how overweight or underweight the portfolio is. However, it still faces the limitation of not being able to effectively react to current market conditions and rebalancing after the position has been already exposed to delta. Where the portfolio is composed of different assets, the differences in volatility between these assets are not accounted for either.

What would happen if each asset’s volatility range can be predicted based on recent price data using an algorithm, and what if we can preemptively rebalance the position? Would it then be possible to both increase efficiency and reflect current market conditions?

Let us introduce the Tolerance Band — Volatility Model. Our model uses an ATR(Average True Range) algorithm who brings in recent price data and analyzes them to provide a prediction of volatility. Rebalancing is triggered when “asset weight deviation + predicted volatility range” exceeds a certain threshold, which we will call the m value. Details on how we derived the optimal m value is explained below.

The advantages of using our Tolerance Band — Volatility model can be summarized as the following:

- We are able to more actively reflect the volatile crypto market. This enables preemptive rebalancing, which then enables us to achieve true “delta neutrality”.

- We are able to derive an optimal rebalancing timing, which makes it possible to provide attractive returns to users.

Backtesting

To provide a better understanding of our strategy, here we would like to present our backtesting data.

- Process of deriving our m value

- Performance data: holding GLP vs investing in nGLP

Risk calculation & deriving the ‘m’ value

Suppose that

being the number of rebalancing over a given period generates revenue that follows the normal distribution of

are all independent.

In this case, the sum of revenue from all rebalancing within the period will follow the following distribution.

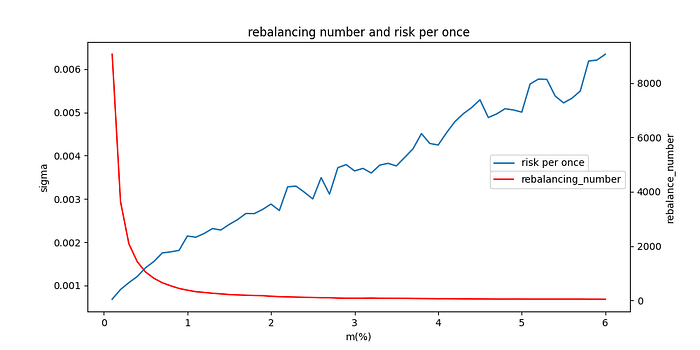

To evaluate a strategy, it is important to find a strategy that has a higher sum of revenue, i.e. n∙μ, but we also have to take into account the risks. A “good” rebalancing strategy is thus one that generates high profit per risk, with risk here being represented by the standard deviation √n∙σ .

If m is too large, allowing for a wider volatility range,

- Rebalancing will occur less frequently.

- As delta exposure lasts longer, risk σ per rebalancing will naturally increase, resulting in an overall higher risk for the entire period.

On the other hand, if m is too small,

- Rebalancing will occur too frequently.

- As a result, the value of n will increase rapidly, increasing the risk.

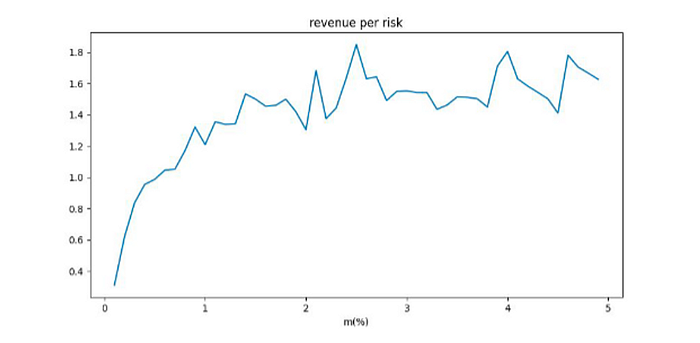

At m = 1%, earnings based on the value of m fall rapidly due to transaction fees, but after this point, profits are almost constant. If we combine these values to calculate “revenue / standard deviation”, we get the following graph.

From here, we were able to find that m = 2.6% is the optimal rebalancing threshold, with the highest revenue per risk value.

Performance Data

💡 Factors

- Timeframe:

- 2022–06–27 14:10:48 ~ 2022–11–21 20:54:14

- Price data: GLP price

- GLP APR: assumed as 20%

- Testing fund $10,000

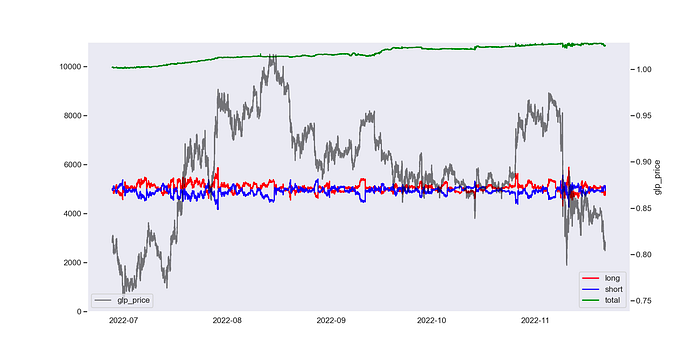

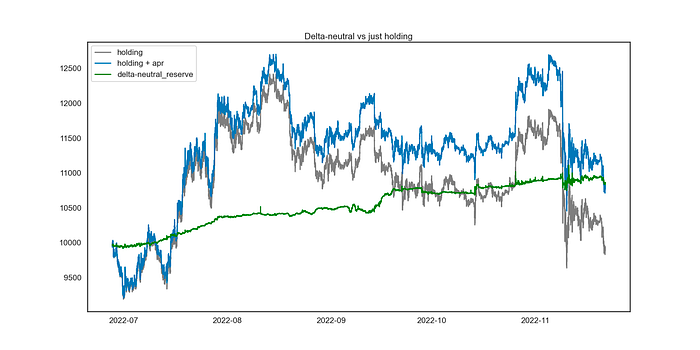

The graph above shows changes in fund size, GLP price trend, and long and short values within the portfolio. We can see that

- Even with GLP price fluctuations, the total position value (green line) sees a steady increase. This is the result of accumulating around 90% of GLP’s APR through our GLP holdings and continuously hedging out delta through rebalancing.

- Through our rebalancing mechanism, the long value(red line) and short value(blue line) are tight mirror images of each other. This shows that the funds are maintained at near zero market exposure.

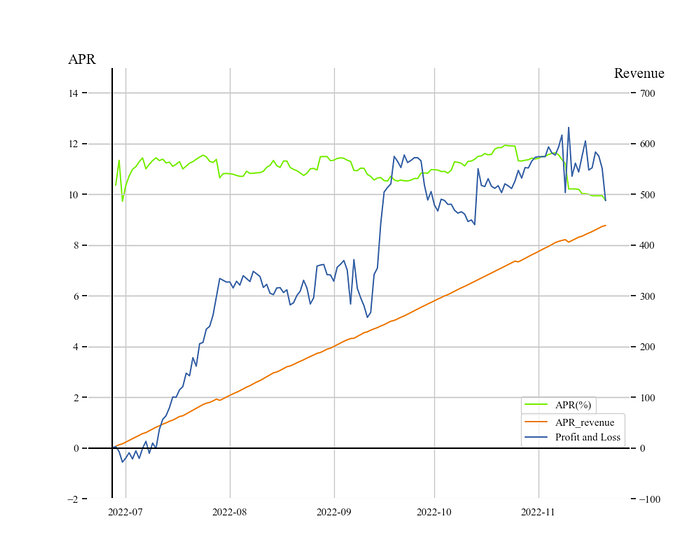

The graph above shows 3 types of values:

- The amount of traders’ PnL earned on our deposited fund (blue line)

- +$470.9866 → 11.304% in terms of yearly APR

2. The net rewards earned on our deposited fund (green line)

- +$407.0217 → 9.77% in terms of yearly APR

3. This net reward shown as APR (orange line)

- The orange line shows that APR has been consistent throughout the timeframe

Hence, our equity value($10,000) has increased by 4.6% during the timeframe(11.304% in yearly APR), increasing to $10,470.9877. In terms of rewards earned from holding GLP, the strategy returned 4.07% during the timeframe(9.77% in yearly APR), earning $407.0217.

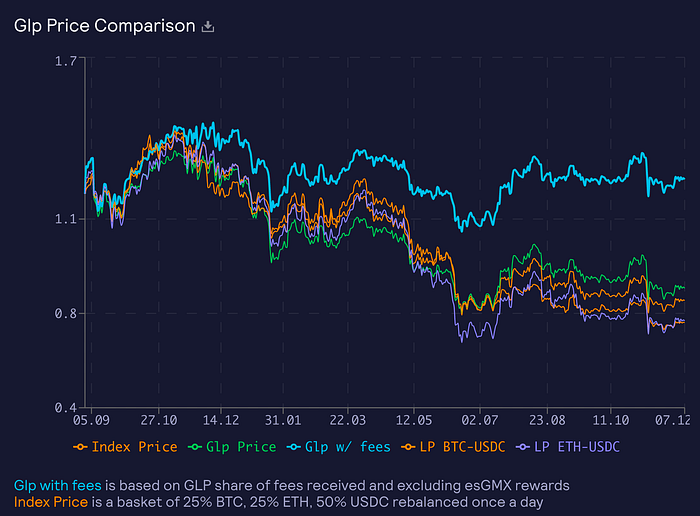

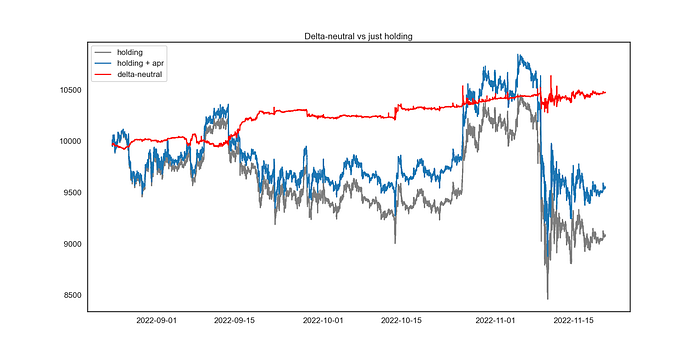

GLP Investment vs nGLP Strategy

The graph above shows what would happen if we deposit $10,000 into

- Simply holding GLP

- Holding GLP with rewards

- Investing in our nGLP strategy

It is true that should GLP’s composing assets increase in price, simply holding GLP may see better returns than our strategy. However, assets are constantly fluctuating in times of market volatility. If you were to invest in the nGLP strategy, your total assets would be protected from fluctuations and you would see a steady increase in position value without having to manage your assets yourself.

Below is the performance data on a 3 month time span

- 2022–08–24 00:00:31 ~ 2022–11–20 17:13:20

You can still see that the nGLP strategy shows the same steady upward trend regardless of when you enter.

6. Ending Remarks

Our nGLP strategy aims to be as safe as staking your stablecoins, while returning higher profit. With a strategy that allows you to invest in GMX’s profitable GLP token with added stability and reduced risk, you will be able to add a more sustainable and profitable product into your portfolio and remain care-free even in unstable market conditions.

As a last note, our strategy utilizes GMX 100%, meaning every step of the process from buying GLP to shorting ETH and BTC take place using only the GMX protocol. In doing so, we expect to contribute to the following:

- Reduce security risks compared to using multiple external protocols

- Provide not only liquidity but also create trading volume on GMX, contributing to the overall growth of the project

We plan to launch the strategy in Q1 of 2023. The team will constantly strive to provide a greater value than what we have presented in this article.

We also have other market neutral strategies in testing, along with token economics and insurance policies that will help you sit back and comfortably earn passive income in any market condition.

Please stay tuned!