Niamh BarryinCaribou DigitalShifting through the noise in the age of information overload — the power of evidence synthesisJun 27Jun 27

Niamh BarryinCaribou DigitalRethinking evaluation in a post-Covid-19 digital worldThis could be a transformative moment for the field of Monitoring and Evaluation. Here’s how.Jul 30, 2020Jul 30, 2020

Niamh BarryDigital Credit — What do we know about the impact on clients?Niamh Barry, Natasha Beale, Carson Christiano, and Alexandra WallNov 20, 2018Nov 20, 2018

Niamh BarryinFiDA PartnershipDigital payments and transfers — the P2P impact storyThere were 690 million registered mobile money accounts as of December 2017. The digitization of a pre-existing behavior — sending and…Nov 20, 2018Nov 20, 2018

Niamh BarryinFiDA PartnershipDigital Credit — What do we know about the impact on clients?This post has been co-authored by Niamh Barry from the FiDA Partnership, and Natasha Beale, Carson Christiano, and Alexandra Wall from the…Nov 5, 2018Nov 5, 2018

Niamh BarryDigital savings — What do we know about the impact on clients?We focus on if and how ‘digital’ has improved savings behavior among low-income populations.Oct 28, 2018Oct 28, 2018

Niamh BarryinFiDA PartnershipDigital savings — what do we know about the impact on clients?Saving is a sound financial practice, particularly for people with lower or fluctuating incomes. Savings help people cope with a poor…Oct 23, 2018Oct 23, 2018

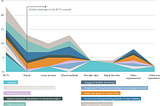

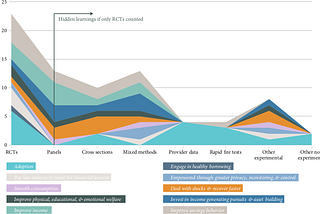

Niamh BarryinFiDA PartnershipLaunching the Digital Finance Evidence Gap Map 2.0A live, online tool, with functionality for filtering and exploration of impact studies by product, delivery method, and and…Oct 3, 2018Oct 3, 2018

Niamh BarryinFiDA PartnershipGetting off the methods pedestal — how can we assess the impact of Digital Finance on clients?There is an impact conversation and we need you to join it.Apr 23, 2018Apr 23, 2018

Niamh BarryinFiDA PartnershipIs digital finance changing the lives of the “excluded” for the better?It’s easy to assume different people will use digital financial services the same way, but factors like age & gender shape impact outcomes.Apr 5, 2018Apr 5, 2018