An In-Depth Startup Analysis: Is Classpass the Next Unicorn or the Next Bust?

Over the last few years, I have taken a keen interest in the fitness and wellness industry and the impact of technology in disrupting the fragmented local fitness marketplace. My previous startup Yoga Panda aimed to create a 2-sided mobile marketplace connecting yoga studios and eventually fitness studios with consumers interested in booking classes on a ‘pay-as-you-go’ model based on dynamic pricing driven by supply and demand.

One of the main players in this industry is Classpass and I have been closely following their evolution and growth over the last 3 years. During this time, Classpass has grown to over 200 employees, expanded to 39 cities worldwide and 8,000 fitness studio partners, thanks to $84 Million of funding. This month, Classpass founder Payal Kadakia stepped down from her role as CEO and she has been replaced by Fritz Lanman who has been an early investor of the company and the chairman of the board since the seed round.

With this change, the question that has been on my mind is whether Classpass which was valued at $400 Million in their last funding round is on the path to become the next Unicorn (private tech company that’s valued at over a Billion dollar). Or if trouble lies ahead, and they are destined to become a bust like many other tech based startups that are focused on operating a 2-sided marketplace who end up failing to sustain themselves at scale with healthy margins without the continuous injection of additional capital.

Rather than just voicing an opinion for the sake of having one, let’s try to take a deeper look at Classpass and try to come up with a more educated opinion about this startup — hopefully a rational one :) ! Let’s tackle this question by getting a better understanding of what they do and what their value proposition is. We’re going to do that by reviewing their history, evolution and key pivots over the last few years, then deep diving into their business model and their profit margins before finally taking a look at their challenges, risks and opportunities ahead.

Understanding the Boutique Fitness Industry

The fitness industry has been historically dominated by traditional big box gym facilities that provide a variety of fitness equipment and free weights in addition to a selection of group classes. Over the last 10 to 15 years, there has been a significant increase in popularity of boutique fitness studios that offer very specialized group classes in one of the following: yoga, boot camps ,cycling, barre etc. These are typically much smaller facilities that sell monthly memberships or class packages for a specific number of classes. The average price for a monthly membership at a specialty fitness studio is typically 2 to 4 times higher than that of a traditional gym. According to the IHRSA, over a third of the $25.3 Billion generated by the industry in 2015 in the US came from these specialty boutique fitness studios. While there are few chains and franchises that have emerged over the last few years such as Orange theory, SoulCycle, Corepower Yoga, CrossFit, Pure Barre etc. the very large majority of this segment of the fitness market is fragmented and these fitness studios are typically run by a local small business owner with one location.

The #1 challenge faced by these fitness studios is often customer acquisition. They typically have a fairly fixed operating cost to serve their customers and offer a certain number of classes each day and these typically include rent, utilities, teacher & staff pay . Besides the top studios in the market and a few select class times, the very large majority of studios and class times are often operating under capacity and the incremental cost of serving additional customers is minimal. Studios are therefore on an ongoing quest to attract more customers through the door and convert them into regular paying members.

One of the main solutions that emerged in the 2009 to 2011 period to help with this customer acquisition challenge faced by fitness studios was Groupon (and the other group buying platforms). However, it proved to be a double-edged sword for many of these fitness studios. While it often led to a flow of new customers through the door, they were often paying very little for classes, they sometimes led to the overcrowding of certain sessions that would negatively impact the experience of existing full-price paying customers. They caused additional overhead to get people signed up for the first time and ultimately often proved unsuccessful for many as an effective marketing tool since the conversion rate of Groupon users to regular paying customers was typically low.

While fitness studios appreciated the incremental revenue generated by Groupon, many ended up with regularly busy classes yet they were full of unprofitable customers that had no intentions to convert to regular paying members. These studios often just ended up shutting down after a while as they failed to become profitable. Besides Groupon, these fitness studios could tap into more traditional marketing and advertising channels but, this often either required a certain level of time investment and expertise to properly manage and optimize, or an up-front budget with no guarantees in terms of success and return on investment. For small business owners operating these boutique studios, a performance-based marketing solution is typically the preferred option for them as it doesn’t require any upfront cost on their part as they can just pay the 3rd party a portion of the revenue generated by new customers. Groupon, while performance-based was generating too little per customer and often had too low conversion rates for studio owners to love it. The “raison d’etre” of Groupon for customers was to provide them with a deal and a great discount. Groupon was therefore, not in a position to change its business model to better serve the needs of fitness studio owners, that is exactly the void that Classpass helped fill for boutique fitness studios.

Understanding the Evolution of the Fitness Consumer Mindset

For the longest time, the fitness industry’s business model has been based on selling monthly memberships to consumers while maximizing the number of subscribers with a membership size cap that is a high multiple of the actual capacity of the facility. This is driven by the fact that not everyone is present at the facility at the same time and more importantly many members end up paying for monthly subscriptions that they do not use or that end up being underutilized. Consumers were traditionally marketed to with offers for risk-free multi-day trials followed by special deals to become regular monthly members along with all kinds of sales tactics to get people to commit. The gyms often see significant peaks and valleys in terms of attendance and signups based on seasonality with a big spike in January as people tend to be very committed to their new year fitness-related resolution. But it drops significantly over time as the summer months come around and consumers slowly forget about their new year resolution and often prioritize spending time outside rather than indoors in a gym. These fitness centers typically see a spike in membership cancellations in the April time-frame as many uncommitted consumers who may have signed up in January end up canceling their monthly membership after it goes unused for weeks or months.

As the boutique fitness studio trend started picking up, consumers got curious about these new trendy work-outs they were reading about in the media and about the new fitness studios that started opening up around their neighborhood. This is especially true for affluent women in large cities which often made up the majority of the customer base of these fitness studios. These boutique fitness studios — that often looked more like spas than traditional gyms provided a more appealing “product/service” to this audience than what they traditionally experienced at big box gyms. As these boutique fitness studios started becoming trendy, Groupon was also gaining in popularity and it provided a convenient and very affordable way to discover and explore different new fitness work outs and various fitness studios.

Groupon users can be segmented in different groups:

- Some used Groupon as a way to try different studios at a low price before finding one that they really liked and becoming a regular customer there. Studio owners loved this segment.

- Other Groupon users used it as a way to try a new fitness routine or studio at a low price with no intent of committing to it long term. While a minority of those in this segment might accidentally stumble upon something they love and end up committing to it, they typically don’t.

- Finally, there is a segment of the Groupon user base that sees Groupon as a great way to get a good deal on new trendy fitness work outs and get into “Groupon studio hoping” by moving from one studio to the other and one offer to the next since they can typically only take advantage of a Groupon deal at a studio once. While this can sometimes be inconvenient, the value they get makes it worth it. Fitness studios generally hate this segment of the Groupon audience as they have no intent of becoming regular members after the end of the deal.

While Groupon does provide value to all three of these segments, it has many limitations for consumers which make it an imperfect solution such as:

- The disconnected experience between the buying of the deal and the redemption process.

- The lack of integration and information about class schedule within the Groupon site/app.

- The restriction on not being able to buy a deal multiple times.

Furthermore, Groupon negatively impacted the perception of many consumers relative to the monetary value of the service offered by these fitness studios. Groupon enabled them to pay a fraction of the regular price of the service. These Groupon limitations and the perceived high price of monthly memberships by many consumers created a void that Classpass helped fill.

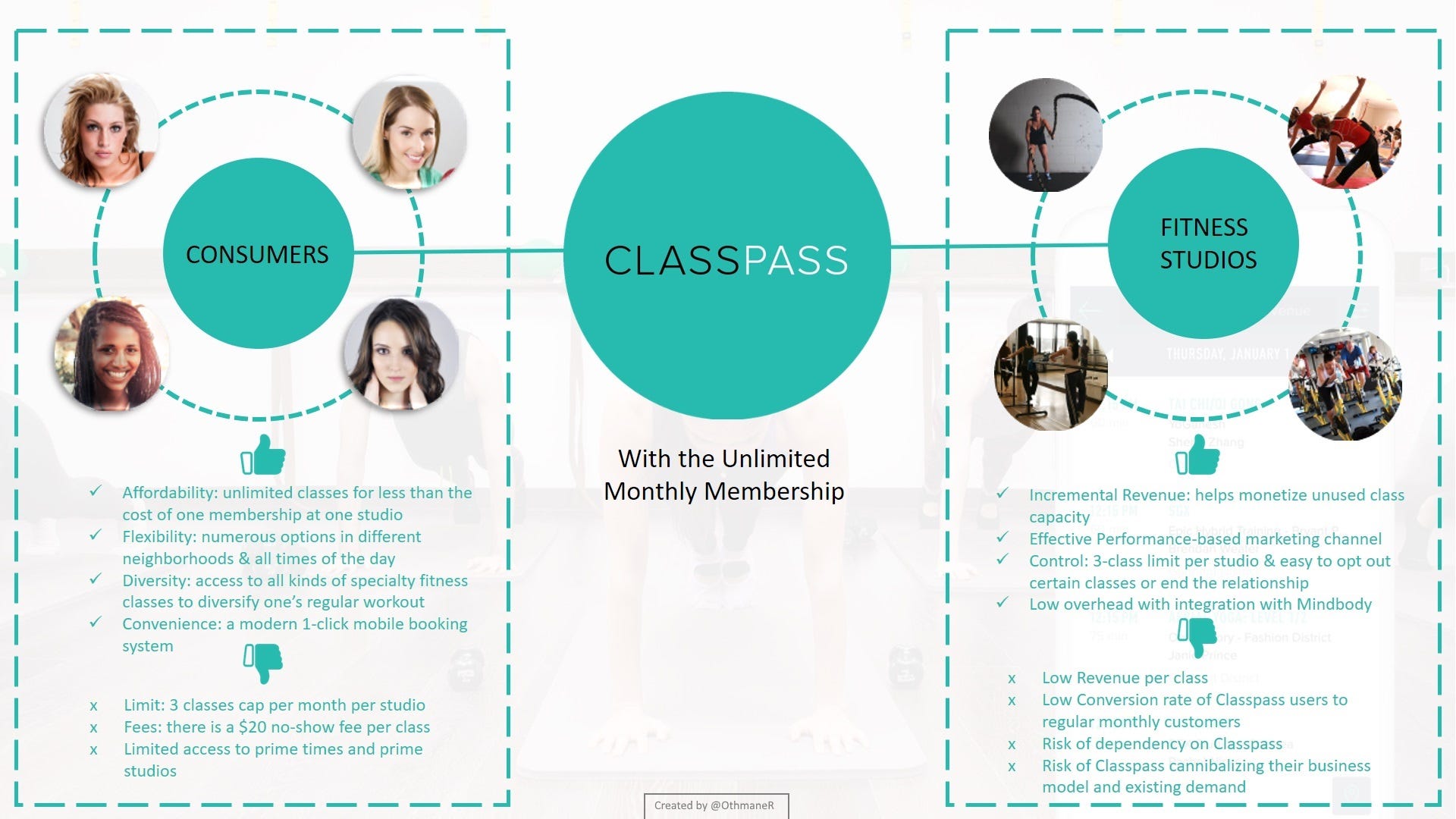

The History and Evolution of Classpass and its value proposition to consumers and fitness studios!

Both sides of the fitness marketplace had unmet needs which Classpass ultimately helped address. Before “Classpass became Classpass”, the founding team struggled to get traction and get consumers to care and adopt their offering. Before rebranding to Classpass, the company was known as DabbleNYC and then Classtivity and their main product consisted of a web portal that aggregated class schedules from different studios. They provided the ability for consumers to book classes through their web portal. It is not until they started offering a 10 class pass for $49 which evolved to Passport — a monthly subscription that typically cost $99 enabling consumers to attend as many classes as they want each month with a cap of 3 visits per studio per month — that they found product market fit. Once they did, the team was able to raise a whooping $82 Million dollars within a period of 14 months to fuel their growth. It consisted of a geographical expansion from 2 cities to over 35 cities and an aggressive customer acquisition strategy with special low priced trial offers for the first month marketed with a significant spend on digital advertising especially on Google Search Ads and Facebook Ads. Over this period of time, Classpass also launched an iOS and Android version of its platform to complement its web portal and grew its monthly revenue by a factor of 50 from around $200,000 per month in early 2014 to over $10 Million per month in early 2016.

The unlimited monthly membership plan was the magical silver bullet that helped create the hockey stick shape of the growth curve of Classpass. The startup offered a strong value proposition for both, consumers and fitness studios, positioning it as a better solution than Groupon to both sides of this 2-sided marketplace.

With the unlimited monthly membership, consumers were getting access to dozens and even hundreds of different studios in their city. They could pick from all kinds of different fitness classes each month enabling them to diversify their fitness regimen. With the number of classes available each day, consumers were no longer restricted to a limited schedule and class availability at one location. They could exercise whenever they wanted because a studio somewhere nearby should be offering a class at the desired time of the day they’d like and in any neighborhood in town whether it was close to home, close to work or near a friend one may be visiting, one could even use Classpass when traveling to another city. Getting access to these classes was convenient and made easy through the web portal at first and eventually through a dedicated app on iOS then on Android. With the integration with Mindbody (the dominant software system used by a large portion of fitness studios in the US), consumers could have a smooth experience once they showed up at the studio. What used to take 10 minutes of paperwork with Groupon in the past, was now all automated through software. There were a few things however that Classpass users did not like such as the monthly 3-class cap that restricted consumers from visiting the same studio more than 3 times per month and the fact that there is a hefty $20 cancellation fee if they don’t show up for a class they registered for. Finally, an issue that has become more of a problem over time is the limited availability of classes to book at prime times. The number of Classpass users which grew over time started competing for a declining number of spots that were made available by studios in their classes at busy times at the most popular local fitness studios.

When it came to fitness studios, Classpass created a new revenue stream and marketing channel that is performance-based with no upfront cost which often generates hundreds and even thousands of incremental dollars of revenue per month to fill capacity that was often left unused in studios. It provided the opportunity for new customers to discover the studio or potentially their type of fitness for the first time and they’d get the opportunity to pitch them on the memberships available at their studio, though not many typically dropped their Classpass membership for a more limited studio membership.

Classpass worked seamlessly with the software system they used to manage their studio and created very limited overhead for them while enabling them to restrict which classes were available to Classpass users or the number of Classpass users allowed per class. This level of control which was introduced over time helped strengthen the relationship with studios which could opt out of the relationship at any time. When talking with fitness studio owners, you’d often hear that they wish they’d receive a higher revenue rate per class from Classpass (it is my belief that some do manage to negotiate higher rates) but, they are often worried and skeptical of these 3rd party “middlemen”. These companies significantly challenge their business model and ultimately capture a slice of the pie by being an intermediary between consumers and providers without always making the pie bigger and therefore resulting in less overall revenue to be shared among the fitness studios.

2016 was a turning point for Classpass as they raised prices for their unlimited plan before eventually eliminating it completely and only offering monthly class passes based on a specific number of classes that can be taken each month, either 3–5 or 10 classes with the option to buy add on classes each month. This major shift in the Classpass business did not impact the “supply side” of the marketplace and the existing relationship between Classpass and the fitness studios. It only impacted the “demand side” and many existing customers were pissed off and very vocal about it online. Classpass was seeking to become more profitable and to do that it had to let go of its “super users”. Who were these people? A segment of its users that were “exercising too much” and generating much more cost for them than what they paid each month through their monthly membership. Classpass lost one of its major appeals for these super users: “affordability”. It made however Classpass more affordable for those who typically only exercise about once a week. Even with this change, Classpass appears to be continuing its growth.

Understanding the Classpass business model

While there was a large online outcry of loyal Classpass customers that took to social media to complain when Classpass decided to raise its monthly membership cost and eventually to completely eliminate it, from a business bird’s eye view, it was the right thing to do. In order to understand the Classpass business model with an unlimited monthly membership, one has to understand how Classpass pays its studio partners combined with the behavior of its users and the number of times they attend classes each month. Given a certain number of users per month, Classpass has a precise fixed revenue based on its set membership cost but a variable cost structure given that it pays its studios per class attended.

Classpass negotiates the rate it pays to studios individually. Their standard formula is to look at the cost of a 10 class pass at that studio and then set its per class pay rate to 50% of 1/10th of that cost. As an example, in Seattle the average 10 class pass cost at studios is around $150. This means that Classpass would typically agree to pay studios who charge that rate $7.50/class. Studio owners are typically reluctant to speak about how much they get paid per class from Classpass as their contract prevents them from doing so. But it is my belief/understanding that they may pay less or more depending on the negotiation. In theory, Classpass should aim to pay as little as possible to improve its margin while keeping its studio partners happy. And at the same time it may decide to pay a little bit more to attract more strategic fitness partners that would help it attract more consumers and keep the demand side happy.

The more active Classpass users end up being, the less money Classpass makes as its payout to studio partners ends up increasing. The average Classpass user ends up going to 1 to 2 classes per week on their unlimited membership. In Seattle, the unlimited membership cost was $79 per month, this means that Classpass gets to keep $49 per user after it pays its studio partners if that user only goes to class an average of once a week: a 62% margin for this segment of their user base. Following the same logic, a user who goes to class twice a week ends up incurring about $60 of costs to be paid to studios resulting in $19 left for Classpass each month or a 24% margin. The problem however is that for users who are more active that than and who may go to classes 3 or 4 times a week or even daily, this can be a big problem for their balance sheet as they’d be incurring more costs to be paid out to their studio partners than what they pay each month. A Seattle Classpass user who pays $79 per month and ends up going through a “30 day challenge” attending a fitness class each day for 30 days would end up costing Classpass $225 in payouts to studio partners or a $146 loss that month.

Classpass aims to get its members to be active and live healthier lives through exercise. The more successful they are in doing that, the more it would hurt their bottom line with an unlimited membership model. Furthermore, such a model creates variability in monthly profitability and unpredictability over time as they are subject to seasonality (people attend a lot more classes in January). One extra class per user per month can mean the difference between making money and breaking even. In other words, one extra class per user per month beyond that could mean bleeding money and going out of business over time. This “unlimited model” only works if there are enough under-utilizing members to subsidize the over-utilizing ones (Just like the traditional Insurance model).

While the unlimited membership model proved to be a priceless “marketing strategy” to grow by a factor of 50 in 2 years, it just was not sustainable in the long term. Classpass therefore had to make a major pivot by sticking with a monthly ongoing subscription at different price points for a specific set number of classes per month: i.e. either 3, 5 or 10 depending on the plan. The pricing for these plans vary per city but in Seattle for example the cost is $30, $50 and $89 per month. With this new model, Classpass gets to keep between 16% and 25% of the monthly membership fee each month for each one of its users after paying its studio partners. This change results in many benefits to Classpass: no more unprofitable customers that could drain the balance sheet by attending 3+ classes per week. This meant a reduction in potential churn from subscribers that were under-utilizing their monthly memberships with a lower priced option for them, and no more conflict of interest between wanting users to be more active and the fear of losing money as a business. The best part of this new model is that by design asking people to prepay for a specific number of classes per month inherently results in “wasted unused classes”. Each prepaid class that the company does not have to pay its studio partners for results in increasing their profit margin even further.

So, how well is Classpass doing in 2017?

Well, It is hard to tell without seeing some key operational metrics that tell the real story such as the cost per acquisition (CPA), the lifetime value of customers (LTV) and the user churn rate (CR).

My “guesstimate” based on all the public data that was disclosed by the company over the last few months and their potential growth trend, Classpass is likely generating around $12-$15 Million in revenue per month with around 1–1.5 Million bookings per month. The rate for their Go/Base/Core plans vary per city and it is not clear what the distribution of users amongst the different plans is but some quick back-of-the-napkin-math with some high level educated assumptions indicates that Classpass probably has around 200k-250k monthly subscribers.

While Classpass does generate some additional revenue from No-show fees and a small commission from add-on classes. The core of their revenue comes from monthly memberships. With the new plans, depending on the plan selected by a user, Classpass is taking a 16%-25% cut on the monthly plan cost which I am assuming would average out to be about 20%. This means that they would end up having to pay out about $9.6-$12 Million to their 8,000 studio partners for all the classes sold to their users leaving them with a Net revenue of about $2.4-$3 Million. The beauty of their new class packages is that, monthly memberships are imperfect by design and they force users to commit and prepay for a certain number of classes each month regardless of whether they end up using them or not (without super-users offsetting this desired imperfection). Classpass users just like in traditional gym monthly subscriptions are likely to over-estimate how often they will actually end up going to classes because people get lazy, they get sick, they go on vacation and so on. Classpass only has to pay studios for the classes its users actually end up taking. My assumption is that Classpass users would end up on average using 80% of their class packages (if users pay for a 10 class pass, they will likely average about 8 classes per month resulting in 2 classes that Classpass does not have to pay the studios for). This 20% inefficiency would potentially translate into doubling Classpass’ monthly net revenue This means that the company is likely making $4.8-$6 Million net revenue each month after paying studios. This translates to about $24 per user per month.

So, is that good? Maybe, again it depends on their CPA/LTV/Churn rate metrics. Over the last few weeks, they have been running Facebook ads for 70% off the first month with the 5-class Base membership. At an average cost of about $50, the company is willing to get paid only $15 for the first month even though they are likely paying out about $30 to the studios for the classes this user is likely to take that month (4 out of 5). Let us assume it takes Classpass an additional $9/user in marketing spend in social media ads to get someone to sign up for this trial, this means that Classpass would take a $24 loss the first month to acquire a customer. They’d be able to recoup that cost the 2nd month and start making money from the 3rd month on. So, if the average Classpass user ends up staying with Classpass for just 2 months, it could be a big problem. However, if the average length of the membership ends up being 6 months or longer, then the Classpass model becomes a lot more interesting financially.

The important question is whether Classpass is profitable. Is it? Let’s try to guesstimate what their other costs are. The Company has about 200 employees mostly in New York City and in the Bay area, assuming the average yearly employee full compensation is around $120k. Classpass needs about $2M to cover payroll each month. Classpass is also incurring about $750k-$1 Million per month in Mindbody Fees assuming 3/4 of Classpass studio partners use their software as Mindbody charges $10/studio and $1 per class booking to use their API (unless they have a special deal negotiated with the company) . Classpass is also likely incurring another $300k-$375k in payment processing fees assuming a rate of 2.5%. This adds up to around $3-$3.3 Million. This leaves around $1.8–2.7 Million for Marketing, taxes, legal, training, office space, software subscriptions and other miscellaneous expenses which I am guessing are likely adding up to be somewhere in the $1-$2 Million range. This means that Classpass should be in the black.

Classpass raised $40M in their last round in November 2016 and they likely still have 10–20% of it still left in the bank which means that with this assumed cushion and the fact that they are likely profitable. Classpass is in a pretty good spot, the key at this stage is to continue to scale by growing its user base and increasing the lifetime value of its customers.

The math above is very high level and full of assumptions and guesstimates and the final numbers and conclusion could end up being completely off if the initial numbers and assumptions based on which the reasoning was done end up being off (garbage in garbage out). But it hopefully helps in understanding the dynamic of the balance sheet of Classpass.

The Challenges and Risks faced by Classpass in 2017 and beyond

Challenge/Risk #1: Losing Execution Momentum

Startups like Classpass who are venture backed technology companies should be growing or they die. I believe that Classpass needs to maintain their growth over the course of the next 6–12–18 months and multiply their revenue by a factor of 3 to 5 to set itself up for another potential Series D funding round at unicorn valuations and to put itself in the path to potentially have a solid public offering. The challenge is that there are many things that can go wrong during this period of time and lead it to lose momentum and fail to maintain growth. 2016 was the year Classpass replaced its “fast growth engine” with a new and better “profitable engine”. Classpass needs to crank up this new engine and pick up pace to make it through the finish line. With the CEO/Chairman role swap between Payal Kadakia and Fritz Lanman, Classpass changed the main operator piloting this new engine but it is key to keep the momentum and get the 200+ employee startup to continue moving quickly and innovating to keep the steam going.

Challenge/Risk #2: Becoming “just another Groupon” in the eyes of consumers and studio partners

Classpass is valuable to consumers if whenever they open the app to book a fitness class, they can find a class that matches their needs in terms of location, type of work out and quality. Back in 2014–2015, Classpass was very aggressive in terms on on-boarding new studios especially as they expanded to new cities. They would aggressively court the best studios in town by offering more generous per class rates and even offer sign up bonuses worth thousands of dollars to get exclusivity in their competition against Fitmob (before they ended up acquiring them). Once the top studios are on board, it is often much easier to convince tier 2 and tier 3 studios to follow and join Classpass too. The problem for Classpass is that tier 1 studios are typically strategically-located busier fitness studios that offer a superior and often differentiated service in their market and they are not as desperate for the incremental revenue Classpass may provide as other tier 2 or tier 3 studios would be.

This mirrors in certain ways the relationship of these tier 1 studios with Groupon: they have either never even tried it, they have either dropped it a long time ago after trying it for a short period of time or they only use it in a limited way allowing a very specific number of users through with many restrictions. These tier 1 studios greatly value their studio’s brand and they aim to maintain a superior perception level for their fitness studio. They do not want to be perceived as a value studio (They want to be Nordstrom not TJ Maxx). They are typically willing to offer a discounted rate for a trial period but they want to close any loopholes that would allow anyone to benefit from taking advantage of their service without paying the high rate they expect. Classpass just does not pay them enough per class so they end up either completely dropping Classpass or only keeping on Classpass their “least busy classes” at times that are often inconvenient for consumers. Classpass provides them with additional exposure for their studio while protecting themselves from the risk of having the company cannibalize their existing demand. With this strategy, given the quality of the service they offer and their brand appeal for consumers, these studio are more likely to convert Classpass users to regular studio members and having them drop their Classpass membership than the other way around.

If too many tier 1 studios drop out or a keep a limited number of classes on Classpass, monthly subscribers feel the pain and the monthly Classpass membership can lose its appeal. It is very likely that Classpass users naturally tend to pick tier 1 classes first (best location, best teachers, best amenities) before picking classes at tier 2 and tier 3 studios. With the per-location limit already in place with monthly subscriptions, Classpass users need enough tier 1 studios on the platform so they can distribute their usage amongst enough studios they like, while still feeling they are getting a good deal. There are 2 big problems that can emerge as a consequence of this which can cause significant user churn over time:

- Classpass users will fail to find classes that match their needs when they open the Classpass app because the best inventory is retracted or is no longer there. It is not just about quantity of studios and classes, quality is key too. (Think about the user experience of browsing through Netflix for 15 minutes without being able to find a movie you like).

- The quality of classes available on the platform will drop as the only inventory available will be from tier 2 and tier 3 studios: if you experience enough classes at studios with sub-par instruction, average teachers, dated facilities… the Classpass membership will lose its appeal over time. (users don’t like to get “the bottom of the barrel” and ultimately end up willing to pay more for the ability to get first pick from the barrel)

Classpass needs to ensure that it maintains a certain level of quality in its supply to avoid becoming the next Groupon in the eyes of its consumers and ultimately only attract the price-sensitive ones who are just looking to get a deal which would drastically limit the revenue potential of Classpass.

Challenge/Risk #3: Failing to build a new band of loyal Classpass fans

There is no doubt that during the “Unlimited membership” phase, Classpass had an army of loyal subscribers that were taking to social media and blogs to preach its greatness and their love for the company, helping fuel its growth. These advocates were typically super-active fitness lovers that saw in Classpass the perfect solution they never dreamed about. They could work out whenever they wanted, wherever they wanted, at the best fitness studios in town for less than the cost of access to just one facility. This audience loved it so much that they took full advantage of it by attending classes many times a week and even every day. These loyal fans were the ones that got burned by Classpass in 2016. They were emotionally vested in the company, they posted photos of themselves on Instagram after each work out with the hashtag #Classpass, they recommended the membership to their friends, they convinced all their friends to sign up and tag along to the next class… and…. how did Classpass pay them back for their loyalty and advocacy efforts? They significantly increased the price of the unlimited monthly membership they loved so much before completely taking it away. When Classpass announced the price hike, they lost 10% of their user base. They did not just lose thousands of subscribers, they lost their most loyal fans, they lost one of the main fuels of the Classpass growth engine.

Classpass needs to replace these loyal fans with new ones and the key to making that happen is delighting customers with their product and service. It seems however that Classpass is not doing a great job on this front. After overcoming the PR nightmare of 2016 i.e. dealing with all the pissed off superusers that Classpass “fired as customers”, there seems to be a fair amount of dissatisfaction building up due to the lack of supply in the marketplace and poor customer service. A great way to get a feel of that is to read through recent reviews in the App store/Playstore for the Classpass App. Its reviews sound like they belong on the Yelp page of a $15/month cheap neighborhood gym with expressions like “bait and switch”, “fees”, “impossible to cancel”, “buyer be warned”.

Challenge/Risk #4: Being crippled or disintermediated by the frenemy Mindbody

Mindbody, a public company based in San Luis Obispo CA, is a key player for booking, scheduling and backend software systems for boutique fitness and wellness studios. The company started back in 1998, they went public in 2012 and they had about $38 Million in revenue this last quarter which they earned by selling a Saas solution to over 60,000 fitness and wellness studios all over the world with rates ranging from $45 to $245 per month. About 60% of their revenue comes from their monthly subscriptions while most of the rest comes from payment processing. Mindbody is the elephant in the room for this industry and they are both a partner and a competitor for Classpass.

The Classpass technology is deeply integrated with the Mindbody system through APIs. Classpass is able to keep the information in its system up to date when it comes to the studio’s schedule and teacher information because they can programmatically obtain that information from the Mindbody system for each one of their 8,000+ studio partners which happens to use the Mindbody software system (the large majority of them do). Without it, Classpass would have to incur a significant amount of human/manual overhead to keep that information up to date and it would require studios to notify them or update their system whenever they decide to cancel a class, change the schedule, change the teacher for a certain class, etc. Furthermore, when a Classpass user registers for a class, they are able to programmatically add that person to the studio’s Mindbody system so that the studio owner can expect that student in their class and that user can have a smooth check in experience. This integration is what makes it possible for Classpass to partner with 8,000+ partners in 39 cities without requiring a large support organization and any additional ongoing work from studio owners. This benefit however does not come for free as Mindbody charges Classpass and any other partners who want to use their APIs: $10 per studio location they work with and $1 per booking in addition to some usage fees depending on how heavy of a utilization the partner’s system puts on the Mindbody servers. Over the last few years, Classpass has processed over 20 million bookings, this means that they have paid out millions of dollars to Mindbody. Fitness studios are paying around $200 per month on average to use the Mindbody software to manage their business and in addition to making money through these monthly subscriptions fees and through payment processing fees. Mindbody is able to generate additional millions of dollars of revenue by charging partners like Classpass to be able to get access to scheduling data for studios and to be able to register students on the studio fitness accounts.

Classpass is heavily dependent on Mindbody and their business would be significantly crippled if Mindbody decides to shut off Classpass’ access to their studio partners’ data or if they decide to significantly raise their API rates. This is a risk that I am sure the Classpass executive team has been thinking about for a while.

While Classpass is a Mindbody partner that generates millions of dollars for Mindbody, they are also a competitor. Mindbody also sees a business opportunity in controlling the demand side of the fitness and wellness market. While they have historically provided a software system for studios to manage their backend, over time they also launched a web interface for each one of their fitness studios that enables their clients to see class schedules and be able to book classes. With the shift of consumers to mobile, they also launched an iOS and Android App that provides the ability for students at a studio to sign up for classes. The Mindbody App has been installed over 3.5 million times as of last August and it enables its users to book classes and wellness services at over 60,000 locations worldwide. The Mindbody App has a user base that is an order of magnitude higher than that of the Classpass App. It ranks in the top 30 in the US Fitness category in the App store according to AppAnnie as compared to a ranking of around 200 for the Classpass App, they also have over 7 times more studios to book classes and services from as compared to Mindbody.

On the surface, it looks like Mindbody is already “eating Classpass’ lunch” but the reality is different. To understand why that is, it is important to comprehend the motivation behind someone installing the Mindbody App vs. the Classpass App and the contributing factors that led to each app reaching its current audience size. When consumers start using the Classpass App (Web, IOS or Android), it is because they are signing up for the Classpass monthly membership and they constitute new demand for the Classpass studio partners. When consumers install the Mindbody App, it is typically because they are already a customer at a specific studio and they are installing the app to easily get access to the schedule of the studio they already go to. Check any studio’s website traffic and you will notice that the most visited page on their website is typically the schedule page but that is only true if they have the schedule from Mindbody embedded on their website (which typically costs extra). So most just end up linking to their schedule page on the Mindbody web application. This means that a significant portion of the dozens, hundreds and sometimes thousands or customers each one of its 60,000+ Mindbody clients has, would end up on the Mindbody portal on each studio’s respective schedule page. These likely add up to millions of page views every month and if you happen to visit these pages from a mobile device which is likely over half of that traffic, you’d be prompted to install the Mindbody App. This is in my opinion what has primarily contributed to having millions of users install the MindBody App. Another factor is that studio owners also started telling their students to install the app to get access to their schedule as Mindbody was encouraging them to. While some students do preregister for classes through the Mindbody App especially at locations that are very busy and where spots are limited, the very large majority of users only use the app to look at the schedule at the specific studio they attend. I suspect that only a small portion of these users end up ever using the app to use the services of other studios.

Ultimately, Mindbody does not generate any or much revenue from the demand side but that could change if they decide to. All the signals indicate that they may be going in that direction, which means they could be competing directly with Classpass. They could in theory dis-intermediate Classpass by offering a similar or better offering that could compete directly with them and potentially be even more appealing to studios especially if they end up taking a smaller commission.

While Mindbody may pursue such a strategy, it is worth noting that they are a much bigger organization and a lot less agile in terms of execution which means they move much slower. Going after the Classpass business could also be risky as it may negatively impact its relationship with its core customers on the supply side of the marketplace: the studios. It is likely that they would pursue this strategy through an acquisition and potentially maintain the company’s brand separate as they position themselves to go after the demand side of the marketplace.

Challenge/Risk #5: getting out-innovated by the next startup

Besides Classpass, there are multiple startups seeking to capture the heart and minds of the fitness industry by creating a 2-sided marketplace that enables consumers to book classes at local fitness studios. This is true both here in the US and overseas. These include Fitreserve which operates in NYC and Boston, Zenrez which operates in 6 cities and just closed a 6 Million funding round this month, Lymber Fitness operating primarily in California, Studio Hop Fitness in Texas and Oklahoma, OpenSweat in the LA area. When it comes to international players, here are some of them: SoMuchMore in Europe, Kfit in Southeast Asia, Fitpass/Fitternity/BookYourGame/FitmeIn in India, GymforLess in Spain, GuavaPass in Asia and the Middle East, UrbanSportsClub in Germany, PayAsYouGym in the UK and many others.

There are also many players in adjacent markets such as tech companies focused on helping consumers book personal trainers near them from their mobile device. Others focused on corporate wellness, some on fitness wearables and yet others on exercise tracking… Any of these startups could get significant traction in the coming year and could come up with a better way to scale and grow and a stronger value proposition for consumers and fitness studio owners to ultimately challenge Classpass in its quest for dominance of this market.

Another key player to watch here is MyFitnessPal. Few months ago, they started a strategic partnership with Mindbody and provided millions of MyFitnessPal users access to fitness classes from Mindbody directly on the MyfitnessPal app without having to go sign up each studio individually (which Classpass had to do with its 8,000 studio partners). This on its own could drastically reshape the marketplace. I have not seen any other announcement about it since November when I tested it on my phone but, it appears that this capability has been disabled in the latest version of the MyFitnessPal iOS App — I am not sure if this is an indication that they have discontinued their relationship.

Finally, I personally think that a pay as you go model with dynamic pricing is the best solution for this marketplace to best serve the needs of consumers while also maximizing yield for fitness studios. It may take time but I believe that the industry will eventually converge towards this kind of model and the marketplace would start looking like the travel industry with aggregators like Kayak/Travelocity/Expedia, etc serving as better search engines for the supply (flights, hotel rooms etc.) with consumers only booking the classes they use with no waste from subscriptions. Different studios will charge different rates based on the value of each one of their classes in the marketplace. Startups are best positioned to make this vision a reality and whoever does will challenge Classpass in a significant way and would become an acquisition target for both, Mindbody and Classpass.

The Opportunities that Classpass could and should be taking advantage of

Opportunity #1: Build a growth engine to take over the fitness marketplace and serve its different sub-segments

While Classpass has experienced some significant growth over the last years, they have only captured a small fraction of the fitness marketplace. With an estimated 200k-250k users spread across 39 markets, this means that they likely have somewhere between 1,000–10,000 subscribers in any given market with NYC likely being an exception given its population size, and the fact that Classpass has operated there for years. Classpass targets large metropolitan areas with populations in the millions or hundreds of thousands. This means that there is a lot of room to grow and a lot of potential customers that could become Classpass users if the company can figure out ways to serve their fitness needs and market to them effectively. There are 3 functions that are key to make that happen and Classpass should ensure that it has a strong team of “rock stars” in Product Management, Engineering and Product Marketing/Growth to power up its growth engine.

Now that Classpass has settled on its new pricing and business model, it is important to understand what their target consumers really want and continuously improve its product and its technology to better serve their needs, and then deploy its marketing team to drive the growth especially as it considers new sub-segments of the fitness market. Classpass should be looking at serving others beyond just those interested in group fitness classes, such as:

- people interested in gym passes to lift weights or get access to cardio equipment to do their own work out

- those interested in booking private sessions or in hiring a personal trainer

- those interested in finding and booking more advanced fitness workshops that their studio partners already offer

- those interested in signing up for a fitness competition or a race

All of these segments provide opportunities to enable new revenue sources for the company and increase its average revenue per user by up-selling additional fitness services or products to its existing user base.

More importantly, Classpass needs to make its product more sticky and build the loyalty of its users once they join Classpass with the key objective being the maximization of the subscription length of its members. One way to accomplish that could be for Classpass to invest more in enabling social experiences and a sense of community within the app:

- creating opportunities for Classpassers to coordinate going to classes with their friends and seeing which classes their friends are going to.

- Enabling ways for their users to make new friends and to find new work out buddies.

- Hosting more events and fitness activities such as group runs or hikes for Classpassers to meet each other.

- Gamifying the experience for people to compete with their friends or with the broader community to meet certain fitness goals.

- Joining with others to participate in races such as marathons and obstacle courses. Etc.

The key is to fulfill the basic human needs for connection within their user base and making Classpass the enabler for that within the context of fitness.

Opportunity #2: Dominate the Fitness market both offline and online

Another area of opportunity for Classpass is online fitness. This could provide a chance for the company to increase its revenue per user by up-selling its subscribers an add-on to their subscription to get access to video-based fitness classes that can be streamed online from their studio partners or on-demand through the Classpass App. There are some existing players in this space such as Grokker or Cody App but Classpass should seriously consider going after this opportunity sooner rather than later whether they decide to build their own solution, partner with one of these players or enter this market through an acquisition.

Opportunity #3: Going after the 80% of consumers who do not typically exercise actively

So far, Classpass has really just served those who are already interested in exercising and are motivated in going to fitness classes. For every person who fits that description, there are likely another 3 or 4 people who are considering exercising, becoming healthier, losing weight, etc. But they are not taking any concrete actions to do so. These are the people who may get a free membership at a fitness studio through their employer but they rarely or never take advantage of it. These are the people that typically have a new year resolution focused on wellness and fitness yet consistently fail in meeting their objectives each year. If Classpass can provide an effective solution that can help people get moving and exercising regularly and meet their fitness objectives, then they could be in a position to “cross the chasm” from the early adopters who are already into fitness to the mainstream consumers, who with Classpass, may be starting to exercise regularly for the first time in their life or in a while. This is not an easy endeavor but doing it successfully can translate into a significant revenue opportunity.

Opportunity #4: becoming a lifestyle company expanding to other local services beyond fitness

One of the natural expansion opportunities for Classpass is to go beyond the fitness vertical to provide its members the opportunity to get access to other local services especially in the wellness space with new add-on subscriptions such as manicures, massages, haircuts and other wellness services. This could help significantly improve the revenue per user that Classpass captures by making a commission on multiple other services their users may be interested in.

Classpass could then expand beyond that to other verticals such as group activities, entertainment, dining, etc. I personally believe that in the next 5–10 years a new player will emerge to be the Amazon of the local services industry. Similarly to how Amazon has become the one-stop shop where you can easily buy anything and get it quickly shipped to your house hassle free in a couple of clicks, I believe that the local market is ripe for a player to dominate the market by providing consumers with a seamless end-to-end experience to find book and get access to all the local services around them at the best prices (Think beyond just looking at reviews on yelp but a true local marketplace to book services and appointments at the best prices with all the information you need to make a decision all in one place with great UX). It may be far-fetched but Classpass could be in a position to horizontally expand to different verticals to become that company: the one digital stop for users to book all their lifestyle services.

Opportunity #5: going after the employer fitness benefit and Corporate Wellness opportunity

Classpass is well positioned to take advantage of the fact that they have established relationships with thousands of fitness studio partners by offering a more customized fitness benefit to employers. According to the IHRSA, about 36% of employers in the US offer a fitness membership subsidy or reimbursement. Classpass could generate millions of dollars in revenue by offering a solution that would both cut operational costs for HR department and provide a much more appealing benefit for employees than “just a standard membership at one fitness facility”. This would open the door to employees to exercise whenever/wherever they want — in their city or while traveling — within the Classpass network while the employer is picking up the tab. There are a few companies going after this opportunity such as PeerFit but, Classpass could easily dominate this market if they pursue the opportunity sooner rather than later.

Another great potential opportunity for Classpass to pursue is in corporate wellness. This industry has been growing quickly as more and more employers and insurance companies look at corporate wellness programs offered by companies such as Limeade, Aduro, Wellness IQ, Sonic Boom Wellness, etc. As a way to reduce their healthcare costs and boost their employees productivity as healthier employees end up being less stressed, take less sick days, etc. Classpass could partner or build its own wellness solution by providing employees of client companies a sort of digital wallet similar to the concept that the Canadian company The League offers with a balance which they can redeem within the Classpass network.

Opportunity #6: disrupting Mindbody by offering a free or low priced Saas software solution

Similarly to how Mindbody is looking to expand from the supply side of the marketplace to establish new revenue streams from the demand side, Classpass could be looking to do the reverse by offering either a free or low cost solution to fitness studios to compete against Mindbody. This would likely happen if the relationship between Classpass and Mindbody is strained and it could be a good counter-attack move if Mindbody starts to aggressively compete against Classpass. Google did something similar when it launched Android to disrupt the mobile marketplace to “commoditize” the operating system stack (where its main competitors Apple & Microsoft have an edge and generate their core revenue) and “bring the fight against the competition to its turf”: the actual apps where it is stronger and better positioned to win (search, google maps, Gmail etc.). Classpass could compete on price with Mindbody to offer a “good enough” SaaS solution for most studios to be able to run their studios at a much more cost effective rate and focus the “fight” on the customer acquisition game where it is stronger and better positioned to win.

While this sounds dramatic, it was a strained relationship with Mindbody that ultimately led to the formation of Frontdesk, one of the main Mindbody competitors based in Seattle. I remember sitting for coffee in the spring of 2015 with Jon Zimmerman, one of its founders (who sadly passed away last year), to hear about his experience working with Mindbody as my team was actively working on integrating the Yoga Panda system with Mindbody APIs. He ended up having to shut down his previous startup “Skilled Athlete” because Mindbody shut down his startup’s access to the Mindbody APIs rendering his startup dead overnight. If Classpass gets its Mindbody access cut off, it would be significantly crippled.

So is Classpass the next unicorn or the next bust?

After these 9,000 words of in-depth analysis of Classpass, I think we are in a better position to have an educated opinion about the potential future of this startup.

Overall, I think that Classpass is in a good position to capture some of the opportunities highlighted above but, it will definitely require proper execution in addition to mitigating the risks mentioned earlier. I am therefore optimistic about their outlook and foresee them continuing their growth over the coming years and potentially becoming the next Unicorn.

That’s my opinion but what do you think? Does this all make sense? What did I miss? Was it useful? Let’s get the conversation started. So please let me know what you think and invite anyone else who follows and cares about Classpass specifically or this industry and topic to join us for this conversation.