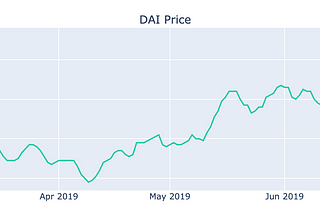

Primoz KordezMeasuring DAI Supply and Demand Price EffectsAt the time of this writing, DAI price has been hovering around 1 USD for about 3 months, but in the last few weeks we’ve seen a lot of…Aug 30, 2019Aug 30, 2019

Primoz KordezMakerDAO Stability Fee BenchmarkingCurrently, there is a lot of debate over whether the stability fee as a policy rate for borrowing DAI and backing it with ETH properly…Feb 25, 20191Feb 25, 20191

Primoz KordezinGood AudienceDecentralized Asset Management — A Utopian Dream?When I used to help Iconomi with building their fund management platform I always wondered if decentralized asset management on the…Jan 14, 2019Jan 14, 2019

Primoz KordezinSquared CapitalImminent Firesale of ETH held by ICOs?Crypto markets have taken a continuous beating since the beginning of the year. The whole crypto market lost 75% of its value and the…Aug 22, 2018Aug 22, 2018

Primoz KordezinSquared CapitalGo-to-market Strategy of StablecoinsCrypto industry experts spend much of their time studying which stablecoin may become adopted and the set standard for stable transaction…May 23, 20181May 23, 20181

Primoz KordezinSquared CapitalSkin in the Game of Centralised MiningLast week a research firm Bernstein published a report stating that the Chinese bitcoin mining company Bitmain made between $3 billion and…Mar 2, 20181Mar 2, 20181

Primoz KordezTokens Targeted AirdropsIn one of my previous blogs I tried to highlight the importance of the structure of token holders and its impact on token price dynamic. As…Feb 13, 20182Feb 13, 20182

Primoz KordezinSquared CapitalCME Futures, Herd & Volatile Crypto WinterBitcoin $10k! For those of us who have been in crypto for some time, such a headline was something we all somehow expected to happen sooner…Dec 1, 2017Dec 1, 2017

Primoz KordezinSquared CapitalHow the Behavior of Token “Hodlers” May Create VolatilityIn my previous article, I touched on the problem of token holders, who consist of either actual users or investors. As shown, the activity…Sep 29, 20175Sep 29, 20175

Primoz KordezinSquared CapitalNetwork Output and Velocity of TokensWhen the crypto community is blinded with ICO hype, there are few attempts to determine the best methods for evaluating cryptocurrencies…Sep 4, 20175Sep 4, 20175