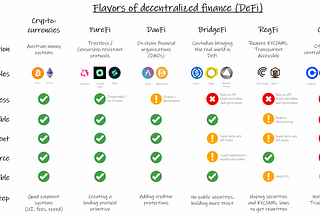

Sébastien DerivauxAlmost 50 flavors of crypto financeWhere suggest here a nomenclature of crypto-finance project to understand what decentralization mean.Feb 17, 20231Feb 17, 20231

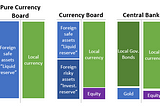

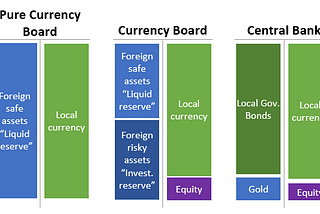

Sébastien DerivauxStablecoins and currency boardsRethinking MakerDAO value propositionNov 5, 2022Nov 5, 2022

Sébastien DerivauxStablecoins: currency or credit?In this article, we will analyze the difference between money-like credit and a currency. Then we will try to understand how such a…Sep 25, 20222Sep 25, 20222

Sébastien DerivauxHow the crypto-banking system could reduce systemic riskThis article shows that liquidity pools, a basic construct of DeFi could create a more robust financial system by improving assets…Sep 8, 2022Sep 8, 2022

Sébastien DerivauxThe Crypto Banking SystemThis article dives into the foundations that are needed to build a financial system on top of decentralized finance (DeFi). While there is…Jul 6, 2022Jul 6, 2022

Sébastien DerivauxCrypto-banking differences with traditional and shadow bankingAnd do we need fractional or full-reserve banking in crypto?Jun 19, 20221Jun 19, 20221

Sébastien DerivauxCapital structures for DAOs in DeFiStructuring the liability side of balance sheetsMay 19, 2022May 19, 2022

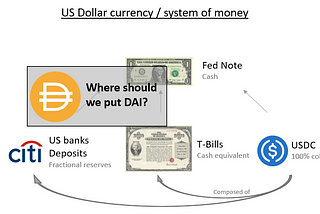

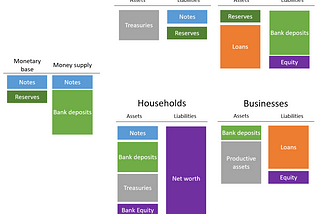

Sébastien DerivauxHow money worksThis article presents a simple and short case on why it is commercial banks and not the Fed that creates money and why it matters for…Feb 28, 2022Feb 28, 2022

Sébastien DerivauxIntroducing ClearingDAO: a decentralized clearinghouse for stablecoinsThis article makes the case of the importance of DeFi stablecoin fungibility and provides initial thoughtsFeb 14, 2022Feb 14, 2022

Sébastien DerivauxThe history of a DAI at par valueStory of the DAI peg since December 2019. What can we learn from it? How did MakerDAO achieve price parity with $?Dec 20, 2021Dec 20, 2021