Are Recessions Rare? Depends On The Definition: Lessons From The Prime-Age Employment Rate

Recessions are commonly defined as real GDP contracting for two consecutive quarters, but this definition is both arbitrary and heavily biased by working-age population growth. If we hypothetically translated that definition to the prime-age employment-to-population ratio, then recessions would appear sooner, last longer, and occur more frequently. Of course, unlike real GDP, the prime-age employment rate cannot increase forever, but as Canada and other economies are showing us, there is still plenty of room for improvement in the US …

In common parlance, we describe recessions as two-quarters of negative real GDP growth. Matt Klein illustrates that real GDP is actually a flawed summary variable for characterizing recessions because it ignores per capita outcomes and glorifies economies solely due to working-age population growth:

“Australia may have the record for missing recessions but it doesn’t have much of an impressive record when it comes to total growth, especially after accounting for the rapid growth of its working-age population.

This is particularly obvious when comparing how much GDP per person aged 20–64 has grown in Australia against Japan and Spain. Both Japan and Spain experienced severe recessions since 2007 and both are often considered economic examples of what to avoid (deflation, real estate busts, and banking crises). Yet Japan has grown 4% more than Australia over the past couple of decades, while Spain has grown almost as much as Australia.”

The National Bureau of Economic Research (NBER), the de facto recession authority in the United States, does not actually use a strict two-consecutive-quarter real GDP definition. It uses a variety of different indicators.

- The 2001 recession no longer fits the two-consecutive-quarter definition. Real GDP was initially reported as having contracted in the second quarter of 2001 but was later revised up sharply a few years later to show that output had actually expanded. Despite the revision, the NBER’s classification of this period as a recession remained unchanged.

- When using a variety of metrics, the methodology naturally becomes more opaque and has scope to take on new biases.

Recession definitions end up being more arbitrary than is generally appreciated. We should never lever ourselves too heavily to a single indicator or a single institution’s description.

But if I were to tie myself to a single indicator… I would probably choose the prime-age employment-to-population (PA EPOP) ratio. Labor utilization rates reflect per capita outcomes, and PA EPOP is certainly better than the headline unemployment rate. PA EPOP is also more timely and less vulnerable to revision than per capita real GDP. The challenge with using labor utilization rates is that it cannot increase forever, but the US still appears to be far from that upper bound, as other economies such as Canada quite clearly reveal

Here’s what it would look like if we flagged every month involved in two consecutive 3-month/quarterly periods of PA EPOP contraction:

Here’s what we see using the NBER definition:

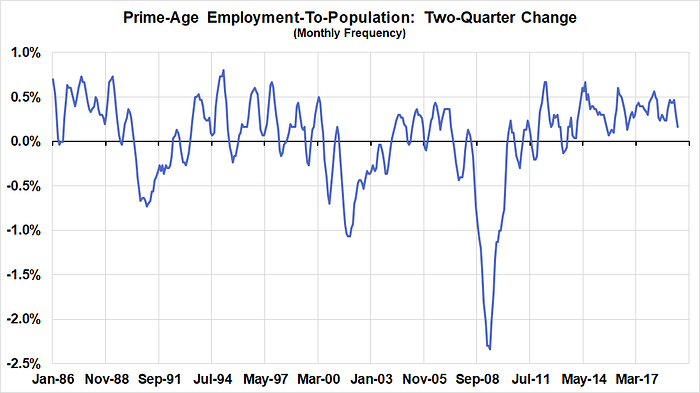

What does the two-quarter change (6-month change in the 3-month moving average) look like for the prime-age employment-to-population ratio? (Keep in mind that data looks more volatile at a monthly frequency)

A few takeaways:

- Recessions should not be treated as simply rare, sparse outcomes. The last three NBER recessions are really just the worst parts of PA EPOP downturns that last 3–5 years. These extended PA EPOP downturns are only occasionally interrupted by periods of PA EPOP expansion. Does the NBER methodology inadvertently cut policymakers too much slack?

- The change in PA EPOP tends to be a leading indicator heading into NBER recessions but continues to decline even after the NBER recession has concluded. In the last three recessions, the underperformance of employment growth has begun many months earlier than when the NBER officially designates the starting point of a recession. The last three recessions have also resulted in jobless recoveries and extended periods when the economy was at risk of a “double-dip” recession due to the precarious state of the labor market.

- Watch PA EPOP now. The 3-month moving average of PA EPOP is currently in a mild decline. Whether this is a blip or marks something more meaningful, we should be focusing more on the implications of slowing labor takeup. Given that aggregate compensation growth (GLI) is also slowing, this does not appear to be capacity-related slowing.