Target’s ($TGT) 2024-Q2 corporate earnings analysis

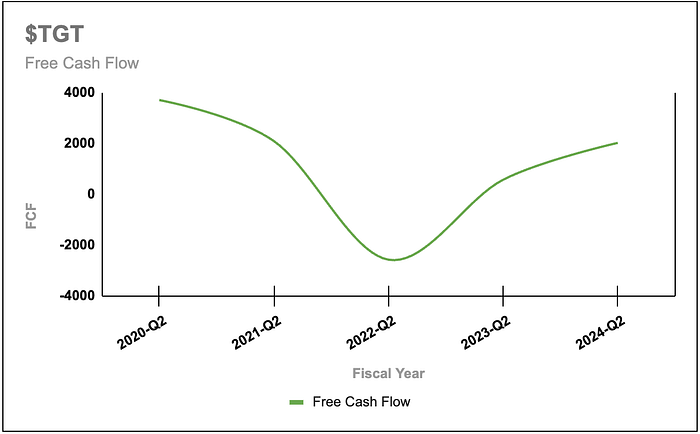

Editor’s Note: a previous version of this article had an incorrect calculation in the model for Free Cash Flow (FCF) and the associated visualization chart. The article has been edited with the correct data.

Link to the Form 8-K through EDGAR

Key Highlights

- Company overall seeing traffic growth and sales growth compared to same period last year

- 463.5M diluted shares outstanding (used for EPS calculation)

- 2024-Q2 revenue increase 2.7% YoY to $25.45B (2023-Q2 revenue was $24.77B), HY2024 revenue down 0.2% YoY to $49.98B (compared with 50.1B HY2023)

- Net income 2024-Q2 $1.19B increases 42.7% YoY, meaning EPS of $2.57 per diluted share

- Future expectations for 2024-Q3 are: didn’t provide revenue guidance; comparable sales increase 0–2%; EPS of $2.10–2.40 (inc. of 0–14%) per diluted share. FY2024 expectations are: comparable sales increase 0–2% (closer to lower end of range), EPS of $9.00–9.70 per share (inc. of 0.9–8.7%)

A look at operating margin

Target directly provides a line item in their income statement for operating income, from which we can see that they are taking out COGS, SG&A, and depreciation expenses out from Total Revenue.

From this data, we can see that Target’s operating income for the latest quarter was about 6.4%, greater than last year’s same period operating margin of 4.8%.

We can also see for the Half Year so far, the company is operating at 5.9%, compared to the half year 2023 margin of 5.0%.

Here, I’m compiling data from former filings to compare same period half year operating margin for the last 5 years:

For the last three years, we see Target is regaining it’s efficiency following a significant growth in 2020–21 (most likely attributable to mass inflation… but this deserves a deeper study to confirm).

This is a good sign from a company that has been struggling for the last year or two, leading to more confidence in a real recovery.

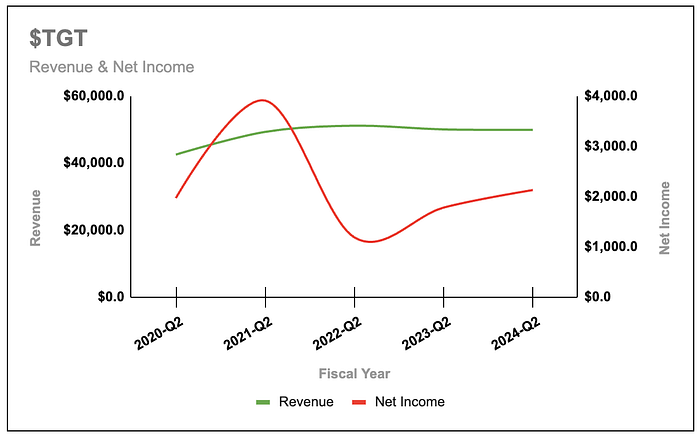

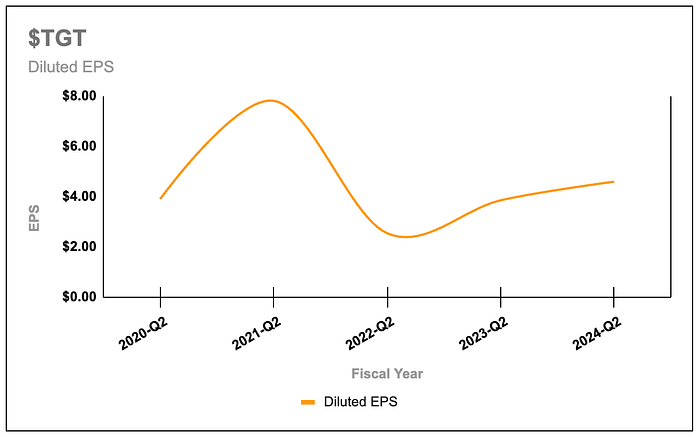

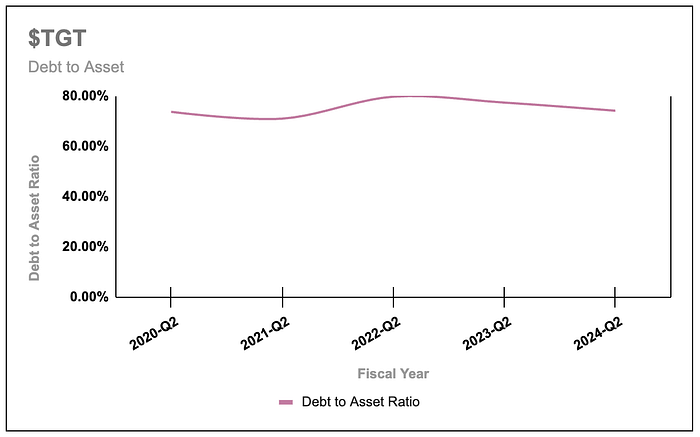

5 Year History

I like to compile data for at least five years when starting a new analysis. And this can easily be added onto as more future earnings are released.

Here is the compiled data on Target earnings for the last 5 years. These are all six-month total data from the start of their respective Fiscal Years.

And the associated charts:

Takeaways from the Data & Charts:

- I do think Target is doing a good job in becoming more operationally efficient over the last three years, while top-line revenues haven’t been expanding as much, that makes sense in this context considering the amount of political turmoil the company had found itself in in recent years, combined with the weakened consumer who is increasingly more apt to seek cheaper shopping options.

- EPS took a significant hit following the 2021 bloat. It is coming back up, but still may be a bit until we see it reach back to those levels.

- Debt to Asset ratios are very high, but they have added a decent amount of assets to their portfolio this year, helping bring the ratio down a chunk. They are running more hot when compared to other industry players such as Walmart & Costco, which seem like overall better businesses as of late.

Final Thoughts

Target will remain on my list of companies to watch out for if and when their stock price takes a hit on news, but barring any significant announcements, this company really doesn’t impress me too much. It’s in an industry with much more attractive names in Walmart and Costco.

Obviously this is anecdotal, but I point to my own experiences with this company during this analysis. Target used to be an “experience” to shop at. It was enjoyable to take a trip when there was nothing else to do, grab a snack at the cafe and window shop for decor and necessities. But over the last few years, my wife and I have really started to hate having to go there, and we typically avoid shopping at a Target whenever we can.

Lack of employee help or visibility, often dirty and unmaintained storefronts, the lack of strong incentives and removal of cash back function of their Circle program, inflated prices that are not competitive to nearby stores, and being more expense conscious in our discretionary budget all factors into this thesis. But, this is just my opinion.

Here is a look at the yearly stock chart for $TGT

While consumer data has been relatively stable as of late, there’s little in terms of growth aspirations to look forward to in Target’s history. I can easily see this company going the way of the likes of Best Buy, Kohl’s or other household named shops from the last two decades. And I think it’s more likely we see years of flat to little growth as we seen in the 1995–2014 range in the chart above instead of aggressive growth seen in 2018–2021.