The Future of Security Tokens

A look beyond issuance and trading of digital assets

Security token offerings (STOs) have received a lot of attention recently due to their unique features as compared to traditional forms of raising capital. The fact that regulators globally are paving the way for STOs as a mainstream form of financing additionally fuels the widespread adoption of security tokens on financial markets. See for instance this article for an overview of US regulations or this article for the regulatory environment in Switzerland.

Meanwhile, the discussion around the benefits of STOs and security tokens currently focuses mainly on the issuance and trade-lifecycle of these assets. On the one hand, this strong focus clearly was necessary for the development of new issuance solutions where, with the help of blockchain and security tokens, issuance and exchange of assets has, technically speaking, become accessible for everyone. On the other hand, by focusing on issuance and exchange of assets only, all other aspects of an asset’s lifecycle have been neglected.

In this article we take a closer look at the lifecycle of financial securities beyond trading and settlement. In particular, we outline important events and processes around the execution of the various obligations defined in a security and the reporting for securities. We believe that these aspects of the securities lifecycle bear a lot of potential for additional automation and efficiency gains through the use of blockchain. Hence, in the future we will see Security Tokens that expose additional features facilitating exactly these lifecycle aspects.

Financial assets

In essence, finance is very simple and the gist of it can be summarized in the following sentence:

“Who owes what to whom and when.”

In other words, finance is about some party A (the “who”) having specific payment obligations (the “owes what”) to some party B (the “whom”) at some future time (the “when”).

The terms and conditions embedding such payment obligations and claims, respectively, are generally defined in financial contracts. A financial asset is then simply a medium representing the financial claims encoded in a specific financial contract such that the holder(s) of the asset, i.e. the investors, are legally entitled to these claims.

This is true for equity, all kinds of lending agreements, futures, options, complex swaps and other sorts of derivatives. While the terms and conditions or, in a more mathematical language, the payoff function changes across these instruments they all express some agreement on future claims. Historically these claims have been expressed in natural language using different legal vocabularies in different countries, markets and across different issuers. This has led to an artificial variety while the patterns of claims encoded remain limited in number.

As a response, the ACTUS Financial Research Foundation started in 2013 with the quest to describe all kinds of financial contracts in mathematically rigorous form. This important work validates the idea of few distinct patterns of encoded future claims as the common ground among all types of financial assets. In fact, the ACTUS system consists of little more than 30 financial Contract Types which capture virtually all financial assets out there. This ground-breaking work allows us to derive a generic model for the implementation and, ultimately, execution of the full lifecycle of all kinds of financial assets.

Beyond the trade-lifecycle

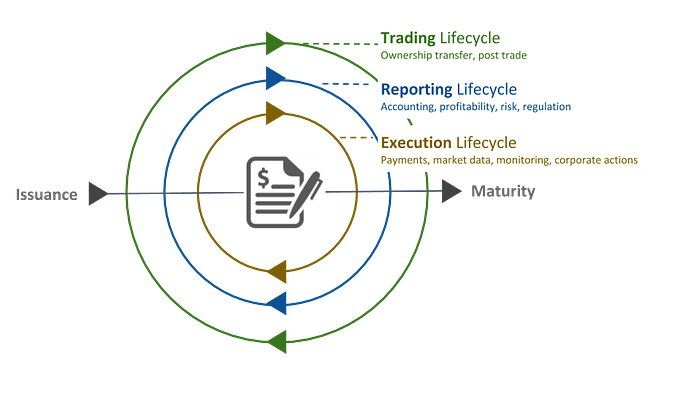

As mentioned above, currently the security token discussion focuses mainly on an asset’s issuance and trade-lifecycle. However, the life of these assets is much richer in terms of the various events an asset emits or is subjected to. Generally, we consider three subsequent phases in the life of a financial asset as follows:

- Issuance

- Lifetime

- Maturing/Expiring

These three phases are shown in the following figure together with three parallel lifecycles that summarize various cyclic activities the parties involved are engaged in during an asset’s lifetime.

1. Issuance

Whether a simple loan or mortgage within a retail bank or a security on capital markets the life of an asset starts with preparation of the issue. As an example, for off-the-shelf products in retail banks this means that the product serving as a template for issued assets is parameterized for the specific client with whom the bank intends to engage. Or, if issued on capital markets the terms of the asset, or the financial contract backing it, are drafted in the term sheet or prospectus, respectively, which is then reviewed by all parties involved and possibly edited again. In general, preparation of the issue also includes that investors (or borrowers for the retail bank example) go through a compliance process such as KYC or accreditation status verification. Once all these things are sorted out and parties agree to the terms the asset is issued. At this point in time, the financial obligations according to the term sheet become legally binding.

2. Lifetime

Once issued, the lifetime phase of the asset begins. Therein, the three lifecycles mark individual event streams that progress in parallel:

The execution lifecycle covers various events and activities around the execution of terms encoded in the asset — sometimes and in particular on capital markets these events are called corporate actions. Obviously, this involves all parties who participate directly in the asset, in particular the issuer and investor, but potentially also asset servicers such as custodians, brokers, or payment agents:

Issuer:

- Determine payment obligations under the terms of the asset (e.g. interest payments, repayments)

- Define and declare optional payments such as dividends

- Execution of payments

- Updating the terms and conditions as foreseen by the contract e.g. variable rate instruments

- Announce corporate actions in general

Servicers:

- Keep record of asset holders

- Distribute payments from issuer among investors

- Transfer payments to (fractional) beneficiaries

- Distribute corporate actions information

Investors:

- Determine own rights and obligations under the agreement

- Monitor the performance of issuer and whether payment obligations are made

- Receive payments from payment agents

- Reconciliation of security records with custodians

- Monitor and react to corporate actions announced by issuer

While this is not an exhaustive list of events and activities involved in managing the execution-lifecycle of a financial asset it gives a glimpse of the complexity around that part of its lifetime. In particular, the challenges around corporate actions range from broadcasting information from the corporation to all asset holders to executing payments. As an example, the Depository Trust & Clearing Corporation — one of the leading post-trade infrastructure provider for US and global financial markets — has described this challenge in a book on the lifecycle of US securities as follows:

“Making sure corporate action proceeds are collected and allocated in a timely and efficient way is a giant processing task for the depository because it must deal with thousands of agents around the world.”

While gradual improvements have led to more efficiency in certain processes, e.g. the move from T+3 to T+2 settlement, since 2010, processes and systems around the broadcasting of information on and execution of various types of corporate actions remains a challenge.

The reporting lifecycle covers all activities around analysis and reporting for the asset. Specifically in an institutional environment these activities currently consume a lot of time within the organization and, hence, are responsible for a large share of operational cost. Specific examples of such reporting activities are:

- Accounting

- Controlling and financial planning

- Risk management

- Regulatory reporting

To a certain extent, the complexity around reporting processes are related to specific regulatory requirements that vary across jurisdictions and change over time. Another reason is the presence of inconsistent data models within and across institutions as well as financial information providers. Partially, the root cause for this can be found in missing data standards across financial markets but also within institutions. As a result, institutions are faced with huge data normalization, consolidation, and reconciliation overhead. In fact, a joint analysis by Accenture and McLagan on the cost-savings potential for blockchain in banks found that:

“Finance-reporting costs could shrink by 70 percent as a result of the optimized data quality, transparency and internal controls provided with a shared, single source of verified data”

Based on the ideas of a consistent smart financial contract representation of all assets within an organization, outlined in this article, and a deep transaction document for regulatory purposes, presented here, the above cost-savings potential can be extrapolated to all accounting, analytics, and reporting activities in banks.

The trade lifecycle captures all activity around the possible selling and buying of assets, or fractions thereof, on exchanges or over-the-counter. Thereby, the trade-lifecycle is currently in itself very complex and involves a number of parties as outlined e.g. in Stephen McKeon’s Security Token Thesis. Security tokens, because building on blockchain technology as a shared infrastructure layer, overcome most of the friction in this part of an asset’s lifetime which is one reason for the increasingly widespread adoption of STOs as mentioned above.

3. Maturity/expiration

Finally, end of life is the last period in the life financial assets. In fact, for debt assets the time of end of life is defined as a term in the asset’s term sheet. Other types of assets such as equities do not have a fixed end of life but this is terminated only according to certain corporate actions such as reorganizations or mergers. In this case old shares are retired and new shares issued. In both cases market infrastructure plays also an important role here as investors have to be informed of the asset’s end of life. Furthermore, for debt assets the proceeds of principal repayment have to be distributed among investors and records for related assets updated. This may sound trivial but, again, in the current infrastructure with different parties involved as intermediaries between issuer and investor the flow of information and funds can be quite cumbersome in practice.

In this article we have outlined the various phases, events and activities of parties involved in the full lifecycle of financial assets beyond issuance and trading. Therefore, we have first reviewed the very nature of financial assets and found that they all are backed by financial contracts encoding future claims which investors ultimately are entitled to. As a result, apart from issuing and trading assets parties involved need to be able to understand, analyze, execute, monitor, and report on these contractual claims as well as other contractual events during the entire lifetime. For institutional players holding portfolios of thousands and more assets this means they will need the ability to integrate new digital financial assets into solutions that scale. Otherwise, the benefits of blockchain technology and security tokens will be outweighed by the additional cost to manage diverse portfolios from issuance to execution and reporting.

About atpar: We have seen firsthand how legacy financial architectures create barriers and hinder prosperity. We have created the ACTUS Protocol enabling issuance and management of the full lifecycle of all kinds of financial assets on blockchains. We help building solutions powered by the ACTUS Protocol. We see a future of frictionless, boarderless and inclusive financial ecosystems.

Acknowledgments: My thanks go to the entire atpar-team who are doing an excellent job building the ACTUS Protocol. Specific thanks go to Michael Svoboda, Johannes Pfeffer and Johannes for their valuable inputs to this article.