87. BBPS — Revisit

PAs such as BillDesk, TechProcess (now Worldline), Atom (now NTT) existed since the early 2000s. So you may be wondering who were there merchants? What people were buying?

Mostly, people were paying various types of utility bills.

The OGs of PA world (BillDesk and TechProcess) built an EBPP (Electronic Bill Presentment Payment) platform that onboarded billers (utility companies) and other side agents (physical counters, websites, bank internet banking portals etc.) who bring customers.

EBPP worked nicely but had its own problems related to interoperability and was dominated by BillDesk.

In 2016, NPCI launched BBPS (Bharat Bill Payment System) and in April-2021, NPCI created a subsidiary, NPCI Bharat BillPay Limited (NBBL), to promote BBPS in India and abroad.

In 2018, I wrote an article on EBPP and BBPS (Read this article) and now will revisit the BBPS

I. Master Circular

On 29th Feb (2024), RBI published the Master Directions on BBPS and here are the few takeaways.

- Entities and their roles

Participants of BBPS are pretty much the same as shown above. Apart from these entities there are Biller Aggregators — Entities that aggregate billers and enable them to connect to BOU.

There is new interesting entity that is introduced — Technology Service Providers (TSP)

TSPs are NBBL certified entities that enable or help Agent Institutes, COU and BOUs to integrate with BBPS.

What do TSPs do? They mostly unify APIs thus reducing dependency on a single player, make integration simple and add some analytics.

TSPs are not new and not even for BBPS space. Setu.co (acquired by Pine Labs) has been operating as TSP for banks for BBPS for quite some time.

2. Welcome — Payment Aggregators (PAs)

An entity needs to take a licence from RBI to operate as BBPOU either as BOU or COU or both.

Below is the snapshot of BBPS institutes (few months old)

Earlier, net worth requirement for non-bank BBPOU was Rs.100 crore. It was a huge amount of money and the licence was huge work. Not so surprisingly, many big payment companies (e.g. Cashfree or RazorPay) were not BOUs.

In May’2022, net worth requirement was reduced to Rs.25 crore (same as Payment Aggregator licence).

And now the new circular allows any authorised/licensed PA (Payment Aggregator) to become BOU or COU or both after informing RBI.

A PA licensed entity can do domestic PA (online), PA-Cross Border and participate in BBPS.

So a PA licence is equivalent to the One Ring from JRR Tolkien’s the Lord of The Rings… One licence to rule them all :)

3. BBPS Working Details:

Nothing much changed in the working of BBPS but let’s revisit the flows

A. Types of bill payments:

- Bill payment: The bill is fetched from the biller and presented to the user to make the payment. User has to make full payment and before the due date.

- Quick Pay: Bill fetch is not done. Users can make the payment (any amount) and before-after due date.

B. Types of transaction flows:

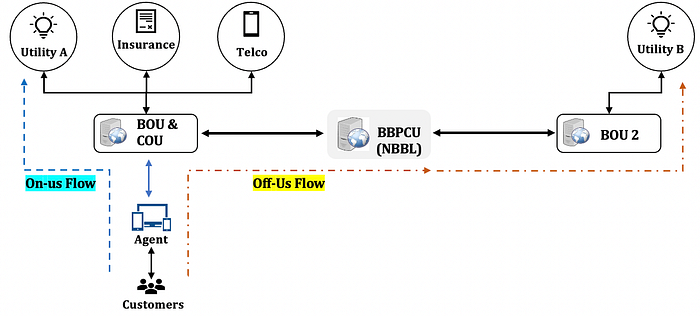

- On-Us transaction: Cases where the biller and agent belong to the same BBPOU. In this flow, the BBPOU confirms the payment status and moves the funds from agent to biller without involvement of BBPCU i.e. NPCI.

- Off-Us transaction: Cases where biller and agent are with different BBPOU. In this flow, BBPCU facilitates the bill payment and acts as swtich/clearing house to move money from the agent to the relevant BBPOU who in turn will settle funds with the biller.

C. Bill Payment Process:

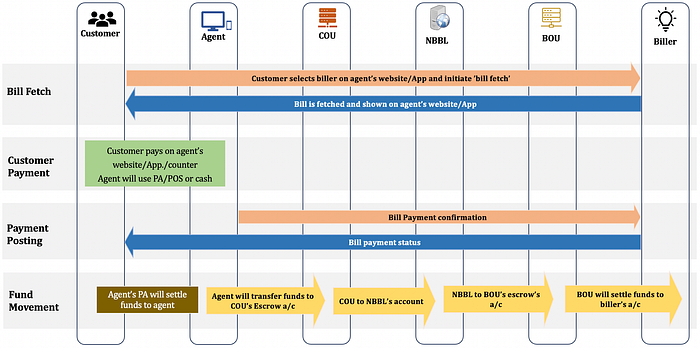

Let’s consider a Off-Us flow and biller works on ‘bill payment model’

Above diagram covers all the 4 phases

- Bill fetch — customer will gets to know the bill amount

- Customer payment — customer pays bill on agent’s site/app/counter. The agent can use PA or POS or Cash for customer payment and PA/POS providers will settle funds to the Agent. This phase is not part of BBPS.

- Payment posting — payment status is communicated to biller and biller will mark it as ‘paid’ and gives confirmation back

- Fund movement: Fund is moved from agent to biller through COU→ NBBL → BOU.

II. Unified Presentment Management System (UPMS)

By virtue of BBPS, I can pay bills via third party Apps.

Let’s assume if I had paid bill using Google Pay and then once PhonePe then every month, both these Apps will send me alert that a new bill is available for payment

This is one of the drawbacks of BBPS

- Each Agent (e.g. PhonePe and G Pay) fetch the bill and send notification to user

- An Agent (Google Pay) will not get to know if the user has paid the bill via another COU’s Agent (PhonePe)

So in the existing BBPS’ decentralised presentment model, creates burdens on billers’ system as every agent will call API to fetch bills) and inferior user experience as multiple agents will send bill presentment notification.

Remedy for this problem is UPMS

Where the UPMS provides the centralised procurement platform where UPMS fetches the bill (one-time) and then agents (of COU) can fetch from UPMS (means, agents doesn’t have to call API to biller’s system)

Once the bill is paid through an agent then it is marked as paid and other agents will know (via status check API) that the bill is paid and they can avoid sending notifications.

UPMS will also allow users to set-up the mandates of recurring payment solutions (e.g., UPI AutoPay).

III. BBPS for International:

Everyone pays bills — even the Indians who are living abroad pay bills in India. It could be for them or for their families back home.

Now the users based out of India can make bill payment via BBPS.

At present, this is live in three countries

- UAE: Lulu Exchange in partnership with Federal Bank

- Kuwait: Al-Mazaini Exchange

- Oman: Musandam Exchange in partnership with Canara Bank

Just to clarify, ‘exchanges’ are the entities that provide cross-border remittance service and they have both physical branches as well online portals. So the migrant population is quite familiar with ‘exchanges’ and logically it makes sense as an exchange offering bill payment service.

Working:

Bill-fetch and bill payment APIs will remain same as regular BBPS flow except the amount is shown in local currency

Exchange will maintain a RDA (Rupee Drawing Account) with the bank which is acting as COU.

Customer will make the payment in AED and basis the exchange’s instruction, the COU bank will move funds from RDA account to Biller (via NPCI and BOU)

Bill payment for NRIs is a good use case but the success of this model purely depends on ‘charges’. A migrant worker, will he use this if there is even a small fee. Think about it?

Any interoperable system creates a level playing field where participants get access to the platform (after licence or certification).

But 1–2 participants become very big. Example: PhonePe in UPI ecosystem. And to balance the UPI ecosystem, NPCI has to come up with a 30% limit on TPAPs (not implemented yet).

20+ years, first EBPP and then BBPS, still BillDesk is the dominant player in the bill payment space. Maybe the entry of PAs who are good at price-wars (and repent later strategy) and TSPs (who bring tech prowess) can make some waves and change the status quo.