Hot Inflation Data causes Massive Sentiment Shift

In this macro series, we explore the changing global sentiment for risk assets in light of recent CPI data, geopolitical tensions, taxes and more.

There was a massive change in sentiment around risk assets over the last few weeks. In 2024, Jan and Feb CPI reports were hotter than expected and had already started a repricing of rate cut expectations (went from 6 cuts in December to 3 at the beginning of April). A CPI YoY print of 3.5% (vs an expected 3.4%) for March really accelerated this repricing and forced a rethink around FED rate trajectory. In subsequent remarks, Fed chair Powell also reluctantly stated that they may need to hold rates at higher levels for longer till the inflation trajectory improved.

Coming into April, worsening liquidity due to seasonal effects (April is tax season and assets are sold to fulfill tax liabilities) had already set up a backdrop for weaker risk assets. Repricing of rate trajectories further hurt sentiment as US 10 yr bond yields marched back to 4.6%. On top of that, geopolitical tensions and war risk in the Middle East acted as tinder to accelerate the conflagration. Equities retreated from all time highs and credit, both investment grade and high yield sustained losses. The Dollar meanwhile strengthened and acted as an across the board damper for risk assets globally.

Monetary Policy Divergence

A month ago, the market expected a concerted global monetary easing with most central banks looking to cut rates. However the recent FED trajectory repricing has led to an increasing monetary policy divergence between the US and other economies leading to a stronger dollar. As expectations of tighter US monetary policy for longer get priced in vs looser policy in Japan,EU, UK and Switzerland, their currencies have all tumbled.

Gold

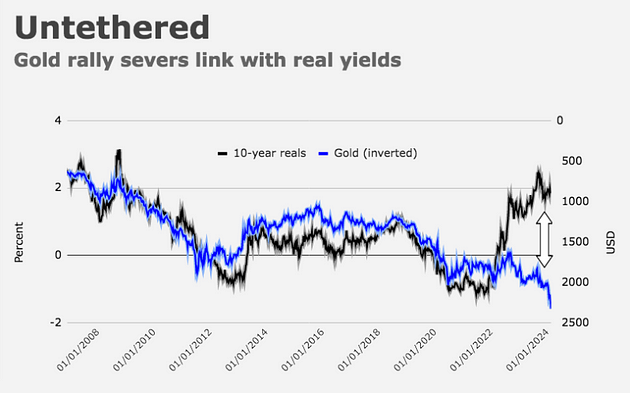

Gold has been on a scorching rally as a monetary inflation hedge (distinct from a main street inflation hedge) as expectations for central bank balance sheet increases (QE) over the long run continue. Gold moves inversely with real yields ( it doesn’t have a yield, thus becomes unattractive when other assets have high real yields), but this relationship has broken down recently. It appears that gold has been discounting a collapse in real rates, as investors hedge the risk of Fed cutting even when inflation doesn’t decelerate enough, and the subsequent possibility of yield curve control and QE to backstop US govt funding.

On the flows front, Gold ETFs have been losing assets, however demand for physical gold has been at an all time high. Central banks,especially PBOC have been heavy buyers while retail flows from China have also been exceptionally high as all other asset classes (real estate, equities) have been pummeled and investors flee to safety.

Near Term Macro Outlook

The market is delicately balanced and current market narrative and patterns resemble last summer as inflation surprises to the upside and FED rate cuts are priced out. The US economy has been humming along nicely but the pace of growth has slowed down. A slowing economy enables the Fed to be more accommodative and cut ,while hot inflation data forces it to stay tighter for longer. Inflation has been the stronger narrative for now and thus a very warm core PCE print on Thursday (3.7% vs 3.4% expected) dealt a further blow to rate cut expectations with only 1.5 cuts priced in for 2024 now.

For the rates complex, upcoming Treasury Auctions matter, with the possibility of a “backdoor equity put” from Janet Yellen when she announces quarterly treasury refunding next week. A surprise with a lower financing estimate (robust tax receipts have built up treasury reserves and reduced US govt borrowing requirements in the near term) will be positive for bond yields (as the market needs to absorb lower issuance) and boost risk sentiment. Equities have been blindsided by the rapid run up in bond yields and have come off the highs thus a positive surprise with rates will act as support amidst a mixed earning season for US megacap tech names.

Crypto

The rout in risk assets in April hit crypto as well. There seems to be a structural change underway in the market with disassociation between BTC and altcoins, as BTC becomes more aligned with tradfi after the ETFs. BTC remained range bound and briefly wicked below 60k as massive liquidations happened over middle east war fears amidst low liquidity.

Altcoins however got completely decimated and a significant amount of OI got wiped out in massive cascading liquidations. This leverage flush reset the market for consolidation before the next leg up, whenever it happens.

Bitcoin Halving and Runes Launch

On April 20th at block 840,000, the 4th BTC halving took place and reduced block rewards to 3.125 BTC. Concurrently, the Runes token standard was also launched and created a minting frenzy with users trying to get in early on the most promising tokens. This led to a bounty for miners as fees spiked and more than compensated for reduced block rewards. In fact, runes generated $135 mio fees in the 1st week alone! There has been a lot of attention on the BTC ecosystem as expectations of BTC DeFI summer heat up.

Read more from the author (and our macro researcher), Fractalmonk: https://medium.com/@fractalmonk999

Avantis is a an onchain leveraged trading and market-making platform. Trade cryptocurrency, forex and commodities with up to 100x leverage, or power trades on the platform as a liquidity provider. Avantis gives advanced risk management tools to traders and liquidity providers for the use and provision of trading leverage. Avantis is built on Coinbase’s Base blockchain, and is backed by industry leading investors such as Pantera, Founders Fund, Galaxy Digital and Coinbase Ventures.