You Are the Job Creator

The Pitch: Economic Update for May 11th, 2023

Friends,

I want to call your attention to a new study of the $15 minimum wage from researchers Justin Wiltshire, Carl McPherson, and Michael Reich. It’s one of the most important minimum-wage studies since the breakthrough 1994 Card and Kreuger study that proved raising the minimum wage doesn’t kill jobs, and it delivers some excellent news that has, in my opinion, been hugely underreported in the economic media.

The report looks at 47 counties where the minimum wage has been raised to (or above) $15 per hour between 2009 and March 2022. These counties range across the economic spectrum, from extremely wealthy to below the average American wealth.

Unsurprisingly, the study found that raising the minimum wage increases earnings within the county. This is to be expected: When workers earn more money per hour, their personal wealth grows. But Wiltshire explains on Twitter that when the study drills down on the less wealthy counties in the study, “we estimate *large* and significant positive employment effects.” In fact, he writes, “These large minimum wage increases led to gains in both earnings *and* employment!”

Put even more simply, this study found that raising the minimum wage creates jobs — especially in economically depressed parts of the country. It’s hard to overstate how important this finding is. Many economists and politicians have repeatedly suggested that a higher minimum wage isn’t appropriate for rural areas and parts of the country with lower wages and less wealth. In recent memory, Senator Joe Manchin killed a $15 national minimum wage in the COVID relief bill because he claimed the wage was too high for his home state of West Virginia and would kill jobs.

This study is significant because it debunks one of the last remaining fallacious trickle-down claims about the minimum wage being a “job-killer.” It proves that a high minimum wage isn’t just good for workers in rural areas and the poorest parts of the country — it’s good for everyone because it creates jobs and increases prosperity for everyone.

This isn’t a surprise to those of us who have been involved in the minimum-wage debate since the dawn of the Fight for $15. It’s obvious that when workers have more money, they spend it at local businesses, creating jobs with their increased consumer demand.

But 40 years of trickle-down dogma takes a long time to die. If you believe, as most politicians in the country did for decades, that a few wealthy people at the top create jobs with their excess wealth, you’re going to find any number of arguments to use against raising the minimum wage. One by one, as cities and states have prospered after raising the wage, those arguments have been roundly disproven. This study feels like the final blow to trickle-down minimum-wage orthodoxy. We now can confirm that raising the minimum wage creates jobs. Period.

Now, who’s going to break the news to Senator Manchin?

The Latest Economic News and Updates

Inflation Is Declining, but Feelings Are Running Wild

As you can see in the chart above, inflation is on a steep decline. Rachel Siegel writes for the Washington Post that “Prices rose 4.9 percent in April compared with the year before…and 0.4 percent compared with March. There’s been significant progress on inflation from last summer, when the consumer price index hit 9.1 percent on a year-over-year basis.”

If you just pay attention to the numbers and data in Siegel’s post, you’ll find a wide array of promising economic indicators. But her analysis tells a completely different — and much gloomier — story: “even as inflation has eased for 10 straight months, policymakers are still fearful that inflation could become a permanent threat to workers and families who are also facing tighter credit conditions, rising loan payments and uncertainty about a recession,” she writes.

We’ve seen this again and again in the last few years — sound economic data accompanied with commentary about “fears” and “uncertainty” that gives the good news a sour aftertaste. The Wall Street Journal, for instance, warned in a headline about the declining inflation rate that “We May Be Getting Used to Inflation, and That’s Bad News.” I don’t know about you, but in the real world, none of my friends are “getting used” to high prices.

Still, prices for every item in the economy don’t march in lockstep, so here are some of the notable inflationary numbers of the past week:

- Meat prices are coming down steeply, reports Axios, and so are megacorporation Tyson Foods’ profits. In the last quarter, “The company swung from a $829 million profit a year ago to a $97 million loss” as customers finally refused to pay ridiculously inflated prices for meat. It seems that greedflation does have a ceiling, and when corporations gouge their customers too much in the pursuit of record profits, they’re likely to feel a considerable amount of pain when customers strike back.

- “Home prices fell in more parts of the U.S. than they have in over a decade during the first quarter, when nearly a third of metro areas posted annual price declines,” reports the Wall Street Journal’s Nicole Friedman. In part, because the Fed continues to raise interest rates, making mortgages even more expensive, nearly a third of the nation’s metro areas posted steep declines in home prices — especially in the western half of the country.

- One category that doesn’t see declining prices, though, is child care. The Washington Center for Equitable Growthreports that child care prices are now rising faster than virtually every other price in the Consumer Price Index:

American Workers Are Still on the Job

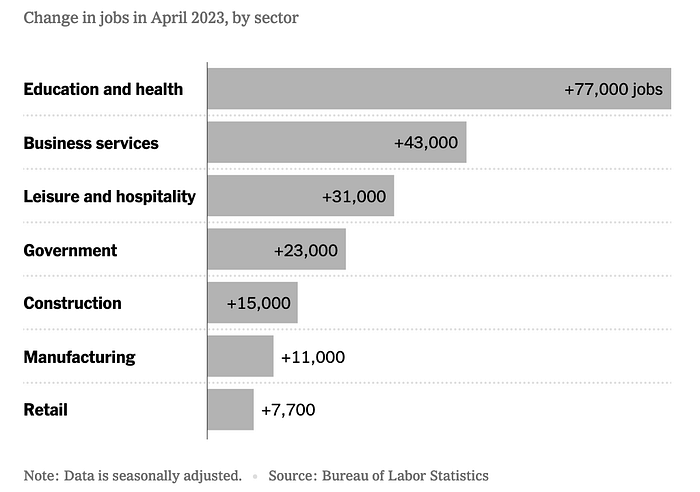

Another positive indicator for the American economy: Some 253,000 jobs were added to the economy in April, and the unemployment rate declined to 3.4% — its lowest in 54 years. The Black unemployment rate is also at an all-time low of 4.7%. All those high-profile layoffs in the tech and media sectors were a drop in the bucket compared to the massive hiring in leisure & hospitality, construction, and private education and health services fields.

Lauren Kaori Gurley writes for the Washington Post that those workers are also taking home bigger paychecks than they used to: “Wages, which have been growing more than the Federal Reserve would like to tamp down inflation, accelerated between March and April, with average hourly earnings increasing by 0.5 percent to $33.36.” (Of course, the Fed is wrong to connect rising wages with inflation, for reasons that we covered extensively in last week’s issue.)

To be clear: This is unabashedly good news. More people working for higher wages is great news for everyone in the economy. Those workers will create jobs and spread prosperity throughout their communities with their spending.

In the meantime, young Americans who are just entering the workforce are now in an excellent position to find employment, reports the Economic Policy Institute. The youth unemployment and underemployment rate for Americans aged 16–24 are better now than they have been in years, and EPI concludes that “Overall, this year’s young people are graduating into a strong labor market.”

But we should acknowledge that not every sector has come bounding back to life from the pandemic. One of the most noteworthy gaps between employment and job openings is in the child care sector, which the Washington Center for Equitable Growth notes is still lagging behind pre-pandemic numbers even as demand for child care is now skyrocketing. This chart explains why child care prices are rising now, and they’re also a sign that wages are too low to entice workers back into the field.

More Regulation, Please

While government has taken a stronger role in combating corporate consolidation over the last three years, there’s much more that the Biden Administration could do to combat inequality through stronger regulations. Here are a few of the stories that caught my attention this week:

- The New York Times’s Reed Abelson explains why giant corporations like health insurers are buying up the private practices of primary care doctors around the country: “The appeal is simple: Despite their lowly status, primary care doctors oversee vast numbers of patients, who bring business and profits to a hospital system, a health insurer or a pharmacy outfit eyeing expansion,” Abelson writes. In a society with a growing and prosperous elderly population, these corporations are preparing to cash in big on aging Americans. In return, patients will experience impersonal care and a nightmare of corporate bureaucracy intended to make it as hard as possible to get the swift (and affordable) care that you need.

- And another negative force is attracting attention in the healthcare industry. “Pharmacy benefit managers are companies that, behind the scenes, determine what patients have to pay for medications,” writes Vox’s Dylan Scott. “They manage insurance benefits for prescription drugs, dictating which drugs are covered by insurers and what costs patients will face when they fill their prescriptions.” After months, maybe years, of debate, the Senate is getting ready to rewrite the rules for pharmacy benefit managers, which will hopefully rein in prescription drug price increases and make it harder for insurance companies to deny patient access to affordable lifesaving drugs.

- On Monday, the Federal Reserve issued a biannual survey of the financial system, and it has found that the nation’s banks are under tremendous stress. With the Fed raising interest rates and three banks collapsing, the report calls for more regulations to shore up the banking sector and diminish the risky investments that destroyed mid-sized financial institutions like Silicon Valley Bank. Robert Kuttner at the American Prospect believes that these reports signal the dawn of a new round of banking regulations, and he also argues that the banking crisis is likely to inspire the Federal Reserve to lay off its relentless campaign of interest-rate hikes.

- The Consumer Financial Protection Bureau is cracking down on a predatory lender that disguised itself as an energy-efficiency program. “The Property Assessed Clean Energy (PACE) program was meant to make it easier for homeowners to install clean-energy technology, such as solar panels,” the Prospect notes, “But many of the projects financed through PACE, which is administered through private companies, have forced homeowners to default on their property taxes, or even left them facing foreclosure.”

- And the Economic Policy Institute has identified one place where government regulations can significantly help workers unionize: It often takes years for newly formed unions to get anti-union companies to agree to a first contract with their workers. Adversarial employers are dragging their feet on the writing of contracts in order to discourage workers and stealthily combat unions. “A much more effective way to reach a fair contract would be to require labor and management to begin contract negotiations shortly after union recognition, use professional mediation in the event of slow progress or an impasse, and submit to binding arbitration if mediation fails to produce a first contract,” EPI notes. This is clearly a part of the labor process that has gone underserved by regulations for too long, allowing employers to exploit the system to their own benefit.

Graph of the Week

The Congressional Budget Office put out a fascinating report this week spotlighting trends in corporate profits and taxation. The whole report can be boiled down this chart, which shows that corporate profits have consistently climbed over the last 40 years, while corporate tax payments have remained pitifully low:

When elected officials, like the House Republicans currently trying to tank the economy in the debt ceiling crisis, argue that government simply doesn’t have the money to spend on investments in working Americans, they’re clearly ignoring the lessons of charts like this. Corporations are making more money than ever, but they’ve kept their taxes so low that government is now losing out on billions of dollars in revenue every year. Note, too, that this chart ends at 2017, so it doesn’t even include those jaw-dropping record corporate profits that we saw over the last year.

Real-Time Economic Analysis

Civic Ventures provides regular commentary on our content channels, including analysis of the trickle-down policies that have dramatically expanded inequality over the last 40 years, and explanations of policies that will build a stronger and more inclusive economy. Every week I provide a roundup of some of our work here, but you can also subscribe to our podcast, Pitchfork Economics; sign up for the email list of our political action allies at Civic Action; subscribe to our Medium publication, Civic Skunk Works; and follow us on Twitter and Facebook.

- This week’s episode of Pitchfork Economics reprises a conversation with McKinsey and Company’s JP Julien about the data that proves inclusion is essential to economic growth.

Closing Thoughts

In the introduction to this newsletter, I wrote about a minimum-wage study that finally debunked one of the longest-lasting pieces of trickle-down economic dogma. Now, I want to highlight another paper that helps explain how that dogma became so widespread, and remained unquestioned for so long. For Slate, Pete McKenzie spotlights a new study of the economics profession that reveals exactly how homogeneous the field has become.

“Hoover and Svorenčík’s paper examines the leadership of the American Economic Association, the profession’s powerful governing body,” McKenzie writes. “According to their research, since 1985, almost 70 percent of the leadership of the AEA have been doctoral graduates of Harvard, the Massachusetts Institute of Technology, the University of Chicago, or Stanford University — a staggering overrepresentation, given that around 150 American universities grant doctorates in economics.”

It’s not just a problem with the American Economic Association: The paper examines the history of economic prizewinners and the pedigree of economists who work in high-profile government jobs and finds that the vast majority of those economists come from just six schools. And other universities are more likely to hire professors who got their degrees from one of those six schools.

So what does this mean? University of Washington Professor Jake Vigdor tweeted that “This pattern of exclusivity reflects a deep-seated worldview…that only the work of a handful of economists truly matters.” That’s a problem for everyone.

Study after study has found that white men dominate the field of economics, and this new report could explain how the field has become so homogeneous. Human nature dictates that when powerful people become too insulated, they begin to disengage from reality — and when those powerful people select the next generation of powerful people, you can begin to see how a worldview as unhinged as trickle-down economics can survive for four decades without any serious investigation.

Diversity of background and diversity of perspective are perhaps the two most important contributors to the longevity and success of an institution. Economics right now suffers from a lack of both. Our leaders and our educational institutions need to start looking away from the six dominating economics schools and toward the other 144 economics schools in this country to find solutions for our modern economic problems. It’s long past time to bring some new voices to the choir.

Be kind. Be brave. Take good care of yourself and your loved ones.

Zach