How EM Investors View Russian Equities

Key Points

- Global EM investors are increasingly looking beyond standard MSCI index constituents in Russia in search of value.

- Average investor allocation to Russia is 3.76% marginally higher than the MSCI benchmark allocation (3.42%), however with a higher deviation from the average than other emerging markets.

- Sector focus in Russia is shifting away from traditional areas like oil & gas and mining towards new areas such as retail and technology. The opportunity for stocks outside traditional sectors to capture institutional investment is perhaps greater now than at any point in the last 5 years.

- A well-structured methodology for proactive targeting of investors can help IR teams to take advantage of new opportunities.

Emerging Market Fund Analysis & Methodology

This blog is written in conjunction with Copley Fund Research, an independent research firm which analyses the holdings of a specific sub-set of institutional equity investors.

In this case we are focusing on a cross-section of 120 actively managed global mutual funds, which invest a combined total of over $250bn in emerging market equities.

These funds use an index (usually the MSCI Emerging Market Index) as their performance benchmark but have complete discretion over portfolio allocations amongst global emerging market companies. As such they provide a good indication of buy-side sentiment towards countries, sectors and individual stocks in emerging markets.

Here we highlight some of the key trends in their fund allocations, analyse the overall pattern of investment in Russian companies and look at some of the top EM Funds that might be of interest to Russian IR teams.

Russia: Today’s Investment Landscape

According to public data, at the start of January 2016 Russian equities made up 3.42% of the MSCI Emerging Markets index, representing a combined total of more than $1.7 trillion in passive and active investments by over 1,100 institutional investors globally. Despite recent outflows and transaction sanctions imposed by Europe and the United States, investors from these geographies continue to hold the lion’s share (>75%) of institutional investment in the Russian equity capital market.

Geographical Distribution of Institutional Equity Investors into Russian Equity Market (2015)

Russian Equity Investment Trends

Following a steady increase in equity investment in Russia between 2011 and 2013, the market was badly hit by the global commodity price depression and the uncertainty caused by the Ukraine conflict and associated trade sanctions. Russia is now the 8th most popular emerging market by average portfolio weight, having been overtaken by South Africa and Mexico during the last few years.

The macro economic factors affecting Russian investment have far outweighed the micro factors, with some institutions forced to close Russia funds entirely to satisfy risk managers and internal obligations.

However, the downward trend may now finally be reversing, as many funds increased their Russian equity allocations during the second half of 2015, positioning themselves as overweight versus the MSCI EM index. Should this trend continue, 2016 may well reward the more optimistic IR teams who anticipate growing interest in their company story and plan accordingly.

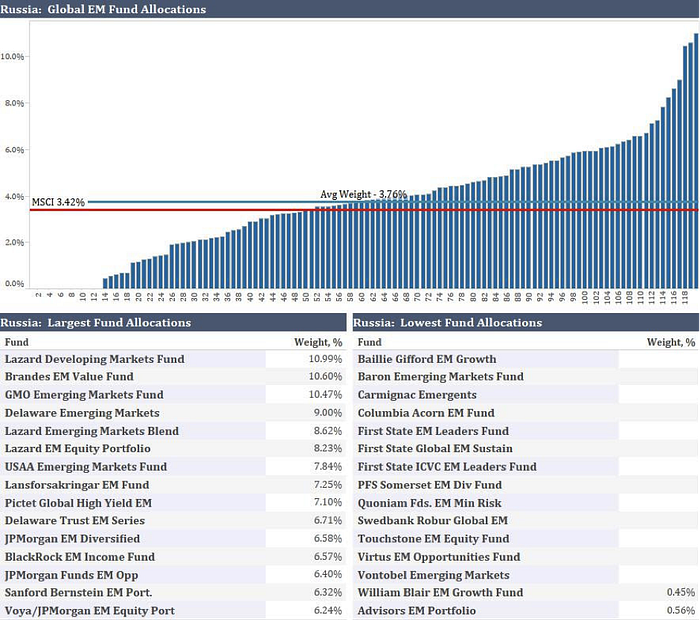

Distribution of Investment in Russia

The current distribution of Russia holdings can be seen in the chart below, with wide ranging levels of allocation amongst the 120 funds. The average allocation of 3.76% is marginally higher than the MSCI EM index benchmark allocation of 3.42% — and still higher than the percentage allocated to either Turkey or Poland — indicating a moderately bullish stance on Russia at present.

Taking Advantage of Investor Opportunities

Following the 2008 credit crisis, investment in Russian equities reached its peak in December 2013. As stated above, a large number of investors subsequently either reduced or sold off their positions as economic conditions worsened. Should this situation turn around, these investors could prove particularly interesting for companies, given their history of interest in the Russian market. It’s certainly worth companies keeping track of investment patterns to understand the likely impact of a change in market conditions and take advantage of potential opportunities.

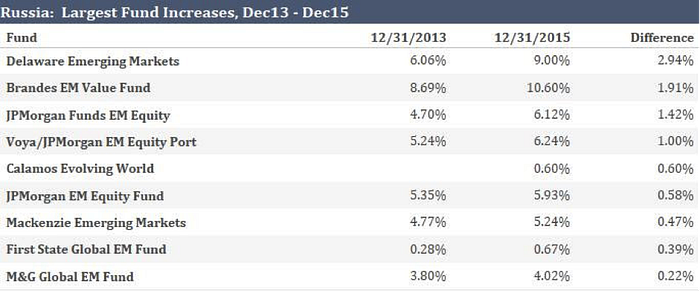

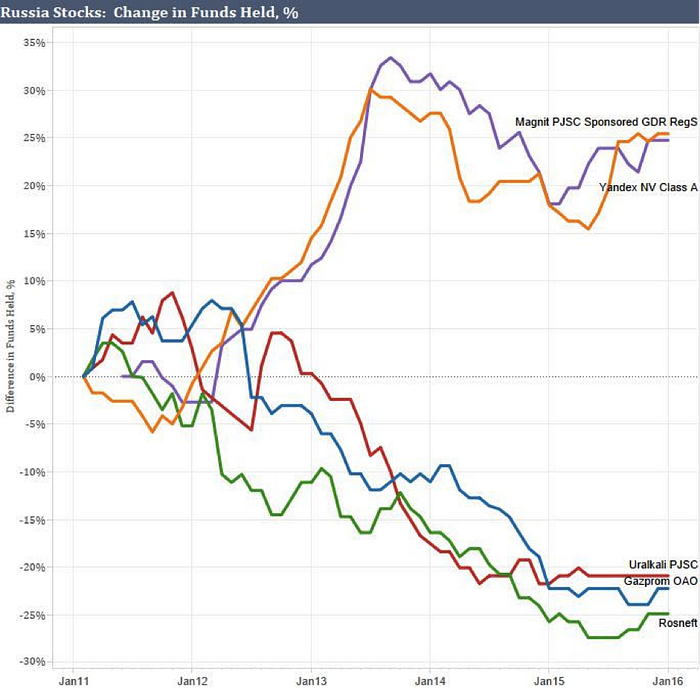

2015 Activity

The chart below shows the funds who have increased exposure to Russia the most over the course of 2015. Schroder’s EM Opportunity Fund tops the list, followed by Lazard’s Developing Market Fund. All of the funds listed below have a shown a willingness to invest in Russia when others have taken a more cautious approach.

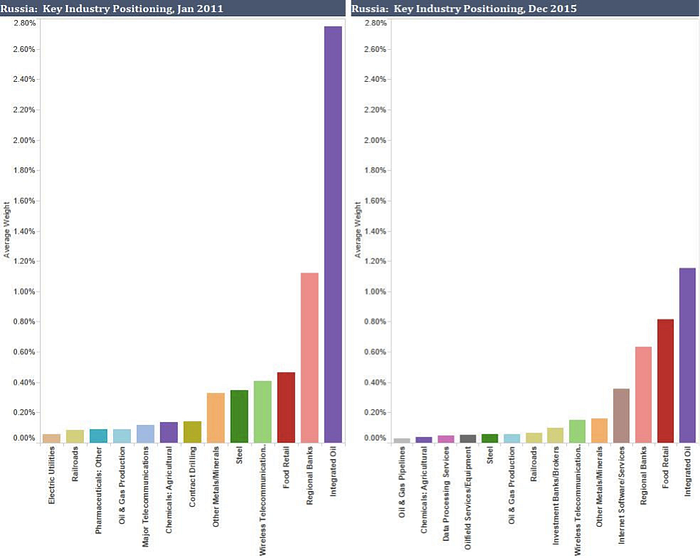

Sector focus

During the last few years investor appetite has switched more and more towards the technology and consumer sectors and away from oil and gas, in line with other emerging markets. Russian oil & gas stocks made up nearly 3% of EM portfolios back in January 2011 but now account for under 1.2%; food retail stocks have nearly doubled from 0.47% to 0.82% over the same period.

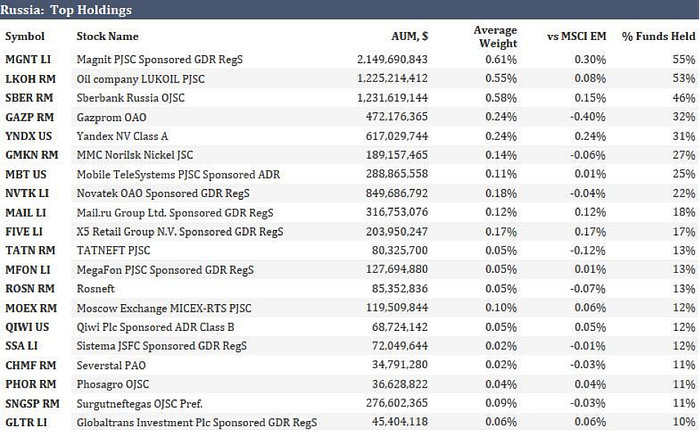

From a stock perspective Magnit, Lukoil and Sberbank are the most widely held in Russia; each is owned by around 50% of funds and together they account for around 46% of total holdings in Russia.

New Emerging Market Opportunities

EM active investors are more than willing to invest outside the benchmark index where the opportunities arise. Stocks such as Yandex, X5 Retail and Mail.ru are not included in the MSCI benchmark but have attracted over $1bn in investment from the active EM funds in our analysis.

This shows two things: firstly that just because a company’s stock is included in the MSCI EM index doesn’t automatically mean that active investors will invest, and secondly that the MSCI EM index isn’t a barrier to attracting investment from international EM funds. This should encourage companies outside the MSCI Emerging Markets index to engage with global EM active investors as they have a clear mandate to look beyond benchmarks in order to generate excess returns.

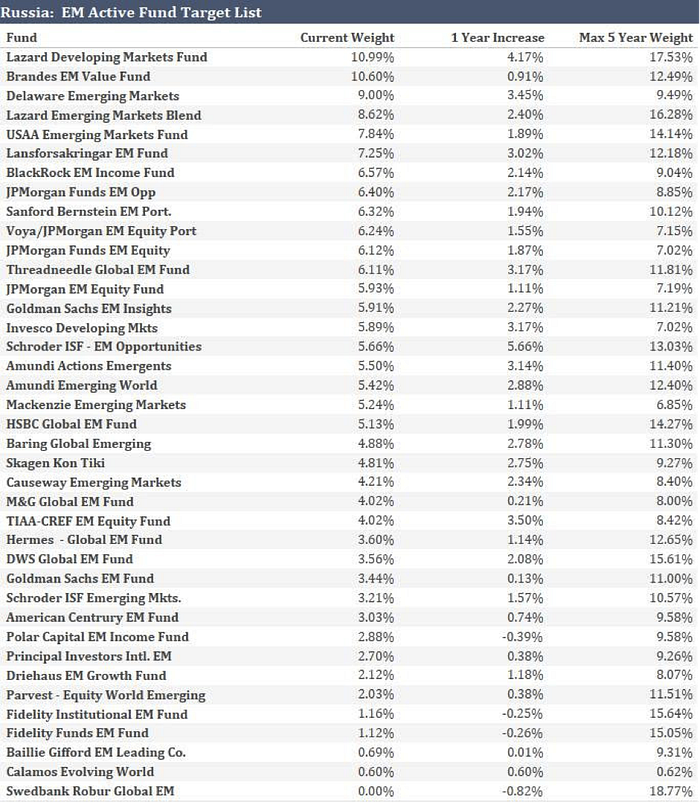

Focus List

Based on the analysis above we recommend the 39 global emerging market active funds listed below should be on the radar of Russian IR teams. These funds are selected on the grounds of either their current allocation in Russian equities, increased Russia allocations over the last 12 months, and/or a history of high allocations in Russia over the last 5 years. As such they will have a greater propensity to invest in high quality companies throughout the region.

A Framework for Investor Targeting

Investment profile of my company

The starting point of any investor targeting exercise is to build a solid understanding of how your company’s story can fit into criteria that global investors look for when screening for companies: liquidity, key fundamental metrics and non-financial highlights.

Things to consider:

- Does my company’s liquidity, or average daily trading volume (ordinary shares and depositary receipts combined) meet institutional investor requirements? Minimum threshold for large institutional investors is on average $1million+ per day. Smaller funds or those focused on the mid-/small-cap segment of the market often have more flexibility, however also tend to have fewer resources and less support (corporate access, investment research) from brokers.

- Compared to the regional and broader EM peer group, which set of fundamentals particularly stands out in my equity story?

- How are we positioning our collateral to address the needs of investors with particular strategies (e.g. Income/Yield, Growth, Value etc)? Do we have a good understanding of the triggers of the investment decision on those funds?

- What are the key non-financial metrics that matter in my story? What macro- or mega-industry trends is my company’s equity story continually benefiting from?

Opportunity Analysis

Many companies take a technical, if not scientific, approach to identifying investor opportunity. A starting point is to conduct a comprehensive analysis of your own shareholder base, factoring in significant movements over the past four quarters.

Next, an institutional investor study draws up a target investor groups based on a number of criteria:

- Investors who are already present in my shareholder register

- Investors who are invested in my peer group but not in my company

- Investors who have held my company’s shares previously but do not currently hold them

- Investors who have been increasing allocations to my region and/or my sector

- New EM funds launched globally over the last 12 months

- New ideas of investors from brokers and other consultants

Things to consider:

- Do I have a clear understanding which investors with active mandates hold my regional and international peer group? How often am I monitoring changes and activity in this list? Are the changes in line with what we are seeing in our shareholder base? If not, what are the drivers of the outliers?

- Am I monitoring developments in the passive and ETF industry and do I understand which benchmarks my company is part of? What are my company’s allocations to each of those indices?

- How often am I monitoring broader fund flows into my region and comparing this to what we are seeing in my company’s shareholder base?

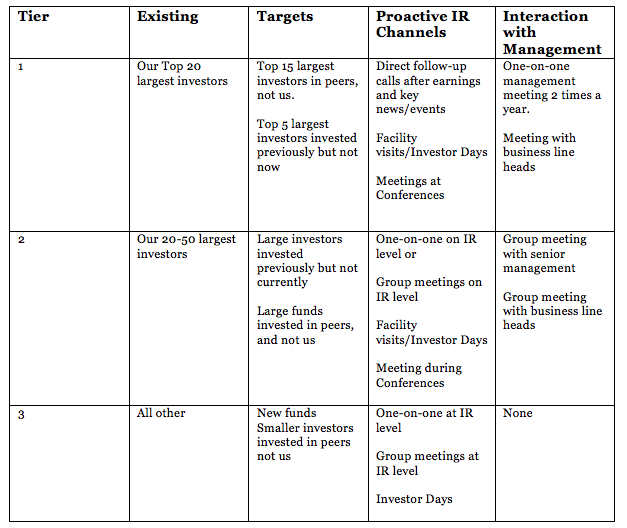

Segmentation

Following this, companies often group investors into tiers, which then dictate the outreach strategy for the year. For illustration purposes the following example may be helpful:

All investor tiers have access to ‘passive channels’ which include IR website/web casts, annual report, IR mailings / press releases, IR events (R&D day, etc.), quarterly conference calls, event-driven/product conf. calls, phone & email contact with IR

The study can then be applied to three key geographies: Europe, North America and Asia.

Summary

In summary, Russian allocations in EM portfolios are increasing but from a historically low base. In order to capture a share of these allocations, it might benefit IR teams to keep track of those funds with a history of investment in Russia. The opportunity for stocks outside the traditional focus of oil & gas to capture institutional investment is perhaps greater now than at any point in the last 5 years. Our targeting framework can be applied by listed companies to proactively target new opportunities.

We hope it is useful and are happy to provide additional information and answer any questions.

Steven Holden

Founder

Copley Fund Research

steven.holden@copleyfundresearch.com

www.copleyfundresearch.com

+64 9 445 4350

Michael Chojnacki

Chief Executive Officer

Closir Ltd

michael.chojnacki@closir.com

www.closir.com

+44 792 0729 329