Everything You Need To Know About The COTI Treasury

TOC

- TLDR

- Introduction

- Deposits

- Minimal engagement period

- APY

- Multiplier

- Rewards

- Health Factor

- Extend lock period

- Deposit Liquidation

- Withdrawal

- Fees

- Scenarios

- Summary

TLDR

- COTI’s Treasury is a pool of $COTI where users can deposit $COTI and be rewarded for their participation.

- When creating a new deposit you will be able to choose your COTI deposit amount, your multiplier (1x-8x) and your lock period (unlocked-360d). Risk factors range from minimal risk (unlocked, multiplier x1) to maximum risk (120 days, multiplier x8).

- An individual deposit APY is calculated based on an individual deposit’s risk factor

- Rewards are always unlocked so that users can claim them at any time.

- You can continue to earn additional rewards based on an APY that equals an unlocked deposit with a x1 multiplier (compound interest).

- New deposits or top-up will be subjected to a minimal engagement period of 5 minutes during which you will not be able to withdraw your deposit balance.

- If you withdraw the entire deposit balance, your accumulated rewards will be automatically withdrawn and your deposit will be closed.

- Withdrawing a deposit when it is within an active lock period will be subjected to a differential early withdrawal fee calculated based on the remaining lock time (2% max).

- The Treasury charges a 0.05% fee for deposits, and 0.25% fee for withdrawals. There is also a transaction fee that is divided into two parts: a network fee of 0.1% and a node fee of 0.1% equaling 0.2%.

- There are several parameters used by the system in order to calculate the deposit health factor; Deposit Multiplier (MUL), Deposit Original Value (DOV) and Deposit Current Value (DCV). If the deposit health factor falls to 1.0 or below, the deposit will be at liquidation risk.

- As of August 15th, 2023, the grace period will no longer be available.

- The Liquidated deposits’ entire balance will be transferred to the treasury and redistributed in a form of treasury rewards between all active deposits. If such an event occurs, accumulated rewards will remain in the platform and will be available to be claimed by the user at any time.

Introduction

Our much anticipated Treasury launch will go live on February 1st, 2022! This means a great deal to the COTI community, whose members will finally be able to deposit even more $COTI as well as choose the way they want to participate and be rewarded. In other words, you will now decide exactly how much and for how long you want to deposit.

Before the big day, we’d like to take you through everything you need to know about the Treasury and all the options it holds for you so that you are fully prepared. Please read each section carefully as they reveal a lot of new and important information about the Treasury. As a reminder, COTI’s Treasury is a pool of $COTI where users can deposit $COTI and be rewarded for their participation.

Deposits

You will be able to deposit your $COTI into the Treasury and top-up your active deposits with additional $COTI any time you wish. Deposits will earn an APY in the form of Treasury rewards ($COTI) based on the deposit multiplier and the lock period. When creating a new deposit, you will be able to adjust your deposit risk factor based on your own risk appetite by adjusting the deposit multiplier (e.g. x1, x2, x4, x8) and the lock period (e.g. Unlocked, 30, 60, 90, 120, 180, 270, 360 days). Risk factors range from minimal risk (unlocked, multiplier x1) to maximum risk (120 days, multiplier x8). Deposits with locking period longer than 120 days will not be able to apply multiplier. After a deposit has been made, the only actions that can be taken are depositing additional funds and/or withdrawing deposits and rewards. After the set locked period has elapsed, you will be able to set a new lock period.

Please note that the chosen multiplier will be applied to your deposit, regardless of whether the locking period has ended or not.

Minimal engagement period

New deposits or top-up (adding funds) to active deposits will be subjected to a minimal engagement period of 5 minutes during which you will not be able to withdraw your deposit balance. Making a top-up during the minimal engagement period will reset the timer (the minimal engagement time period is designed to eliminate system abuse).

APY

An APY is the annualized rate of return from an investment. An individual deposit APY is calculated based on an individual deposit’s risk factor which is a function of the deposit size, the multiplier, and the lock period (the APY calculation is performed in 60 second cycles). By increasing the multiplier of an individual deposit, its APY will increase accordingly and so will the risk of liquidation of that deposit due to COTI’s price fluctuation. In addition, the Treasury APY will be affected by inbound and outbound liquidity flow. Please note that the APY is an estimated APY as it’s being recalculated every 60 seconds and may fluctuate (increase\decrease) during deposits life cycle.

Multiplier

When you open a deposit, the x1 multiplier is selected by default (no liquidation risk). If you wish to increase your deposit risk profile, you may set the multiplier to a value higher than x1. Setting a higher multiplier will multiply the deposited amount within the treasury, which will result in a higher deposit APY. Increasing the multiplier value above x1 also introduces a deposit liquidation risk as the multiplier has a direct impact on the deposit health factor, which is calculated based on COTI’s price fluctuations (the higher the multiplier the higher the impact on the deposit health factor, e.g. Depositing 1,000 COTI with a 2x multiplier would be like depositing 2,000 into the Treasury).

Rewards

The amount of the rewards received is calculated based on the current deposit APY, which is recalculated every 60 seconds. Rewards are always unlocked so that users can claim them at any time. A huge advantage that the COTI Treasury has is the accumulated rewards. You continue to earn additional rewards based on an APY that equals an unlocked deposit with a x1 multiplier (compound interest) for as long as the deposit balance is greater than 0.

Health Factor

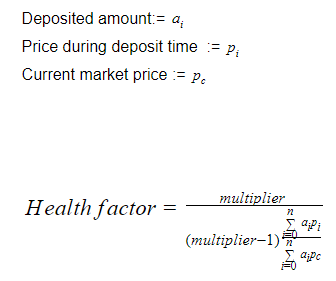

The Health Factor calculation is used to determine the health of the deposit; if the health factor reaches 1.0 the deposit will be at liquidation risk that may lead to liquidation of the entire deposit amount. Health factors may increase and decrease based on COTI price fluctuations. When the COTI price increases that health factor will increase, if the price decreases, the deposit’s health factor will decrease. The initial deposit health factor is determined based on deposit multiplier; if the deposit multiplier equals x1 then the health factor is non-applicable as price decrease will not put the deposit at liquidation risk. Deposits with a multiplier of x2 start with health factor 2.0, deposits with multiplier x4 start with a health factor of 1.33, and deposits with multiplier x8 start with a health factor of 1.14. Health factor impact ratio is calculated on deposit multiplier for example; a 10% COTI price will have a lower health factor decrease on deposit with a multiplier x4 then it would on a deposit with a multiplier x2. Health factor ratio is calculated based on the following calculation health factor ratio = multiplier/(multiplier -1). In order to calculate the health factor of a deposit the platform uses the following formula:

The platform will provide visual cues utilizing color coding the reflecting deposit health status; deposit with a health factor > 1.3 is considered a health deposit (Green), deposit with a health factor =< 1.3 triggers a liquidation warning (Yellow), deposit with health factor =< 1.0 will trigger deposit liquidation risk (Red).

Extend lock period

You may extend the current lock period by activating the “extend lock period” feature. By doing so, you will extend the lock period by an additional cycle once the first cycle has elapsed. For example, if you have locked a deposit for 30 days during which you have enabled the extended lock period, when the first 30 days have elapsed the system will automatically engage an additional 30 day lock period. After the second period has elapsed, your deposit will be unlocked. You may disengage the extended lock period at any time before it has taken effect.

Deposit Liquidation

In the event that the deposit was liquidated by the platform as a result of a deposit health factor of 1.0 (or lower) ,the Liquidated deposits’ entire balance will be transferred to the treasury and redistributed in a form of treasury rewards between all active deposits. If such an event occurs, accumulated rewards will remain in the platform and will be available to be claimed by the user at any time. Please note that remaining rewards will stop earning additional rewards as the deposit balance has been liquidated.

*Please note that it’s your responsibility as a user to actively maintain the deposits that are at risk of liquidation.

Withdrawal

You can withdraw all or part of your deposit or reward balance at any time. The withdrawal fee is 0.25%. If you withdraw the entire deposit balance, your accumulated rewards will be automatically withdrawn and your deposit will be closed. Please note that withdrawing a deposit when it is within an active lock period will be subjected to a differential early withdrawal fee calculated based on the remaining lock time (2% max). This fee will be reduced based on the elapsed time since the beginning of the lock period. All rewards accumulated during the active lock period will be liquidated and distributed as rewards in the Treasury. If you claim all your rewards and then decide to make a withdrawal while the deposit lock period is active, the platform will deduct the amount of the claimed rewards during the active lock period from the withdrawn deposit along with fees and an early withdrawal fine.

Fees

Below is a breakdown of the Treasury’s fee structure:

Deposit fee:

We have decreased the deposit fee from 0.25% per deposit to 0.05%. This will grow adoption.

Withdrawal fee:

Dynamic fees for withdrawals were replaced with a single flat fee of 0.25% that is significantly decreased.

Top ups and how they affect the withdrawal fees:

For every top up or new deposit, the counter will start counting from the beginning. The top up will reset the counter only for the new transaction and will be calculated from the same date that the top up was added. Thus, the existing transaction will not be affected.

Multiplier fee:

Multiplier fees are applied on multiplied deposits only (they do not apply for X1 deposits). The amounts are fixed per day, and are as follows:

Deposits with X2 multiplier: 0.0025% / Day

Deposits with X3 multiplier: 0.0033% / Day

Deposits with X4 multiplier: 0.0035% / Day

Deposits with X8 multiplier: 0.0045% / Day

The multiplier fee applies only to the deposit, not to the rewards. The multiplier fee will be collected and paid at the time of withdrawal.

Early withdrawal fee:

The early withdrawal fees are applied on deposits with a locked period only. The early withdrawal fee will remain the same (0%-2%) for users that withdraw their funds before the lock up period ends, as illustrated in the graph below:

Liquidation Risk Fee:

The liquidation risk fee applies only to those who added a multiplier factor to their deposits.

Liquidation risk fees range from 1%-5%, and the amount charged depends on the deposits’ health factor at the time of withdrawal.

X2 multiplier with health factor of 1.3 or below, will result in 1%-3% fees charged.

X3 multiplier with health factor of 1.15 or below, will result in 2%-3% fees charged.

X4 multiplier with health factor of 1.1 or below, will result in 2%-4% fees charged.

X8 multiplier with health factor of 1.04 or below, will result in 3%-5% fees charged.

The liquidation risk fee will be paid at the time of withdrawal.

You can find more information about the fee structure here: https://cotinetwork.medium.com/cotis-treasury-fee-structure-update-124bd3038a74

Scenarios

Below you can see a few different scenarios of users interacting with the Treasury:

*Please note that the numerical data presented in this article, such as the APY figures, are for explanatory purposes only and are not the actual figures. The exact numbers will not be available until after the launch.

- David is known for not being a risk taker and he will be happy earning a minimal APY on his deposit without exposing it to a potential liquidation risk. David deposited 100,000 $COTI, kept the multiplier at x1 and locked his deposit for 120 days in order to maximize his APY. When David created a new deposit with above mentioned parameters he noticed that the platform calculated and estimated 20% APY on his deposit. David returns to Treasury after 110 days and notices that his deposit accumulated 5,000 $COTI in rewards. David is happy with his deposit’s return and decides to engage the “extend lock period” feature in order to automatically lock his deposit for an additional 120 days when the active lock period elapses. David returns to the treasury after 130 days and notices that his accumulated rewards grew to 10,123 $COTI. David decides to do a partial rewards withdrawal for the amount of 5,000 $COTI.

- Alex is a known high roller and risk taker. He wants to deposit his 1,000 $COTI and aim for the max APY possible. Alex sets up a deposit with an x4 multiplier and locks his deposit for 120 days; the platform calculates an estimated 83% APY. Alex’s deposit health factor is 1.33 once the deposit is submitted. Alex returns after six months eager to claim his accumulated rewards. Alex locates his deposit and notices it’s colored red with a liquidated status, his deposit balance states 0 and his reward balance states 138 COTI. Don’t be like Alex, monitor your deposit.

- Nichole is willing to take some risks, so she decides to multiply her deposit by setting a multiplier of x2. Nichole deposited 50,000 $COTI and locked it for 90 days. When Nichole created a new deposit with above mentioned parameters she noticed that the platform calculated and estimated 49% APY on her deposit. Nichole keeps monitoring her deposit health on a daily basis and keeps a close eye on COTI price fluctuations as she is aware her deposit health factor can decrease and her deposit may be liquidated. After 90 days Nichole’s deposit is unlocked and she sees that her deposit accumulated 6,125 COTI in rewards. Nichole decides that she had a good run and wants to close her deposit by withdrawing her deposit and rewards balance. She withdraws her 50,000 $COTI deposit minus fees and her 6,125 $COTI rewards minus fees. Nichole walks away happy with the outcome of her Treasury experience.

Summary

This is the first version of the Treasury. In later versions you will see more features, calculators and automatic processes that will make your experience even more enjoyable. We are excited for the launch, which will mark the beginning of a brand new era for COTI and we are happy to have you, our users, by our side on this ever so thrilling journey!

In the coming days, we will also share a detailed step-by-step guide and videos describing all how to use the Treasury. Stay tuned!

Stay COTI!

For all of our updates and to join the conversation, be sure to check out our channels:

Website: https://coti.io

Twitter: https://twitter.com/COTInetwork

Telegram: https://t.me/COTInetwork

Github: https://github.com/coti-io

Discord: https://discord.gg/wfAQfbc3Df

Technical whitepaper: https://coti.io/files/COTI-technical-whitepaper.pdf