DAR Crypto Weekly — 3/13/20

When the Levee Breaks

Market Overview

It was a brutal week for digital assets as prices were down significantly for the week — the total industry market cap down 46.5% to $135.5B. Large-cap relative winners on the week were XRP (XRP -34.5%), Bitcoin (BTC -37.2%), and Litecoin (LTC -43.1%). Laggards in the large-cap category were Bitcoin SV (BSV -51.5%), Bitcoin Cash (BCH -49.7%), and Binance Coin (BNB -49.5%). Other noteworthy relative outperformers across the industry were UNUS SED LEO (LEO -1.4%), KuCoin Shares (KCS -5.4%), and Factom (FCT -27.1%). Other notable laggards on the week included Beam (BEAM -60.1%), Harmony (ONE -60.0%), and Ocean Protocol (OCEAN -59.0%).

DAR Research and Events

It was a crazy week in traditional markets and an even crazier one in crypto. We have some interesting research we were going to publish, but frankly it’s not timely and it would probably get lost in the madness. We’ll hold it off until things quiet down, but we swear it’s super interesting. Tune in shortly.

Against the backdrop of this week’s craziness, we were interviewed for a story at Coindesk regarding this week’s market volatility. The article can be found here.

An interview with DAR’s Chairman Doug Schwenk is live on the Tabb Forum. This broad-ranging interview covers risks for institutional traders, the current state of crypto regulation globally, and whether firms can trust crypto market data. The interview can be accessed here (login required).

A Historical Week, but the Bad Kind of History

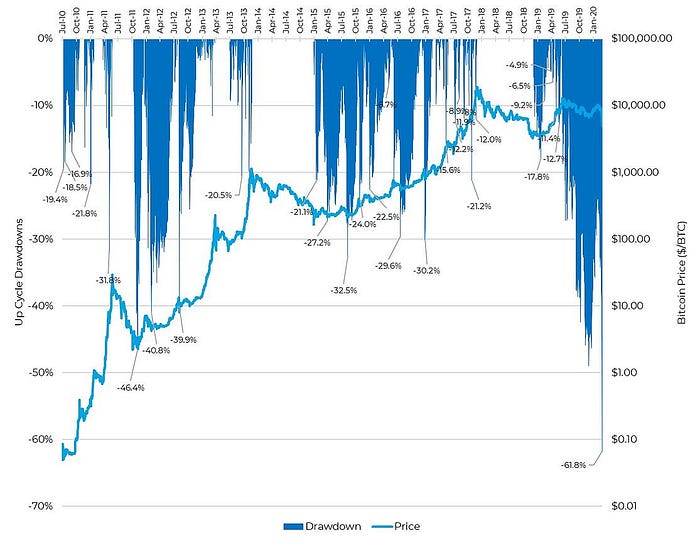

We’re not going to sugar coat it — it has been a brutal few weeks in crypto and in traditional markets. On a relative basis, it has probably been crazier in traditional markets than it has been in crypto. No, we’ve never seen an up-cycle drawdown of this magnitude (-62% — previous worst was -46%) in Bitcoin, by a long shot, but this is a new and volatile asset class. US equities markets, on the other hand, have been around for a lot longer and have never seen a drawdown of this ferocity (% lost/day). Keep this in mind — 22 days ago the S&P 500 was at an all-time high. Now it’s down nearly 27%. That’s a loss of 1.4%/day. The next worst drawdown average -0.82%.day, during the Great Financial Crisis. Keep in mind, we don’t know if a trough has been reached yet.

Proposed Solutions — Are They Enough?

Our belief is the market reaction, which has filtered down into crypto, has be caused by the spread of the coronavirus from China to the rest of the world. A number of solutions have been proposed to this existential threat. Unfortunately, they have been focused mostly on monetary policy (50 bps emergency rate cut, $1.5T liquidity backstop from the Fed) and some fiscal policy (payroll taxes, tax filing delays, increased spending to the tune of $8.3B aimed at combating the coronavirus). However, a comprehensive or coordinated policy response is likely what’s needed to impact the root cause of the issue — the spread of the virus. Our view is that unfortunately, we’re focused on treating the symptoms rather than the cause. What we really need to do is “bend the curve” in the growth of the virus before markets settle down. The data we track has yet to show that in current hot spots — the US, Italy, and Iran.

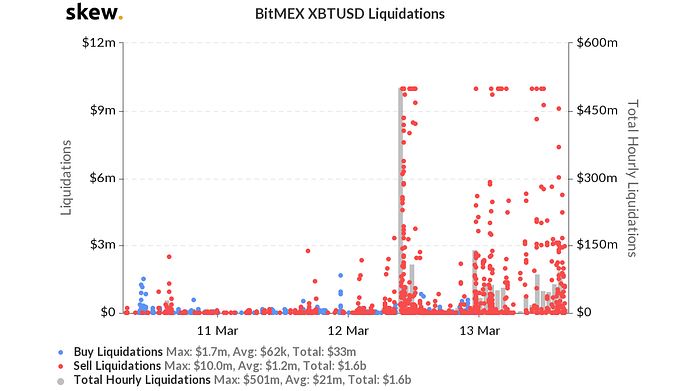

Liquidity Driven Sell-Off

Liquidity and access to it is important for financial markets. When liquidity isn’t available in markets to bring prices to a fair and orderly balance, weird things happen. In traditional markets, it can mean that high-quality companies can’t access credit markets in order to fund liabilities. This was a pervasive issue during the credit crisis of 2008. We actually saw shades of it yesterday as high-quality credit spreads suddenly blew out.

In crypto markets, that can mean that there’s no more dry buying powder, which is what we saw yesterday, and a run in the market can occur. Over the past 24 hours, nearly $1.4B of long positions were liquidated on BitMEX. These are positions that sold according to programmatic rules to bring clients balances back into compliance.

The reason why this is important is because liquidity, in the form of client funds, need to be on the bid side of the programmatic offer to keep prices from free falling. Absent client funds, exchanges like BitMEX and Deribit have set up insurance pools to prevent a cascade of sales. These are pools of fees, a form of socialized losses, which are set aside to backstop this type of situation. But a problem can ensue if the liquidation engine runs though the insurance pool, which is nearly what happened with Deribit. In a recent update, the company itself contributed 500 BTC to the liquidity pool, which had dwindled from 400 BTC to 43. This was spotted by Larry Cermak from The Block:

Deribit’s insurance fund looks a lot better after the additional funding, but it still took a significant step down.

Looking at BitMEX’s insurance fund, it was actually up day today. We’re scratching our heads at that one. Perhaps, liquidation fees that go into the insurance fund were greater than the amount drawn on the fund or perhaps we don’t fully understand how these funds are used. Absent that, we’re at a loss for an explanation. But we’re open to information and education that can help enlighten the situation.

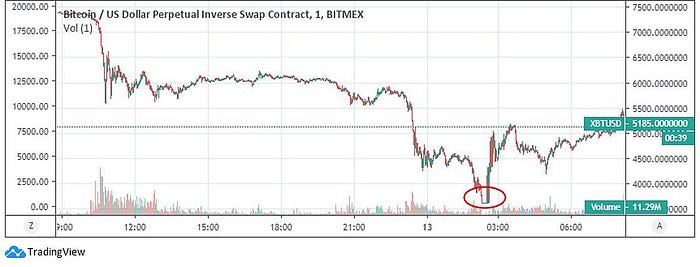

BitMEX Maintenance Saves the Day?

We do know that BitMEX went down for unscheduled maintenance at 2:16 UTC. This was due to a hardware issue at a cloud service provider according to their post. It happened to coincide with the end of the sell-off and a reversal in the price of Bitcoin.

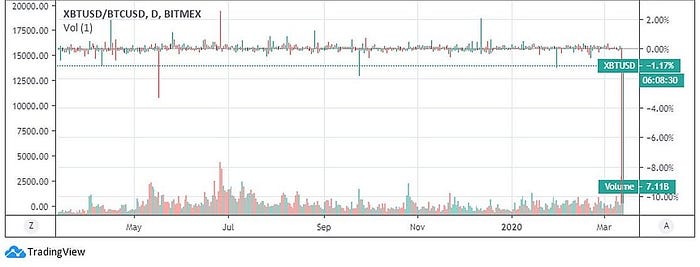

BitMEX’s XBTUSD perpetual product usually trades in close tandem with the price of high-quality exchanges. Using Coinbase as a benchmark, the following graph shows how divergent BitMEX’s price was — up to 10%.

This is very unusual and certainly a sign of stress. Our past research has shown how important BitMEX is to price discovery. Active and passive investors should understand what is happening on derivatives exchanges, simply because they are becoming systematically important to the market structures within crypto. The following chart is from our aforementioned lead-lag study regarding the number of times BitMEX leads prices — the most of any exchange in our study:

Strange Times, Strange Events

We want to close by showing how unique the current market drawdown is (peak to trough price decline). We’ve already shown how extreme the situation is with traditional markets, but Bitcoin is no stranger to volatility. Prior to yesterday’s sell off, Bitcoin has exhibited 4 cyclical drawdowns of over 70%: 2011 (-92.4%), 2013 (-71.0%), 2015 (-84.9%), and 2018 (-83.1%). But once a cyclical low has been put in (up cycle), it had never exhibited a drawdown of greater than 46.4%, until yesterday. Yesterday, Bitcoin had reached an up-cycle drawdown of -61.8%.

That’s all the time we have this week. Please reach out with any questions, comments, or feedback on our work. Get our weekly wrap and daily news delivered directly into your inbox here.