Fairview’s Update and Outlook on COVID-19

Introduction

The goal of this report is to provide the Fairview Capital perspective on the impact of the coronavirus (COVID-19) pandemic on the venture capital and private equity asset class. Fairview has been monitoring the rapidly evolving facts, and leveraging its unique position as one of the most tenured private equity investment management firms in the industry, to provide insights for investors in the asset class. This report is based on industry analysis and Fairview insights informed by communications with its many best-in-class venture capital and private equity managers who are at the front lines of sourcing, investing in, and supporting category leading privately held companies across industries, stages and sectors. As the world grapples with the health and economic consequences of the pandemic, the only constant appears to be uncertainty. At the time of writing, there is uncertainty about its global health implications, the macroeconomic impact, the effects of monetary and fiscal policy responses, and the implications for various asset classes, including venture capital and private equity. We will attempt to make sense of the uncertainty by addressing each of these topics using a scenario analysis based framework.

Macroeconomic Impact

The macroeconomic impact of the coronavirus is in many ways the most clouded with uncertainty and hardest to predict. That said, there appears to be a range of potential outcomes, spanning from the best case scenario of a quick rebound, to the worst case scenario of a prolonged contraction. The consensus base case appears to be a delayed recovery. The disease progression assumptions and the corresponding global economic impact under each of these scenarios are summarized below:

Impact on the Venture Capital and Private Equity Industry

The outlook for the venture capital and private equity industry mirrors that of the general economy in the relatively wide range of potential outcomes currently being contemplated. While the venture capital and private equity industry can expect to see similar negative economic pressures in the short to medium term, history suggests that it is likely to manifest at a lag to the public markets. If history is a further guide, the private markets are perhaps best equipped to respond to and alleviate these economic pressures. This is particularly true since in both venture capital and private equity, dry powder levels are at record highs on an absolute basis. History also suggests that the private markets are the greatest engine for value creation, employment and growth. In fact, 95% of net new jobs created in the US over the last 20 years were from companies less than 5 years of age.[1] Private markets are also best positioned to capitalize on economic dislocations. Private equity funds have outperformed public markets in all 21 of the quarters since 2001 in which the S&P 500 was negative.[2]Indeed, the best-performing venture capital and private equity funds tend to be those that invest at the nadir of a downturn and into the early stage of recovery, when entry multiples are lower, competition abates and portfolio companies benefit from more favorable macro tailwinds. However, there can be no doubt that in the short-term, the venture capital and private equity markets are not immune to the impacts of the COVID-19 pandemic. The following chart summarizes our thinking on the best case, base case, and worst case scenarios for the venture capital/growth equity and buyout sectors.

Organizational and Operational Responses

Fairview’s unique vantage point has served as an advantage in assessing the private market response to the COVID-19 pandemic. At the time of writing, we have formally collected and analyzed responses from over 50 of our general partners executing venture capital, growth equity, buyout, and related strategies to understand their organizational and operational responses to the COVID-19 pandemic. Business continuity plans have been successfully implemented, nearly all employees are working from home, and most physical meetings have shifted to calls and virtual meetings. Travel is strongly discouraged, and when done, self-disclosures are often the norm. The aforementioned holds true for both tenured managers and emerging managers (firms raising newer funds, smaller funds, and/or led by women and minorities).

Aside from emails and phone calls, communication tools overwhelmingly favor Zoom and Slack, two Fairview portfolio companies disproportionally benefitting relative to incumbents. These tools are used not only for internal communications but also for communications between the general partners and the executives at portfolio companies. For example, some managers have dedicated Slack channels to communicate with portfolio companies. Also, with annual meeting season upon us, nearly all physical annual meetings have been postponed or shifted to videoconferences with Zoom, as the primary interface.

Advancements in technology have leveled the playing field by allowing smaller firms to perform essential functions just as well as larger firms. Most firms in Fairview’s portfolios, tenured and emerging, are advising entrepreneurs to implement remote working arrangements and perform scenario analyses during this period of uncertainty. Tenured firms, with experience from previous market dislocations, are able to lean on their more senior partners for guidance in these tumultuous times. Emerging managers appear to be well positioned to compete against tenured firms, even more so than in previous crises, due to advancements in technology and differentiated networks, sourcing, and strategies. These firms often feature smaller teams, niche strategies, and tend to be very nimble.

Portfolio Company Impacts

Beyond deploying business continuity plans, GPs have been actively communicating with LPs while revisiting approaches to portfolio construction, pacing, and investment strategy. As deal making slows, active pipeline deals are being reevaluated and terms are being renegotiated. The majority of GPs though are spending most of their time working with portfolio companies — helping them respond and adjust to the effect of COVID-19 on their business. The impact on portfolio companies will vary widely depending on their stage, sector and business model. The following analysis is based on areas where Fairview has the most exposure and expertise.

From a stage and strategy perspective, Fairview invests primarily in the venture capital/growth equity and small buyout categories. For venture-backed companies, the timing of their most recent capital raise is an important factor. Companies that have raised capital recently are able to modify their costs and business models to extend their runways, while those that need to raise capital soon or are already in the market may be more challenged. GPs are providing tailored advice to their companies and are revisiting their reserve strategies to ensure their best companies have funding available. Putting together a syndicate will become more challenging and some companies may require bridge rounds. Overall, venture capital appears to be in relatively good shape, aided by most firms’ focus on technology-related companies, which have been less impacted than other sectors. Small and mid-market companies in the portfolios of buyout funds are likely to be under the most duress. The market had featured record high levels of debt and entry multiples. Firms that rely on financial engineering and multiple expansion will be highly challenged. Firms that are operationally focused will also have challenges, likely differing based on sector, business model and balance sheet strength. GPs in this category have also been working closely with portfolio companies on an individual basis.

The sector focus of venture capital and private equity firms and their portfolio companies is perhaps the most important factor in how COVID-19 impacts business. Some sectors are benefiting, seeing boosts in revenue due to changes in how people work, communicate and spend their free time. Additionally, some sectors, such as ecommerce, edtech and workforce productivity may benefit from long-term changes in consumer behavior because of the crisis. Conversely, sectors such as tourism, consumer goods and hardware, are experiencing acute challenges and may recover while others may face lasting, long-term challenges.

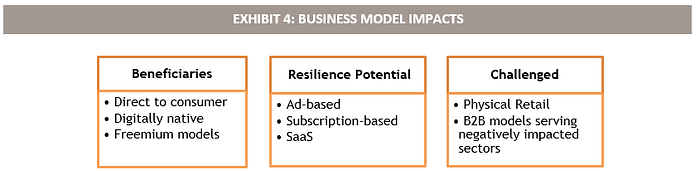

Over the years, we have witnessed the evolution and expansion of business models across stages and sectors. This is another factor that will play a role in determining how companies fare through the crisis. Digitally native, ad-based, and direct-to-consumer models should fare well in most sectors. Freemium models may see a boost and higher conversion rates in certain sectors. Subscription and SaaS models have the potential to be resilient, depending on contract length and terms. Challenged models are likely to include physical retail, and business-to-business companies serving sectors that are negatively impacted.

Across stages, sectors and business models, private equity and venture-backed companies are responding by making operational and strategic changes. Cost-cutting measures are being put in place by impacted companies, including many companies reducing executive pay. Of course, unfortunately, some companies are being forced to furlough or lay off employees. As a way to support cash flow, it has been common for companies to draw down lines of credit while also seeking to accelerate accounts receivable and extend accounts payable. For most companies it appears these measures are temporary, as a means to increase cash flow and extend runway through the crisis.

Fairview Guidance

As one of the most tenured private equity investment management firms in the industry, Fairview has experience managing portfolios through several cycles and challenging market conditions. Our programmatic approach to building well-diversified long-term portfolios featuring best-in-class managers has proven highly resilient. In our experience, a consistent approach to committing capital, through ever changing economic cycles, has been the most successful strategy for long term investors in the private markets. Commitments made to funds this year would likely feature an investment period ranging into 2023 or beyond and it is likely these funds will be able to take advantage of market dislocations and more favorable pricing.

We expect best-in-class venture capital and private equity firms to emerge from this crisis successfully. Most of these firms are tenured and feature experienced managers investing through multiple market cycles. Innovation, the backbone of the venture capital industry will continue unabated. Venture-backed companies are predominantly technology or healthcare companies, two primary areas of economic growth across the world. With public market volatility, IPO activity is likely to slow, shifting even more value creation to the private markets.

Emerging managers will experience a range of challenges, particularly those firms run by inexperienced managers and investing or raising a first-time fund. Sources of capital for emerging managers are already scarce, with a limited number of dedicated investors in the category. Further, many new firms rely on non-traditional or non-institutional sources of capital which are likely to pull back from investing. Conversely, emerging firms run by experienced managers, with differentiated or niche strategies, may thrive. We find that the best emerging firms are generally very adaptive and can move quickly in uncertain times. As always, these firms feature a better alignment of interest, appropriately sized funds and more motivated professionals — all of which are major advantages, particularly in markets like the one we currently face.

In summary, as we look ahead to the rest of 2020, it is clear that the unprecedented crisis presented by COVID-19 will consume our attention as the situation evolves and we digest additional data. We believe that the venture capital and private equity industry embodies the country’s greatest assets — its innovative spirit, ingenuity, its nimbleness of response, and its “can-do” attitude. We expect that many of our portfolio companies will rise to the challenge, and that our managers will continue identifying attractive opportunities in the midst of market dislocations. The best-performing vintages tend to be those that invest at the nadir of a downturn and into the early stage of recovery, when entry multiples are lower, competition abates and portfolio companies benefit from macro tailwinds. Our view is that now is the time to invest. We look forward to sharing our updates with all relevant stakeholders.

Copyright © 2020 by Fairview Capital Partners, Inc. All rights reserved. This publication may not be reproduced without the written consent of Fairview Capital Partners, Inc. This document is for informational purposes only and is not an offer to sell or a solicitation of any offer to buy any security or other financial instrument and may not be used for legal, tax or investment advice.[1] Kauffman Foundation

[2] PitchBook