Active liquidity provider’s Q3 review of Uniswap v3 performance

Subscribe to our Active Assets Weekly Substack newsletter here.

Introduction

In this post we want to share our analysis of what the recent dynamics around of the top pools in Uniswap v3 in terms of volume, total value locked (“TVL”), and fee income since v3’s launch until September 26 2021. In this time period TVL has risen to 2.34 Billion USD on main net, with the amount recently launched optimistic rollups, Optimism and Arbitrum.

The analysis will focus on the top 100 Uniswap v3 pools, breaking down the time series data by fee tier (0.05%, 0.3% or 1% as allowed by the protocol), and by the type of pair of tokens that compose the pool: whether one of the tokens is ETH or a stablecoin, whether it is an ETH-stable pair, or all other pairs combined.¹ The data is derived from the great Uniswap v3 tables provided by Flipside Crypto.

Volume

Let’s begin by looking at overall volume traded² in USD terms on the top 100 Uniswap v3 pools:

Volume traded had it’s peak back in May shortly after launch, but had a significant slowdown in the summer where the volume stabilized a bit below $1 billion USD per day. This reduction in volume in USD terms is necessarily associated with the overall crypto price downturn. Since late August we have seen an increase in volume to a new higher average.

Let’s now look at how this volume looks when we break pools down according to their fee tier:

While the 0.3% pools were dominant early on, by July the 0.05% pool had caught up, and has since dominated in volume, and taking a significant lead in late September.

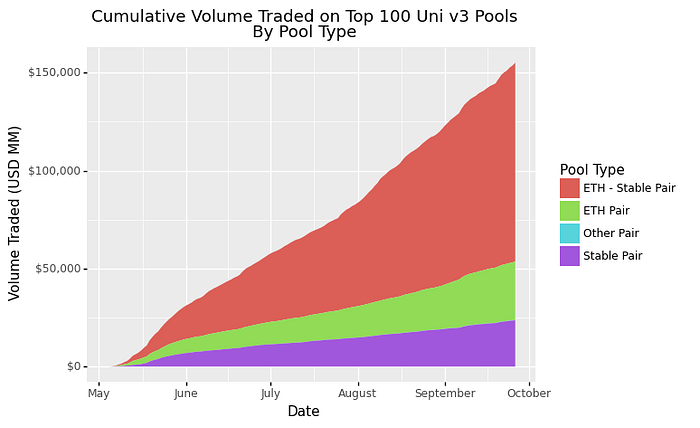

Let’s now look at the cumulative volume traded for the top 100 pools, which is a bit over 150 billion USD for the top 100 pools. First, breaking out this cumulative volume by fee tier:

This chart echoes what we have just seen for raw volume, even thought the 0.05% pools took a while to build up steam, they have since taken a significant share of volume on Uniswap v3, which now rivals the 0.3% pools in cumulative volume.

Now, looking by pool type:

When we look at the cumulative volume by pool type, it is evident that ETH-Stable pairs dominate volume traded (with increasing dominance), while ETH / Stable pairs with other tokens split up most of the rest of the volume. Non-stable or ETH pairs have negligible volume.

Total Value Locked

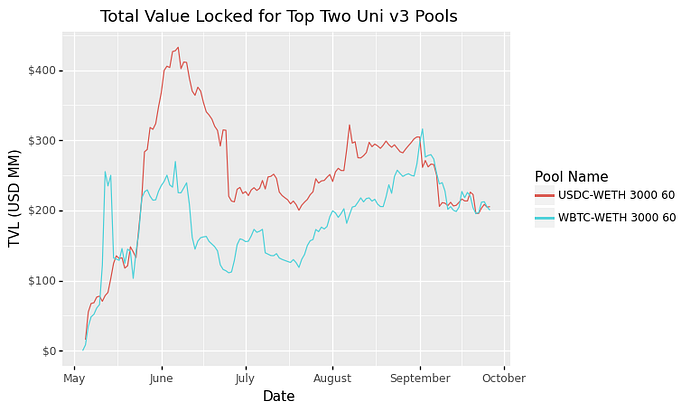

Let’s now look at how much liquidity is locked in these pools. First, let’s look the total value locked (“TVL”) of the top two pools, the USDC-WETH 0.3% and WBTC-WETH 0.3% pools, which by far dominate TVL on Uniswap v3 with currently close to 200 million USD per pool:

The USDC-WETH pool peaked in USD terms in early June at over 400 million USD and is now in the lowest levels since May, while the WBTC-WETH pool had its peak in early September, where it got a bit over 300 million USD. Again, it’s important to note that the TVL in USD terms is heavily dependent on the price of the assets in the pool.

Let’s now loot at TVL for all of these pools on September 26:

We can clearly see the dominance of the USDC-WETH and WBTC-WETH 0.3% pools , followed by the USDC-USDT 0.05% pool as the only three pools with over 100 million USD in TVL. Then we have five pools with over 50 million USD in TVL with a mix of 0.05% and 0.3% fee tiers, as well as ETH / stable pairs. Afterwards there is a long tail of smaller pools, rendering the distribution looking like the typical 80/20 concentration levels.

Let’s now look at thee breakdown over fee tiers:

Here we can see that in terms of TVL the 0.3% pools dominate the top 100 pools with about 1 billion USD at time of writing, while the 0.05% pools have 63% of the size of the 0.3% pools. Given that we have seen that the 0.05% pools have more volume, a natural question arises, which one is more profitable to LP in? We will look at this in the next section.

Fee Income and APR

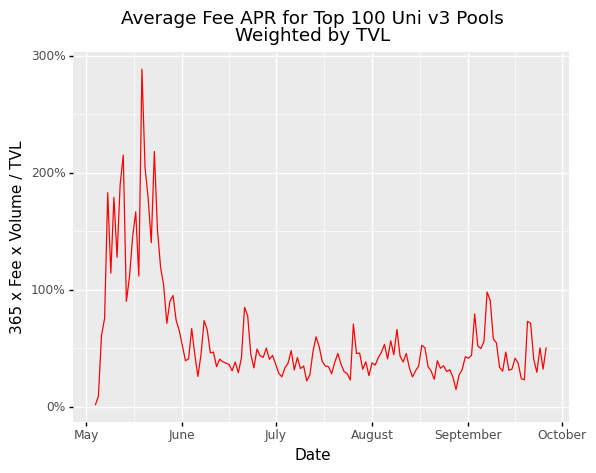

Let’s start off by looking at the average fee income APR, where we weigh the pools by their TVL in order to make the indicator more representative of the typical USD in liquidity in Uni v3’s performance. Note that this analysis abstracts from the advantages of concentrated liquidity and presents the fee APR as if all liquidity was distributed evenly over the price range, as well as ignores potential impermanent loss that could be incurred from LPing.

The weighted average APR had a significant peak in May, but as volume died down and TVL grew, the APR has decreased, averaging a bit below 50% for the past couple of months, with an average of 50.7% on September 26.

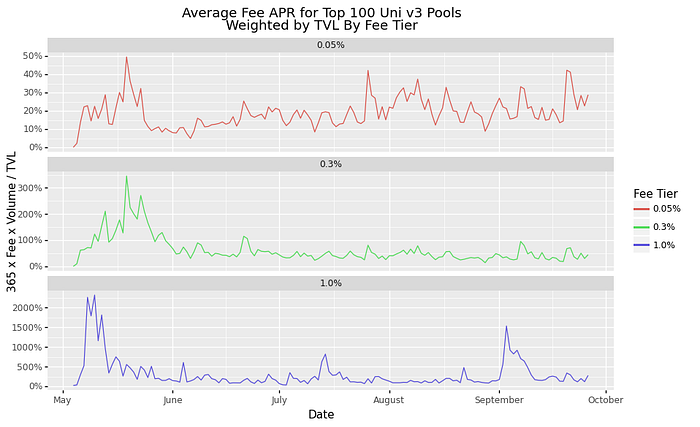

Let’s now break that down by fee tier to see how the different parameters combine to a weighted average APR:

We can see that the weighted average APRs increase by fee tier consistently for the top 100 pools. The 0.05% fee tier averaged a bit below 30% APR recently, while the 0.3% fee tier averaged close to a 45% APR on September 26. The 1% fee tier pools had a massive 282% fee APR, but as we saw from the TVL and volume charts above, this is generated by relatively tiny pools with little volume. Were a material amount of liquidity to be added to these 1% fee tier pools would reduce the APR significantly, while exposing the LP to impermanent loss as the 1% fee tier pools are typically those with more volatile pairs. Due to these considerations we will ignore these for the APR analysis that follows.

Let’s now look at the cumulative return from LPing in the 0.05% and 0.3% fee tier pools, by asking compounding the daily APRs earned since July 1st 2021, a date where the volumes in Uniswap v3 had reasonably stabilized:

Thus, while the volume in the 0.05% pools has taken over recently, when deciding which pool to LP in, you must look at the three relevant variables in combination: TVL, fee %, and volume. This chart shows that when averaged across the top pools, the APR of the 0.3% pools have significantly outperformed the fee return of the 0.05% pools by at least double cumulative weighted average returns. It is important to note again that this calculation ignores concentrated liquidity, which could boost a particular LP’s return in a 0.05% pool above that of the 0.3%. This would typically imply however taking more risk as well.

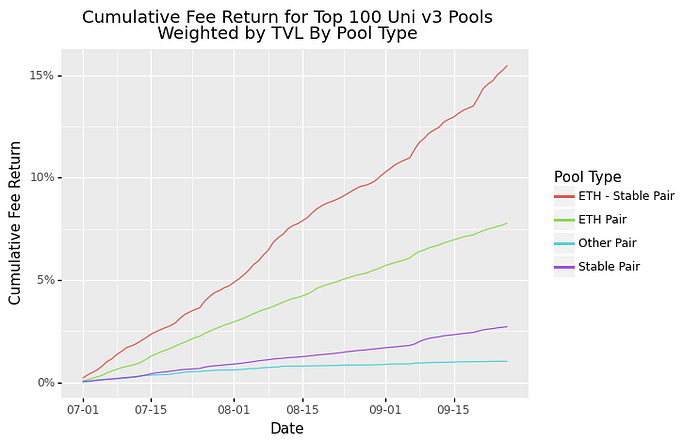

As a bonus, let’s look at how this cumulative return looks at for the pool type breakdown:

The ETH-Stable pairs dominate in cumulative fee return, with a bit above 15% by late September. This is to be expected given the significant share of volume these have represented, and the fact that they are typically 0.3% fee tier pools. Second come the ETH pairs, which are mostly pairs of DeFi protocol tokens with ETH, which are a market where Uniswap v3 has significant presence. Third come stablecoin pairs (without ETH), where the cumulative return isn’t that strong, and the other pairs where a combination of low volume, low fee, or high TVL combine to make a fairly poor return.

Conclusion

When deciding where to LP there are many considerations, with the main variables in terms of income being fee tier, volume, and total value locked in the pool. In this article we looked at the dynamics of how Uniswap v3 pools have behaved since launch, with a particular look at these three determinants of performance, finding the following conclusions:

- Uniswap v3 volumes in terms of USD peaked in late May-early July, and have since found a new, constantly rising plateau, which we expect to keep rising as DeFi grows and ETH valuations recover.

- Volume is dominated by the 0.05% and 0.3% fee tier pools, with the former having a significant increase recently.

- Volume is mostly concentrated in ETH-Stable pairs, with the rest split between pools with either ETH or a stablecoin as one of the pairs.

- TVL in Uniswap v3 pools displays an 80/20 distribution with a few pools dominating most of the liquidity, followed by a (very) long tail of smaller pools.

- Average Fee APR is optimal in the 0.3% rather than the 0.05% pools, indicating that the higher volume of the lower fee pools still doesn’t make up the profitability, given the TVL locked in each pool.

Every week Gamma Strategies publishes analysis and metrics of active asset management within DeFi:

Subscribe to our weekly Substack newsletter and follow us on Twitter

Notes:

¹ For our analysis the relevant stablecoins were USDC, USDT, DAI, FEI, FRAX, PAX, LUSD, OUSD, and UST.

² Volume is measured as the USD value of tokens swapped in, to avoid double counting, per 24 hours.