Technology’s Favorite Curve: The S-Curve (and Why It Matters)

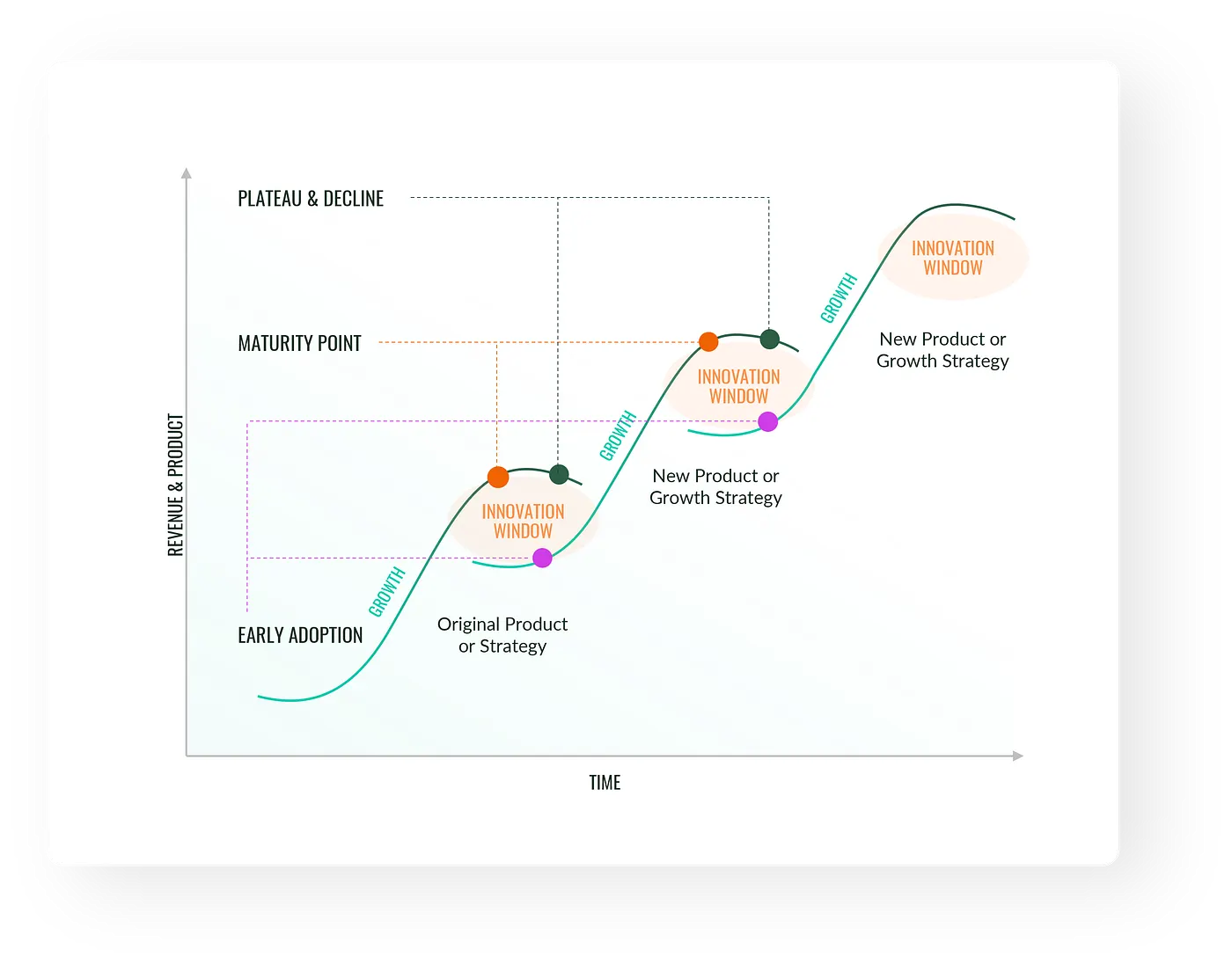

All the technological revolutions of the last few decades tend to follow a similar behavior — the S curve. Technology starts out expensive, bulky, not very widely adopted; Improvement is slow as the fundamental concepts are being figured out. A period of rapid innovation and massive adoption follows, up to a slowdown in meaningful improvement and little new customers. We’ve reached the top of the S-curve — only leaving room for a whole new technology with its own S-curve to come on top.

What hasn’t been written about 2022 so far? The R word (recession), the I word (inflation), Putin-China-red-Nasdaq-Supply-shortage (forget wheat, have you heard of the epidural shortage? Now that’s scary news). But analyzing how the market is responding to these uncertainties (bad), is missing the bigger picture.

Following a conversation with one of my favorite conversation partners (Tal Morgenstern, I’m talking about you), I think we should zoom out and look at the bigger picture of how technology and innovation behave. Spoiler alert: in the very same, highly predictive manner, repeated over and over again.

What’s to an S-Curve? It All Looks the Same

If you look at all the technological revolutions of the last few decades, you can see that they all tend to follow a similar behavior — called the S curve.

- At first, the technology starts out expensive, bulky, not very widely adopted. Improvement seems slow as the fundamental concepts are being figured out (think about the first automobiles, for instance. Development started in 1672, and it was not until 1769 that the first steam-powered automobile capable of human transportation was created.).

- Then there is usually a period of rapid innovation and feature expansion, bringing about massive adoption (this is when engines and cars got better and cheaper, more appealing than a horse and cart and pretty much everyone was buying one).

- Then, as the market matures, meaningful improvement tends to slow down and there aren’t that many new customers to sell to. We have reached the top of the S-curve which is saturated. But -

Now, a whole new technology with its own S-curve can come on top. You can see this in cars (the emergence of electric vehicles), aircrafts, or other inventions. A far more obvious change in the middle decades of the 20th century than in the first decade of the 21st — and you can see it in PCs or in smartphones (the ‘PC curve’ has been completely flat for years and ‘smartphones curve’ is now starting to flatten as well).

Computer S Curve and the Evolution of the Personal Computers

Take computers. We had mainframe computers in the 1970s — HUGE calculating machines that were only used by big corporations or government departments for limited use (like payroll issuances). With advancements in technology, computers became smaller and cheaper. The concept of personal computers emerged, and they became more user-friendly and affordable. But even with cheaper and faster PCs, not every household had a real reason to spend a couple of thousand dollars for what was then a pretty clunky word processor.

But then, a new technological S curve emerged, the internet, which meant that suddenly there was a reason for pretty much everyone to purchase a PC. The internet spread unlocked a whole new, much larger market — we moved from 100 million PCs in the mid-’90s to over a billion PCs today, and we are now seeing a slowing down of the market growth derivative. That’s it — the S-curve cycle for PCs. PCs started out basically as toys in the 1970s and ’80s; They were useful but limited devices for work in the early 1990s; Adoption was then massively accelerated by the internet, and by the early 2000s the technology and its adoption peaked and started plateauing. This S-curve is complete, but:

In the background, a whole new S-curve was starting to brew. That’s when the smartphone (a form of a personal computer) exploded. Smartphones went through exactly the same cycle, and their S-curve would also reach a plateau: Today, there are about 7.5 billion people on Earth, but 6.5 billion of those people already have smartphones. So, the growth has slowed down because we have run out of new customers, and also because smartphone technology itself is plateauing— read “Smartphones are boring now” or the letter Tim Cook sent to his investors after Apple sold (many) fewer iPhones than it had anticipated in the final quarter of 2018. He basically said — “too many good phones are already out there”).

Where is the Money?

Let’s stay with the smartphone S-curve for a moment to understand where the money goes. In the early days of a new tech S-curve, the profits come from the infrastructure; from the companies that invent the breakthrough. With time, it moves to companies who build on top of that infrastructure — apps, networks and new products. The value pendulum moves from infrastructure to the end-user: The iPhone was introduced in 2007, and its massive adoption over the years is what allowed the “end-user companies” to reach 1B monthly users several years later (Spotify in 2011, Facebook in 2012, Instagram, Waze and WhatsApp in 2017).

Where is Israel?

Israel joined the party relatively late, in the mid-80s’ and early 90s’ (right at the beginning of PCs’ S-curve). The first legendary entrepreneurs in Israel came mostly from a hardware background. They met a world that really needed what they had to offer, and they built wildly successful infrastructure companies (MSystems, Amdocs, Nice), establishing Israel, then a merely 5M people country in the middle of nowhere, as a force to be reckoned with. After years of building the infrastructure, the value started shifting from the infrastructure layer to the application layer. But Israeli entrepreneurs did not have a relative advantage when it came to their experience with design, product, marketing and sales. Therefore, we (kind of) watched some major success stories from the sidelines: Web 2.0 (Google in 1998, Twitter in 2006), social media (Facebook in 2004, Instagram in 2010), and online marketplaces (eBay in 1995, Amazon in 1994, Alibaba in 1999, Etsy in 2005, Wish in 2010). Then, Israeli tech was quickly back in the game. Directly evolving from the internet S curve, a new S curve was born — one of Cyber and business intelligence. Here, again, top Israeli talent met a world that really needed what they had to offer, and giants such as Chekpoint (1993), Palo Alto Networks (2005) were born.

The same thing that happened in cybersecurity in Israel happened again with data-focused companies. Look at what happened in 2007. It was a crazy year — other than the iPhone introduction, Facebook became global, VMware IPO’d and enabled any operating system to work on any computer which basically enabled cloud computing. The cloud was born in 2007, the Hadoop project which enabled a million computers to work as they were one, which gave us big data — was launched in 2007, Github, Watson — all launched in 2007. All of a sudden, we had a surge of big data tech innovation. That was an extremely fertile ground for Israeli companies who knew how to use data: Waze (2006), Outbrain (2006), Taboola (2007), IronSource (2010), Dynamic Yield (2011). Israel emerged strong because when the difference between a very successful company and a failing one came down to the data optimization and analysis, rather than the startup’s brand, or it’s ability to design a great UI/UX — Israel has major talent.

Now What?

After several years of busy activity in areas where Israel doesn’t necessarily have a relative advantage, we are again at the beginning of new S-curves that are enabled by fundamental breakthroughs in compute, ML, Biotech, Quantum Computing and more. The pendulum is again moving towards infrastructure. Grove Ventures was built on the premise that the natural movement (from infrastructure to applications and then back to infrastructure) means that there are big dollars hidden in the infrastructure — SW, HW, or anything in between.

I’m an engineer, not a macro-economist or a political scientist, so I don’t have much (intelligent things) to say when it comes to interest rates, inflation, oil prices, the war in Ukraine, or political turmoil in Europe or the US. I know that all the risk factors that were in place early in 2022 seem to remain in place today. But here’s an optimistic graph to end with: difficult market times have never (really) hindered S-curves, and my bet is that they aren’t going to start now: