直观理解,既然STO本身与IPO相近,那么两者的发行流程应该具有相同特征,由不同的机构相互合作行程一条产业链。

相关文章:

本篇介绍STO常规项目的发行路径,以及可能遇到的问题。

STO目前无专门法律规范细节,实务上主要利用传统金融法规进行。因适用范围、归属问题、金融准入条件等因素,加上基于区块链发行的通证能够几乎不受限于国界随意移动,因此在法规解释上多有所争议。

先前我们介绍过STO的标的资产主要可以分为基金、股票、债券和实体资产,本篇对资产与STO的结合进行详细介绍:

最近数字货币市场迎来最大熊市,比特币(BTC)在11月14日突然暴跌,从价格6640USDT一路来到4340 USDT,截至11月29日止,短短16天跌幅高达30%,比特币市值蒸发了约150亿美元。

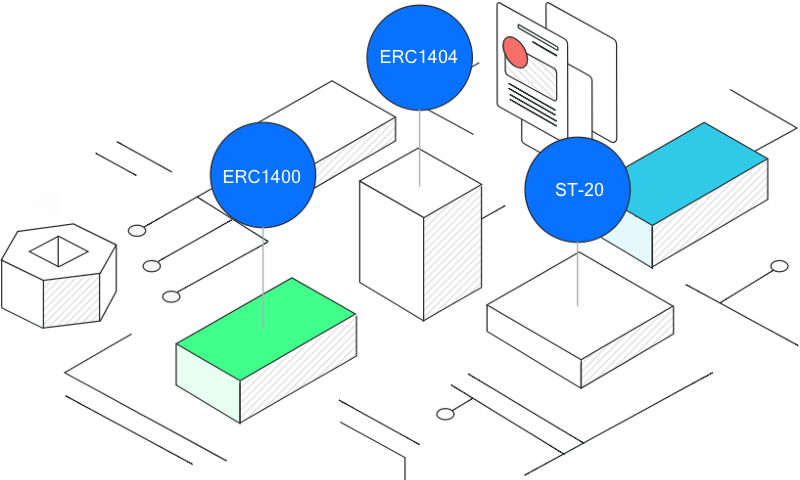

在理解各种协议的不同之前,我们必须先解释Fungible Tokens(可互换通证)与Non-Fungible Token(不可互换通证)的差别。

STO与一般的证券不同,具有以下特殊的优势:

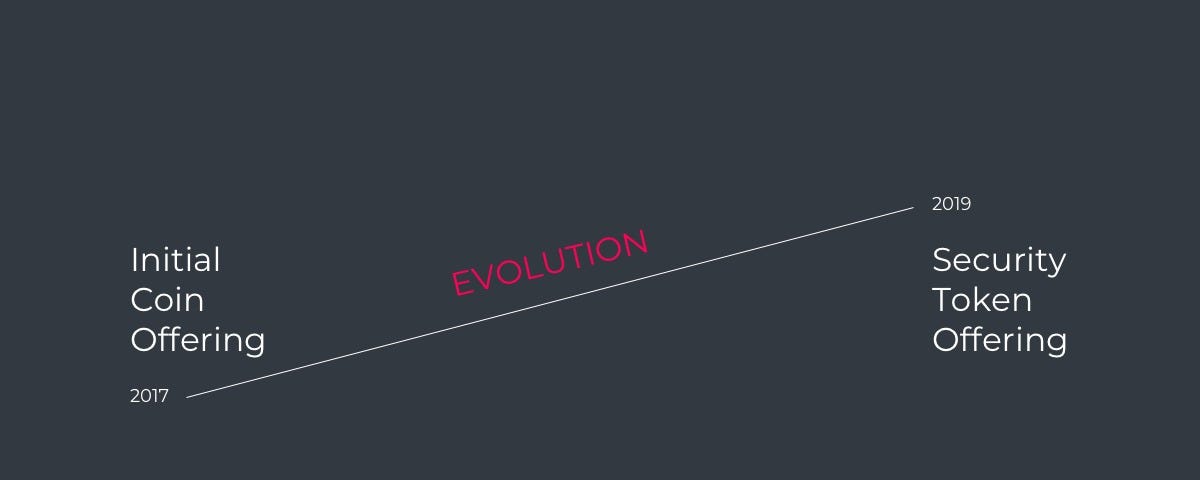

STO的出现除了改进ICO本身的空气币问题,以及IPO成本高、效率低的两大因素外,更重要的原因可以分为两大类: