Is Venture Capital uncorrelated with the public equities market?

When analyzing the effect on ONEVC's portfolio of the first wave of Covid during 2020, we notice that: (i) our portfolio was very resilient to Covid; (ii) our SaaS companies benefited from the pandemic; (iii) no company perished during Covid, and many of them were able to raise additional rounds, two of which had follow-on rounds preempted by funds before going to the market; and (iv) all the companies are experiencing revenue levels higher than pre-pandemic, and the vast majority are at record levels.

Looking at the portfolio performance above, this question becomes natural: Is Venture Capital uncorrelated with the market?

There many reasons for this include the following:

- in many cases, the startups are going after recently created markets or “stealing” market share from the slow-moving incumbents;

- many startups are going after markets that became viable only when abrupt shifts created favorable tailwinds, such as changes in regulations, the rise of new technologies, and a drop in the cost of software/hardware;

- the markups are not in real-time in this asset class;

- in many cases, startups are fighting for a smaller and less competitive piece of the market, whereas incumbents are trying to grow in a more competitive sector over a large revenue base.

This is corroborated by Clayton M. Christensen’s Disruption Theory, which claims that many times, startups begin with a smaller segment that is still ignored by the incumbents — a segment that tends to be less competitive and thus, less correlated to the market. We believe that our portfolio’s behavior during the pandemic is in line with this lack of correlation.

Specifically, as incumbents focus on improving their products and services for their most demanding (and usually most profitable) customers, they exceed the needs of some segments and ignore the needs of others. Entrants that prove disruptive begin by successfully targeting those overlooked segments, gaining a foothold by delivering more-suitable functionality — frequently at a lower price. Source: "What Is Disruptive Innovation?" by Clayton M. Christensen, Michael E. Raynor, and Rory McDonald

In order to provide a few additional insights, we listed some numerical evidence from the market below:

a) Invesco’s whitepaper “The Case for Venture Capital” shows that Venture Capital is not correlated with the large caps in the public markets. The correlation is -0.06, very far from 1.00 (100% correlated) and -1.00 (100% negatively correlated). A “zero” would mean totally uncorrelated.

b) AngelList, with a database of thousands of deals done inside their platform, calculated the correlation between returns from their portfolio and Nasdaq’s. They ended up with a 0.00 correlation; that is, their returns are totally uncorrelated.

c) Finally, even the long-term correlation between Venture Capital returns (using Cambridge Associates Index) and the market (Nasdaq and S&P 500) is very weak.

Should public equities investors consider Venture Capital?

Yes! The first reason is related to the topic above and the second is not:

1. Uncorrelated assets can reduce the risk of a portfolio:

According to the Modern Portfolio Theory, Venture Capital can help investors diversify and reduce risk in an portfolio with public equities.

“Modern portfolio theory (MPT) asserts that an investor can achieve diversification and reduce the risk of losses by reducing the correlation between the returns of the assets selected for the portfolio.” Source: Investopedia

2. Returns are migrating from the public equities market to the private:

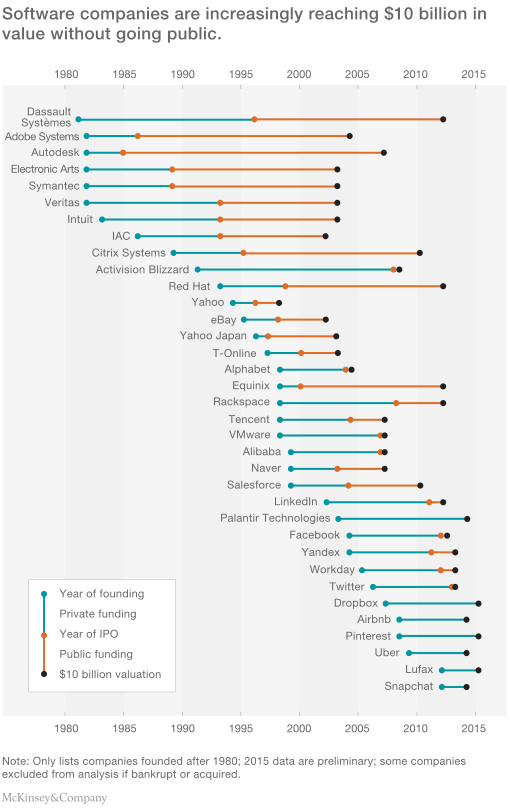

At ONEVC, we have many Brazilian LPs that are moving into Venture Capital. With a relevant increase in the capital available for growth stage investing, companies are taking longer to go public and a the returns are migrating from the public markets to the private markets. See below the study McKinsey conducted showing that statups are now raising more capital with the private market.

"The average age of US technology companies that went public in 1999 was four years, according to Jay Ritter, a University of Florida professor who studies public markets.1 Of the more than 35 public software companies that reached valuations upward of $10 billion from 2004 to 2015, only six achieved that level before going public. The rest reached it an average of more than eight years after their IPOs". Source: "Grow fast or die slow: Why unicorns are staying private" by McKinsey

More about this topic:

In case you are curious about the topic, find below additional sources of information and insights:

- AngelList: Innovation isn’t Correlated with the Markets

- The Case for Venture Capital — Investco

- The Inverse Correlation Between Venture and Public Markets

- Correlation and Modern Portfolio Theory

- McKinsey: Grow fast or die slow: Why unicorns are staying private

The content above was published in ONEVC's monthly newsletter.

Subscribe here.

Bruno Yoshimura — General Partner at ONEVC

Bruno Yoshimura is a Co-founder and General Partner at ONEVC. Bruno has accumulated 15 years of experience as a tech founder with extensive involvement in product development, sales, and marketing. Before pursuing an MBA at Stanford, he launched Kekanto, an online guide based on users’ reviews backed by Accel Partner and Kaszek Ventures, and Delivery Direto, a white-label platform for restaurants doing delivery sold to Locaweb (BVMF:LWSA3) in 2019. Bruno holds a major in computer science from the University of Sao Paulo.