Interest Rates in the DeFi Market (EN)

Recently, DeFi projects like Pendle Finance and the emerging LSDfi have caught the spotlight for their innovative use of interest rates. This trend mirrors the pivotal role of interest rates in traditional financial markets, signaling a rising demand for investment and hedging against interest rate risks. Yet, in the DeFi landscape, interest rates’ role has largely been restricted to their foundational use and as promotional tools, often manifesting as floating rates. Given the considerable room for growth and evolution, this article will explore the fundamental nature and significance of interest rates, their current limitations within the DeFi ecosystem, and what the future might hold.

What are Interest Rates?

Interest rates represent the proportion of interest to the principal amount that a borrower must pay for using borrowed funds. They are instrumental in shaping economic choices such as investing, borrowing, and saving. Central banks in nations adjust interest rates to align the money supply with prevailing economic situations. A reduction in interest rates lightens the borrowing load, fostering consumption and enticing businesses and individuals to invest. Conversely, elevated interest rates promote savings and dampen inflation, thereby fostering economic stability. In today’s financial landscapes, interest rates don’t merely signify the cost of capital; they actively shape pivotal financial decisions including investment, savings, and borrowing.

What Determines Interest Rates?

Interest rates are shaped by several primary factors:

- Central Bank Monetary Policy: The decisions made by a country’s central bank play a big role in setting interest rates. Central banks adjust the benchmark rate, which is a short-term interest rate, based on how the economy is performing. When the economy is growing, they might raise this rate to prevent too much inflation. When the economy is slowing, they might lower it to encourage more spending and investment.

- Economic Outlook: The future expectations of investors about the economy directly impact long-term interest rates. If the general sentiment is positive and growth is expected, long-term rates tend to rise. If there’s pessimism and a potential downturn is anticipated, these rates often drop.

- Risk Premium & Term Premium: “Risk premium” is the extra interest investors expect when they’re taking on riskier investments. “Term premium” is the added interest for holding a bond for a longer period, considering the uncertainties of the future.

Considering these elements, it’s understandable why an inversion of long- and short-term interest rates can signal an impending economic downturn. Typically, long-term interest rates are higher than short-term rates because of the the term premium. But when the market expects an economic downturn, investors seek the safety of long-term bonds to escape future uncertainty, driving the interest rates on these bonds down. Since short-term rates, which are closely tied to central bank decisions, have less room to move than long-term rates, they can end up higher than their longer counterparts. Thus, the difference between the 3-month to 10-year or the 2-year to 10-year bond rates is often viewed as an economic recession indicator in financial circles.

Fixed Interest Rates and Their Significance

Interest rates come in two primary forms: fixed and variable.

- Fixed Rate: With a fixed rate, the interest remains unchanged for the entire duration of a financial instrument or loan. This means that no matter the ups and downs in the wider economy or financial markets, the interest rate is set in stone until the end of the term. For investors, this provides clarity and predictability, ensuring the same amount of interest is paid every month.

- Variable or Floating Rate: This type of rate is dynamic, adjusting in response to the prevailing market interest rates. It usually tracks specific benchmark rates, like SOFR, LIBOR, or the Prime Rate, plus an added risk premium. This arrangement places the risk of interest rate hikes on the borrower but also offers the potential benefit when rates decline.

Fixed rates captivate investors with their predictability. Unlike the erratic nature of fluctuating interest rates, fixed rates ensure a clear return path, eliminating any financial guesswork. This stability is why major entities like pension funds and insurance companies gravitate towards fixed-rate bonds, securing their future obligations. Even corporations can benefit, using fixed-rate bonds to guarantee steady financing and streamline their financial planning. In essence, fixed rates transcend mere speculation; they’re a safeguard against the unpredictable ebbs and flows of interest rates, anchoring long-term financial stability.

Limitations of Interest Rates in the DeFi Marketplace

Interest rates in the DeFi space gained attention during the “DeFi summer” due to activities like “yield farming”. However, since the DeFi market is still emerging, these interest rates mainly serve speculative purposes and come with several limitations.

- Absence of a Standardized Benchmark Interest Rate in DeFi

A key challenge faced by the DeFi sector is the absence of a universally accepted benchmark interest rate. In conventional financial systems, there’s a clear distinction between the benchmark and market rates. The benchmark rate, set by central institutions like the Federal Reserve, accounts for macroeconomic conditions. This established rate acts as a consistent point of reference for all market participants. The market rate, on the other hand, evolves based on this benchmark, factoring in elements such as risk, typically framed as “benchmark rate + basis points (BP)”.

This structural clarity is missing in the DeFi space. Without a consistent benchmark, there’s notable disparity in interest rates across various platforms or blockchains, even for the same cryptocurrency. The decentralized nature of DeFi means there’s no centralized entity to enforce or suggest standardized rates, and there’s a lack of uniformity in how participants perceive and set interest rates. This environment naturally enhances market volatility where it’s not rare to witness sizable interest rate discrepancies on the same platform, often without clear justification. As a result, DeFi interest rates presently struggle to reflect genuine value and often play a more promotional role for projects rather than being an intrinsic component like in traditional finance.

[Example]

- For instance, on AAVE’s Ethereum chain, the supply rate APYs for USDC and DAI were once 8.19% and 10.66%, respectively, while on the Arbitrum chain, they stood at 5.64% and 4.78%.

- The Missing Interest Rate Derivatives Market in DeFi

In conventional financial systems, the interest rate market isn’t just about borrowing and lending; it has a robust derivatives segment. For perspective, the global over-the-counter (OTC) interest rate derivatives market is valued at an impressive $502.6 trillion, dwarfing the $109.6 trillion foreign exchange market. This derivatives market offers investors tools to protect against interest rate changes, as well as avenues for generating returns.

In contrast, the DeFi landscape is predominantly focused on lending and borrowing, and these services often only provide floating rates. This restricts investors from effectively gauging the true value of interest rates since they lack hedging tools to counter the inherent market volatility. Furthermore, the range of products centered on interest rate investments in DeFi is quite limited. Such constraints deter institutions that seek dependable returns, including pension funds and insurance companies, from entering the DeFi space.

Initiatives in the DeFi Market

Recently, there’s been a rise in DeFi projects targeting the constraints of the prevailing floating rate paradigm. These initiatives, primarily centered on providing fixed rates, aim to enhance price discovery in the DeFi space, echoing the influence of the traditional interest rate derivatives market.

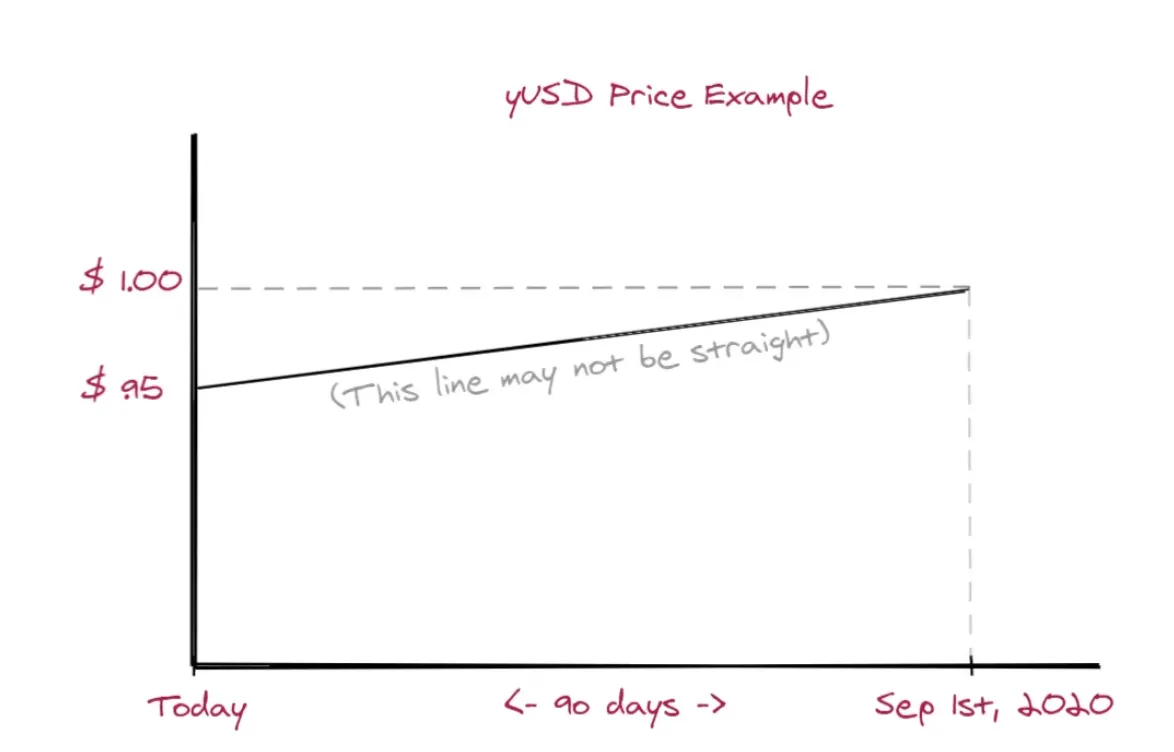

(1) Zero-Coupon Bond

Zero-coupon bonds are a unique type of bond. Rather than being issued at full face value, they are priced at a discount and do not involve periodic interest payments. Instead, investors receive the initial amount they invested plus the accrued interest all at once upon the bond’s maturity. This means that the profit investors make comes from the gap between the discounted purchase price and the full face value received at maturity. Consequently, these bonds guarantee a predetermined rate of return, providing clarity and certainty for investors.

[Example]

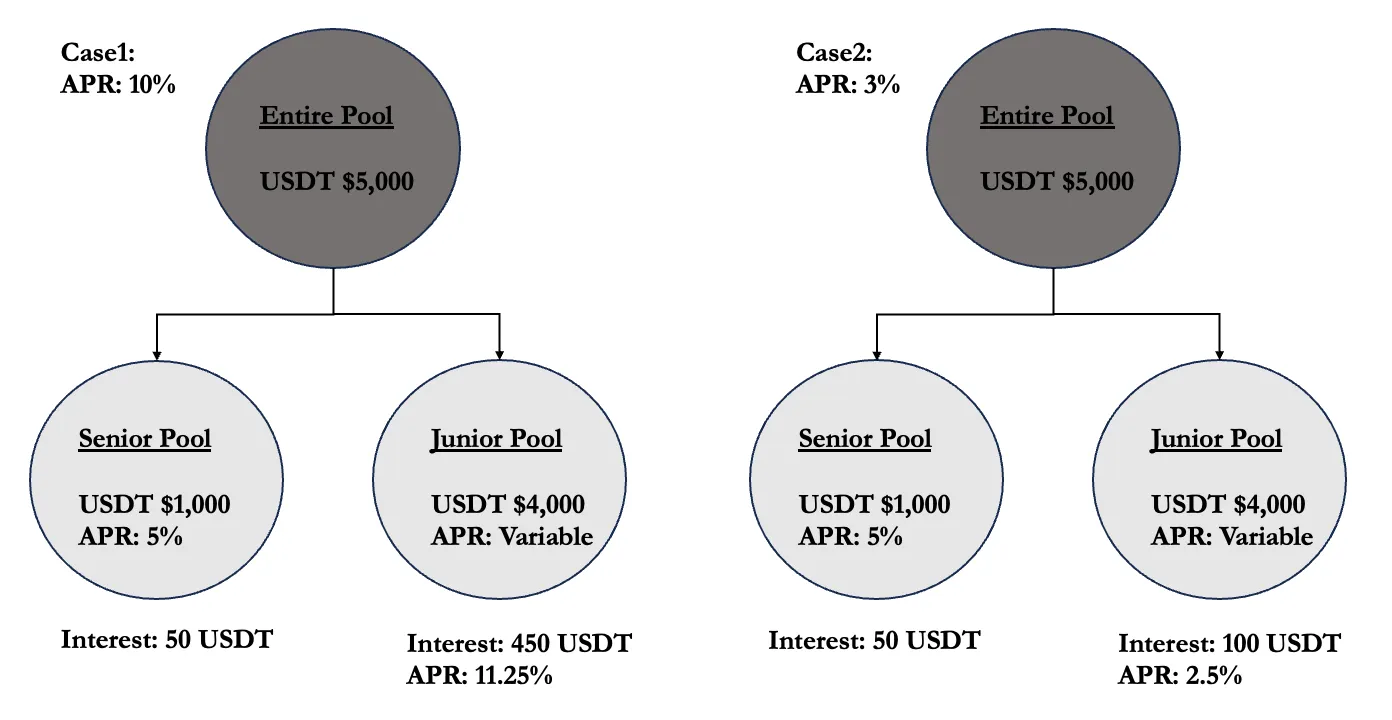

(2) Junior and Senior bond/pool

Bonds are categorized into different classes based on an investor’s risk tolerance. Some investors prefer stable investments with minimal risk at the expense of lower returns, while others seek investment opportunities with higher returns at the expense of higher risk.

Reflecting this investment landscape, the structure of the junior and senior bonds/pools is designed so that the senior bonds/pools receive a fixed interest payment first, and then any remaining yield is paid to the junior bonds/pools. This allows investors looking for a small but stable return with minimal risk to invest in the senior bond/pool, and investors looking for a higher return with more risk to invest in the junior bond/pool.

[Example]

Generally, if the yield from the loan is higher than the fixed rate of the senior bond/pool, the surplus yield is paid to the junior bond/pool. However, if the yield from the loan is lower than the fixed rate of the senior bond/pool, the junior bond/pool may not receive any interest at all.

(3) Auction

Recently, services like Term Finance have adopted an innovative approach by offering fixed rates through an auction mechanism. This method mirrors the U.S. Treasury bond auctions, where the clearing rate (or fixed rate) is set based on the rates proposed by both lenders and borrowers.

[Example] Term Finance uses sealed-bid, single-shot, single-price, second-price, double-auction, and pro-rata on the margin allocation methods.

(4) Yield Stripping

Yield stripping is an innovative technique gaining popularity with platforms like Pendle Finance. It tokenizes principal and interest distinctly, enabling them to be traded separately. This method offers both fixed returns and flexibility in devising investment strategies amidst varying interest rates.

Here’s how it works:

- Principal Token (PT): Represents the principal part of an investor’s original asset. Investors are guaranteed their principal back on a predefined maturity date.

- Yield Token (YT): Reflects the interest component, with its value varying in line with market interest rates.

Investors can choose to sell their YT to navigate market fluctuations, keeping the PT for consistent returns. Alternatively, by retaining YT, investors can employ better/efficient capital allocation or taking positions on interest rates. This duality caters to those wanting a stable yield and those ready to speculate on floating interest rates.

[Example]

It separates the underlying asset into a Principal Token (PT), which represents the principal, and a Yield Token (YT), which represents the interest until maturity. The price of the PT will be equal to the price of the underlying asset at maturity, while the price of the YT will vary depending on the average APY from purchase to maturity.

- In the example above, if the price of stETH on December 26, 2024 is $2500, the price of PT stETH will also be $2500 at expiration.

- The price of YT stETH is determined by the Average Future APY until expiration.

This approach offers investors the opportunity to diversify their portfolios and boost their investment efficiency.

- Anticipating Rising Rates: If you believe interest rates will go up, you can sell your PT and reallocate those funds to purchase more YT.

- Anticipating Falling Rates: Conversely, if you predict a decline in rates, it would be wise to sell off YT and use those proceeds to buy more PT.

The aforementioned projects provide investors with the opportunity to directly invest in interest rates, enabling price discovery and identifying what investors in the market see as the right rate. Additionally, while the market is currently limited to USDC and ETH, they are expected to play an important role in setting interest rates for other cryptocurrencies by acting as a reference rate in traditional financial markets.

[Example]

USDC or DAI or ETH acts as a benchmark interest rate, providing arbitrage opportunities in the above-mentioned projects and shaping the interest rate that the market thinks about → This allows investors to understand the risk of the chain or the risk of the project.

- The interest rate of other cryptos is formed as DAI APY +x bp according to the risk.

- For example, if the borrowing rate for CRV on Chain A is DAI APY +5 bp, and on Chain B’s identical platform it’s DAI APY +3 bp, this suggests Chain A might be perceived as having slightly higher risk than Chain B.

Conclusion

- Interest rates hold significance beyond mere borrowing costs, influencing the global economy profoundly. For investors, they provide an investment benchmark, while for governments, they act as economic regulatory instruments, a role they’ve maintained throughout financial history. Yet, in the DeFi realm, the importance of interest rates is somewhat diminished, primarily due to floating rate constraints. As their relevance in the DeFi space is poised to grow, there’s a pressing need for further development and innovation.

- Recently, the DeFi market has seen the emergence of various projects offering fixed returns. While challenges like liquidity fragmentation and collateral discussions persist, the appetite for fixed interest rates in the DeFi space is anticipated to surge due to these initiatives. Historically, interest rates primarily served as marketing lures to draw in funds; however, with these evolving projects, the role of interest rates in the DeFi arena is set to align more closely with their traditional financial market counterparts.

- To date, fixed interest rates in the DeFi sector have primarily catered to speculative demand, struggling to address essential risk management needs — a crucial aspect for those seeking interest rate swaps. Liquidity constraints further limit the current offerings of fixed interest rate products, making it challenging to tailor trading conditions to meet specific demands. As a result, these products often prioritize offering a fixed return over enabling effective risk hedging. For the fixed interest rate segment to truly flourish within the DeFi ecosystem, solutions that cater to institutional demands and deliver genuine risk hedging benefits are imperative.

Disclaimer

All content in this article is intended to communicate and provide information and is not intended as the basis for investment decisions or for recommendations or advice for investment. The contents of the text are not responsible in any shape or form including matters that pertain to investment, law, or tax matters