The Stablecoin Trilemma and Its Challengers (I)

Algorithmic & Fiat-Backed Stablecoins

Stablecoins have emerged as a crucial element in the cryptocurrency ecosystem, offering a stable value in a market known for its extreme volatility. From facilitating everyday transactions to enabling complex decentralized finance (DeFi) operations, stablecoins are central to the functioning of the broader crypto economy. However, their design involves several complex trade-offs, collectively known as the “stablecoin trilemma.”

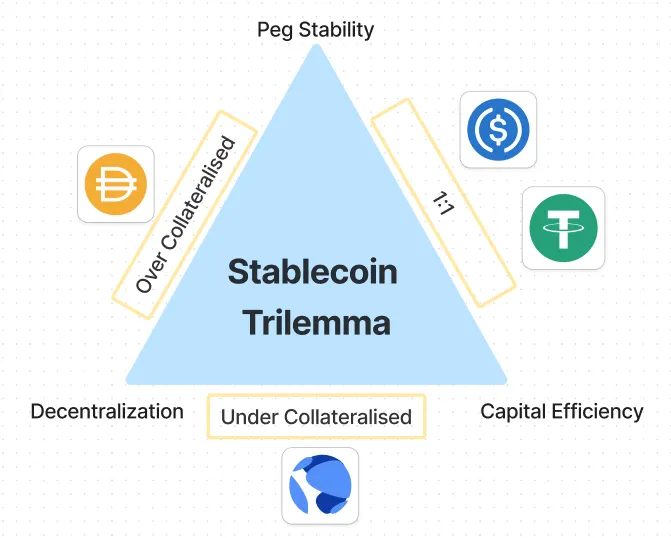

Understanding the Stablecoin Trilemma

The stablecoin trilemma refers to the difficulty – or near impossibility – of simultaneously achieving three key objectives in a stablecoin’s design:

- Peg Stability: The ability to maintain a stable value, usually pegged to a fiat currency like the US dollar. This is crucial for user confidence, as a stablecoin should consistently hold its value.

- Capital Efficiency: The effective use of collateral or backing assets. Ideally, a stablecoin should require minimal collateral to maintain its peg, making the system more efficient and scalable.

- Decentralization: The distribution of control across a network, free from centralized authority. Decentralization is a core principle of cryptocurrencies, ensuring transparency and reducing the risk of single points of failure.

Balancing these three objectives is challenging, and most stablecoins prioritize one or two at the expense of the others. In this article, we’ll explore how different types of stablecoins – specifically algorithmic and fiat-backed stablecoins – navigate this trilemma.

Algorithmic Stablecoins: Innovation and Risk

Algorithmic stablecoins attempt to maintain their peg through algorithms and market mechanisms rather than direct collateralization. The most infamous example of an algorithmic stablecoin is TerraUSD (UST), a project that captivated the crypto world with its innovative approach and dramatic collapse.

TerraUSD (UST): The Rise and Fall

Launched by the Luna Foundation Guard (LFG), UST was designed to maintain its 1:1 peg with the US dollar by using a balancing mechanism with Terra (LUNA), the network’s native token. The idea was that UST could be minted by burning LUNA, and vice versa, creating a dynamic between supply and demand to keep UST stable.

This mechanism, paired with high annual percentage rates (APRs) offered through the Anchor Protocol, attracted many investors and users. At its peak, UST was one of the most utilized stablecoins, and LUNA’s market cap soared.

However, the system’s downfall began when market confidence wavered. A significant sell-off led to a de-pegging event in May 2022, where UST lost its $1 value. As panic spread, the algorithm intended to stabilize UST only exacerbated the problem, leading to a “death spiral” in which both UST and LUNA plummeted in value.

The collapse of UST had wide-reaching consequences, wiping out billions in value and sending shockwaves through the broader crypto market. This event also drew significant regulatory scrutiny and highlighted the inherent risks in algorithmic stablecoins. As you might remember, after LUNA crashed to the ground, the crypto winter grew even colder, ushering in an ice age.

While they may offer high capital efficiency and decentralization, their reliance on market dynamics can make them vulnerable to extreme volatility and loss of confidence.

FRAX: A Shift from Algorithmic to Fiat-Backed Stability

FRAX initially launched as a partially algorithmic stablecoin, backed by both USDC and its native token, FXS. The system managed FRAX’s peg by dynamically adjusting the ratio of USDC and FXS, balancing stability with capital efficiency.

However, after the collapse of TerraUSD (UST), the FRAX team reconsidered its approach. To mitigate similar risks, FRAX is transitioning to a fully fiat-backed model, relying 100% on USDC reserves. This strategic pivot aimed to enhance stability and reduce the vulnerabilities associated with algorithmic mechanisms, positioning FRAX as a more secure option in the stablecoin landscape.

Fiat-Backed Stablecoins: Stability at the Cost of Decentralization

In contrast to algorithmic stablecoins, fiat-backed stablecoins like Tether (USDT) and USD Coin (USDC) maintain their peg by holding reserves of fiat currency or equivalent assets. This model provides strong peg stability and capital efficiency, making these stablecoins indispensable in the cryptocurrency market.

Tether (USDT): The Pioneer

Tether (USDT) was one of the first stablecoins to be widely adopted, and it remains the largest by market capitalization. Each USDT is theoretically backed by one US dollar or equivalent assets held in reserves. This model has proven effective in maintaining Tether’s peg, even during significant market volatility.

However, Tether has faced persistent scrutiny over the transparency of its reserves. Questions about whether USDT is fully backed by dollars or if Tether holds riskier assets in its reserves have led to regulatory investigations and market skepticism. Despite these concerns, Tether continues to dominate the stablecoin market due to its liquidity and widespread adoption.

USD Coin (USDC): The Regulated Alternative

USD Coin (USDC), issued by Circle in partnership with Coinbase, positions itself as a more transparent and regulated alternative to Tether. USDC reserves are regularly audited, and the stablecoin is fully backed by cash and short-term US Treasury bonds. This transparency has made USDC a popular choice among institutions and DeFi projects seeking a reliable stablecoin.

However, even USDC is not without risk. In early 2023, the collapse of Silicon Valley Bank (SVB) affected USDC, which held some of its reserves in the bank. This led to a temporary de-pegging of USDC, with its value dropping to around $0.90 as market participants feared potential reserve losses. While the situation was eventually resolved, it highlighted the vulnerability of fiat-backed stablecoins to external financial shocks, even when fully collateralized.

Centralization Risks and the Stablecoin Ecosystem

Both USDT and USDC illustrate the trade-offs inherent in fiat-backed stablecoins. While they offer strong peg stability and capital efficiency, they are centralized entities that rely on trust in the issuing company. This centralization introduces risks, such as regulatory intervention, reserve mismanagement, or banking crises like the one that affected Circle.

Moreover, the centralization of these stablecoins contrasts with the broader ethos of decentralization in the crypto world. Many users and developers are cautious about relying on centralized entities, which could be subject to censorship, blacklisting of addresses, or other forms of control that undermine the permissionless nature of blockchain technology.

Despite these concerns, fiat-backed stablecoins have become an essential part of the cryptocurrency landscape. Their stability and liquidity make them indispensable for trading, DeFi, and even cross-border payments. However, their centralization and associated risks mean that the search for a more decentralized yet stable solution continues.

Conclusion: The Stablecoin Trilemma in Action

The stablecoin trilemma presents a fundamental challenge for the cryptocurrency industry. Algorithmic stablecoins like TerraUSD and FRAX (in its initial form) aimed for decentralization and capital efficiency but struggled with stability, especially during market stress. Fiat-backed stablecoins like USDT and USDC offer stability and efficiency but at the cost of decentralization and the introduction of trust-based risks.

Each type of stablecoin represents a different approach to solving the trilemma, and their successes and failures provide valuable lessons for the future of digital finance. As the market evolves, we may see new models emerge that attempt to balance these trade-offs more effectively.

In the next article, we will explore crypto-backed stablecoins, focusing on ‘DAI’, a decentralized and over-collateralized stablecoin that has become a cornerstone of the DeFi ecosystem. Despite its low capital efficiency, DAI has achieved significant success by leveraging the utility of Ethereum and maintaining a robust decentralized structure. We’ll examine how DAI has navigated the trilemma and its impact on the broader cryptocurrency market.

We hope this article has given you a deeper understanding of the stablecoin landscape and the challenges these digital assets face. Stay tuned for the next installment, where we’ll dive into the world of crypto-backed stablecoins and their role in the future of decentralized finance.