Maximize your Portfolio Returns for the US Elections

Coauthored with Anthony Tan

Introduction

With less than a month to the election day, the election season is reaching a climax. Although polls, as shown below, indicate a clear Biden win, an upset is still very much possible, just like the previous US Presidential Elections.

Nevertheless, an expected Biden victory or a renewed presidency by Trump can still have profound impacts on the equity markets. Investors who experienced the recent 2016 Presidential Elections may remember the 250 points surge in the DJIA on the day President Trump clinched his unexpected victory. As elections bring about much uncertainty for investors, how would the results of the upcoming elections affect your portfolio this time?

Historical

We took the historical S&P 500 data starting post-World War II and looked at the one day returns of the market after the elections results was announced. Because the political party of the incumbent President can also influence the nature of the country’s economic policies, we also decided the group the victor according to his party — Democrats or Republicans.

Daily/Monthly Change

Visually, a Republican win seems to have a positive correlation to market performance the day after the elections, as well as 1 month following the elections. 50% (5 out of 10) of Republican wins results in a positive market reaction in the day immediately after the result was announced. This is compared to a Democrat win where there are larger swings and more volatility in the markets. 25% (2 out of 8) of Democrat wins result in a positive market reaction in the day immediately after the result was announced.

These findings also apply to the 1-month time frame, where a Republican win seems to result in a more positive market performance.

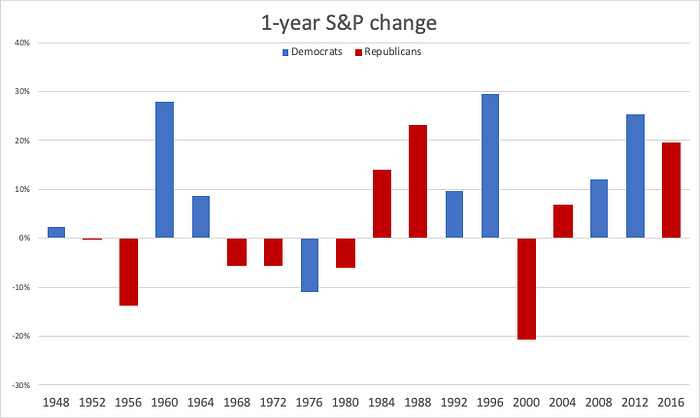

Yearly Change

However, taking a longer term perspective, we looked at the returns one year into the term of each newly elected President. The trend is reversed when we look further into the 1-year horizon. The Democrats have an outsized impact on the markets just one year into their term, where they are both more likely to observe positive returns, as well as higher highs and lower lows compared to the Republican counterparts.

The 2020 Presidential Elections

Moving back to the present, we will take a long term view at the trends that will be driven by the potential winner of this elections as well as the potential assets that stand to benefit from these trends.

Biden Win

Overweight tax-efficient sectors like REITs and utilities, clean energy sector, and Asian equities

A Biden win is largely expected and many have suggested that the markets have already priced in this fact. However, we argue that Biden-friendly stocks still have much more run for growth and appreciation should he implement his policies during his tenure.

Tax increase

Among others, Biden’s tax plans include an increase in capital gains and dividends tax rate from 23.8% to 39.6% on America’s top earners, a corporate tax hike from the current 21% to 28% and increasing taxes on foreign income of multinational corporations.

While the first thought that comes to mind might be a market crash due to lower net income of companies, there is actually a short term spike since tax bills take some time to be passed. Goldman Sachs expects this to come into effect only in 2022. Before then, firms would rush to declare dividends and investors rush to lock in their gains at the existing tax rates, causing the short-term spike. This effect was seen in 1986 during the Reagan tax plan, when the capital gains tax rates were increased from 20% to 28%. In the months before the new tax rates took effect, capital gains realizations surged by 60%. Again when top tax rates were set to rise from 15% to 23.8% in 2012, capital gains realizations hiked 40%.

Post-tax hike, however, S&P500 companies are estimated to take a 9.2% hit on expected earnings according to estimates by BofA Global Research. However, the net impact will potentially be cushioned by greater fiscal spending and elimination of tariffs. By industry breakdown, REITS and utilities are relatively less tax-sensitive compared to the rest of the industries, as REITs funds that distribute at least 90% of their profits as dividends are tax-exempt at the fund level and utilities companies are better positioned to pass on tax increases to consumers. Some REITs and utilities funds to consider are:

- REITs: Realty Income (NYSE: O), National Health Investors (NYSE: NHI)

- Utilities: NextEra Energy Inc (NYSE: NEE), Invesco Solar ETF (NYSE: TAN)

On the other hand, investors may consider avoiding multinational corporation with a high revenue stream from overseas. According to FactSet, domestic revenue accounts for only 43.5% of total revenue of tech companies, benchmarked against the 60.3% across all S&P 500 companies. As such, it could be wise to underweight on the FAANG or tech stocks in general.

Green Energy

In July, Biden announced a comprehensive USD 2T plan dedicated towards increasing use of clean energy in the transportation, electricity and building sectors. Biden’s plan outlines specific and aggressive targets including to achieve an emissions-free power sector by 2035. Most clean energy stocks are already rising as the polls point more towards a Biden win. In August he reiterated his $2 trillion, four year climate plan designed to move energy policy away from Big Oil and towards green energy, These policies are expected to reduce carbon emissions and create up to 10 million jobs by crafting a green energy infrastructure.

To benefits from the boom in green energy infrastructure should Biden win, investors can look at individual stocks like:

- Sunrun Inc (NASDAQ: RUN), which is US leading residential solar company

- utilities such as NextEra Energy (NYSE: NEE) who have embraced renewable generation or electric vehicle

- clean energy companies such Tesla Inc (NASDAQ: TSLA)

For a broader base exposure to the sector, investors can look to the following ETFs:

- Invesco Solar ETF (NYSE: TAN) which tracks companies in the solar energy industry

- Invesco WilderHill Clean Energy ETF (PBW), which tracks US companies engaged in the advancement of cleaner energy and conservation

- SPDR S&P Kensho Clean Power ETF (NYSE: CNRG) which tracks companies driving innovations behind the clean energy sector

Eased US-China tensions

Since the US-China trade war started in 2018, equity risk premiums in Asian countries has been heightened. However, it is likely that foreign policies will likely be less hostile and tariffs reduced/eliminated under a Biden presidency, causing Asian stocks and currencies to rise. ETFs you may consider include:

- iShares MSCI All Country Asia ex Japan ETF (NASDAQ: AAXJ)

- Invesco China Technology ETF (NYSE: CQQQ)

Trump Win

US-China relations will remain frail, while military-related equities benefit from increased military spending

Should Trump clinch a re-election, he will likely maintain status quo with his policies with little to differ from his first 4 years in the office. This means a combative and protectionist approach to international trade as well as a strong commitment to national security, to name a few.

Trade

International Trade was one of the focal points of Trump’s first presidency term. The country slapped tariffs on more than $500 billion worth of Chinese goods, all while portraying China as the bogeyman for unfair trade policies (as claimed by President Trump himself). US-China trade tensions heightened to a trade war, with both parties retaliating each other with further protectionist measures in 2018 and 2019. However, these trade tensions have been easing since January 2020. Both countries have repeatedly held talks to move forward with Phase One of the US-China trade deal, which has since seen increased tariffs exemptions by both countries as well as record deals on US commodities by China.

Nevertheless, we believe that should Trump get elected for a second term, his long-term strategy will remain the same: paint a negative picture on China’s trade practices, and continue to impose some protectionist measures on their economy. It will be unlikely for US-China trade tensions to ease significantly under the same President who has been on the offensive against China throughout his first term. As such, US companies with large supply chain or revenue reliance on China may continue to be adversely impacted.

Looking forward, we foresee that Vietnam is likely to remain a winner for the US-China trade war, where the economy has shown a 7% growth owing to shift in production lines away from China to Vietnam, and an increase in demand for Vietnamese exports. Investors can consider the following funds to increase their exposure to Vietnamese equities:

- Vietnam Enterprise Investments Limited (LON: VEIL) — the longest running fund focused on Vietnam which invests primarily in listed and pre-IPO companies in Vietnam that offer attractive growth and value metrics, and strong corporate governance

- VinaCapital Vietnam Opportunity Fund Ltd (LON: VOF) — a fund which invests companies in Vietnam or in companies with a substantial majority of their assets, operations, revenues or income in, or derived from, Vietnam

Military Spending

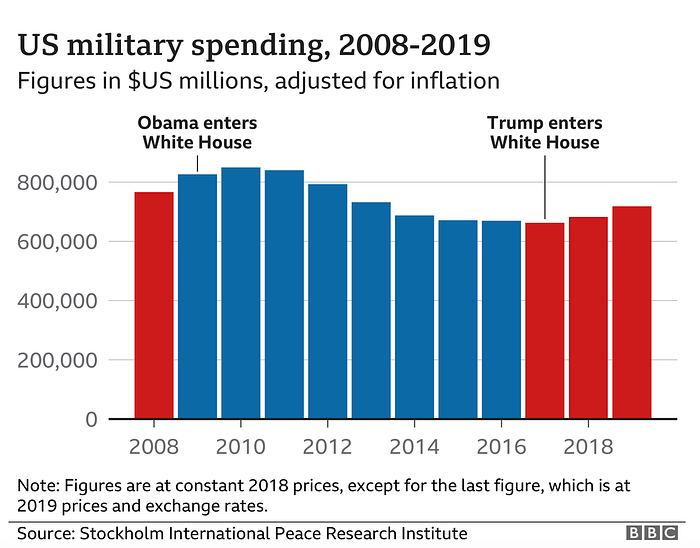

President Trump has been very vocal about his desire to build a strong military. Since taking over the White House, the president has largely delivered on his promise on reversing budget cuts from Obama’s administration. While military spending levels did not reach record levels unlike in 2010, there has been a considerable increase in annual US military spending under Trump. In fact, the president authorised a whopping USD$738 billion defense bill for the fiscal year of 2020, which is added USD$21 billion from the previous year. The increasing trend is very likely to continue in the coming years should Trump continue to serve a second term. Meanwhile, most analysts predict future budgets cuts to the military if Biden and the Democrats win the election.

Should investors want exposure to the defense sector in anticipation of a Trump victory, the following equities are worth noting:

Individual Stocks

- Lockheed Martin (NYSE: LMT) — the world’s largest defense contractor, with half of their annual sales contributed by the U.S. Department of Defense

- Raytheon Technologies Corp (NYSE: RTX) — one of the largest aerospace and defense manufacturers in the world, and also a military contractor which gets a significant portion of its revenue from the US government

ETFs

- SPDR S&P Aerospace & Defense ETF (NYSE: XAR) which tracks companies the aerospace and defense portions of the S&P Total Stock Market Index (TMI)

- iShares U.S. Aerospace & Defense ETF (BATS: ITA) which seeks to track the investment results of an index composed of U.S. equities in the Dow Jones U.S. Select Aerospace & Defense Index

Either way

US dollar is expected to face huge downside in the short to middle term

Regardless of the winner of this election, the US dollar is expected to face huge downside in the short to middle term. This is due to the widely expected release of another US Covid stimulus bill regardless of who’s sitting in the office as well as the Fed position that the benchmark interest rate will remain at near zero through till 2022.

US Covid stimulus bill and fiscal deficit

Should the second US stimulus bill pass as widely expected, uncertainty is expected to be reduced in the markets. This reduction in uncertainty will allow investors to take a more risk on mentality, rotating out of the USD safe haven, exerting a bearish force.

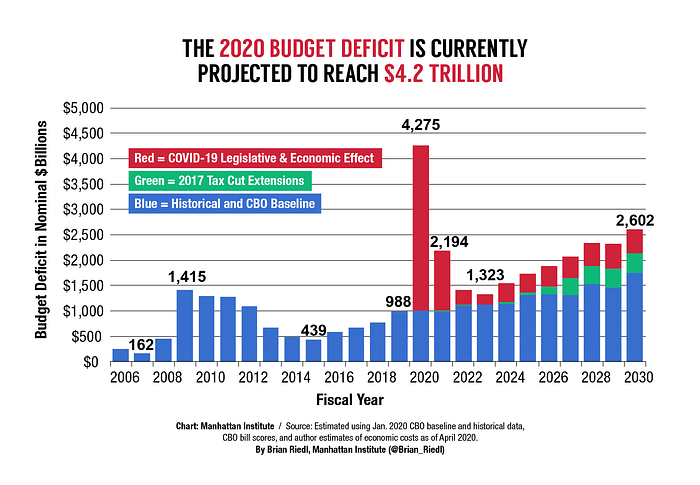

Furthermore, according to the Manhattan Institute, the US Federal deficit is expected to expand dramatically in 2020 should yet another relief bill be passed. Domestic savings are insufficient to fund these deficits and the US may require capital inflows from foreign savers. However, given that with the Covid-19 situation, deficits are expanding globally and these foreign investors will require a discount either in the form of higher yield or a weaker USD. Given the US treasury rates are almost at its all time lows, a depreciating USD is expected to be the only valve for a increasingly worsening US fundamental.

Near Zero US Benchmark Interest Rate

The low expected benchmark interest rate will reduce the allure of holding USD due to its low returns especially when compared to other countries with better growth prospect and higher benchmark interest rate. This widening of interest rate differential between USD and other currency baskets is expected to be a bearish force to the USD as investors seek for yield.

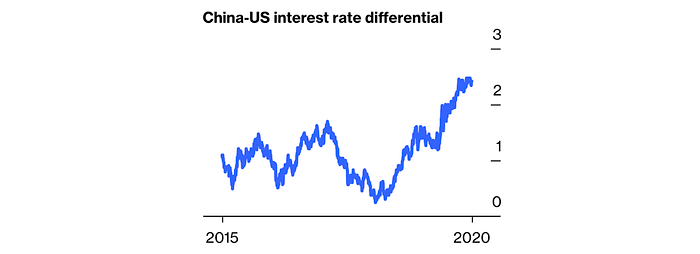

Perhaps a good example would be the CNY, China growth prospect remains good as businesses are slowly resuming having handled the pandemic relatively well. Should Biden win the election and ease the geopolitical tension between USA and China, investors will see more certainty in the prospect of the China market. On top of that, China government bonds pays a much higher interest rate than the corresponding tenor of the US, this interest rate differential as shown below is expected to entice investors to rotate out of USD to seek CNY denominated bonds.

However, it has to be noted that should the US Stimulus Bill continues to be dragged out, uncertainty will continue in the market with a risk off mentality, this could prove to be a bullish force for the USD as a safe haven currency.

Conclusion

With a controversy filled election season in the peak of the Covid-19 pandemic, this election will go down as one of the most important one yet in the history of the United States of America. As volatility is expected to increase as we draw closer to the elections, investors should take a long term view and hedge their portfolios accordingly, participating in the major thematic trends brought upon by the next President.