The Podcasting Endgame: A Paradigm Shift for the Audio-Industry

Key takeaways:

- Podcasting started as a small niche without meaningful revenue but grew into a global phenomenon but the externalized nature of the revenue model causes inefficiency for all stakeholders

- Podcast-aggregators like Spotify are starting to internalize the revenue model into a true digital platform-model to decrease friction and increase their margins

- The move marks the beginning of the digitization of audio-advertizement and whoever “wins” podcasting is likely to play a major role in this battle

Introduction

Podcasting describes spoken audio content which can be accessed on demand. It has become a remarkably widespread phenomenon in recent years. More than half of all US consumers have ever listened to a podcast with around 40% being monthly listeners.

And the trend will only continue as demand drives supply and vice versa: the top two reasons why consumers do not listen to podcasts more are 1) that there are not enough available on topics they are interested in (65% of respondents) and 2) few well-known personalities have podcasts (60%).

The good news for podcast-consumers is: more supply is sure to come as the business model of podcasting undergoes a fundamental change. This article outlines how. Let’s start with where we came from.

Phase 1: Podcasting as a pre-revenue niche

In the early days, podcasting was mainly a sort of talk radio with the advantage of being on demand. Apple had added the app seemingly as a gimmick and barely invested in it in the past 10 years. In terms of revenue: there was almost none to be made. Only radio stations would use their existing advertiser base to “sell” their additional audience’s attention to. The “business” — for the most part — looked something like this:

Podcasting continued to grow in a virtuous cycle: new listeners led to new content suppliers which led to more diverse content and thus more diverse listeners. Other aggregators emerged and music streamers like Spotify joined the distribution game. At some point the space became interesting enough for advertizers and monetization was viable.

Phase 2: Podcasting as a growing phenomenon with a decentralized revenue model

As podcasting matured monetization became possible. Today this is mainly done in two ways:

- Content creators get paid by advertisers for delivering their message right into your ear.

- Content creators monetize their most loyal customers on services like Patreon where they receive payments for additional, exclusive content.

As the graphic shows these processes have been external to podcasting aggregators such as Apple or Spotify:

If the chart looks a little complicated that is because it is. As creators, customers and advertisers lack ways to coordinate through the aggregators themselves, new businesses jumped in to fill the gap.

The status quo shown in the chart has a few important pain points for stakeholders:

- Creators face a lot of friction when trying to monetize their content. Both reaching out to potential advertisers and building a following on services like Patreon requires time and scale often leaving smaller creators with little or no income.

“Sponsors and ads chew up a TON of time that I’d rather spend finding and doing cool things I can share”. (Famous podcaster Tim Ferris)

- Creators lack good feedback from their audience and are limited to rather rudimentary data provided by the aggregator (although these have seen improvements already).

- Advertizers have very little feedback and measurability when using podcasts as a channel. They rely on data provided by creators but have a hard time tracing ROI through rather archaic measures like mentioning unique links on air.

- Consumers have limited ability to interact with the creators. Besides leaving a rating (unavailable on Spotify) or writing an email listeners cannot give input on what they liked or disliked about a show/an episode nor have easy ways to financially support their favorite creators.

- Aggregators/ platforms have not profited from advertising or additional payments but mainly used podcasting as a retention lever.

All these pain-points demonstrate the friction which comes with the externalization of the podcasting business model.

But the good news is: players like Spotify are recognizing the opportunity and make strategic moves to internalize the podcasting business (see my article on Spotify’s acquisition of the Joe Rogan Experience).

Phase 3: Podcasting becomes a centralized revenue model

Companies like Spotify have realized that podcasting could be the space which finally makes audio streaming a sustainably profitable business. Music streaming has the inherent disadvantage of high variable costs (royalties are paid per stream) which makes profitability hard even at scale. To make this point clearer: Spotify pays 65 cents to labels for every Dollar it earns with premium subscriptions with other COGS adding 8 more cents to variable cost.

Podcasting on the other hand knows no royalty system but can be monetized by platforms in three ways:

- Podcasts can increase user acquisition and retention thus improving topline of the aggregators/ platforms. In podcasting this only works well when content is exclusive to the platform as other content can be found free elsewhere. This is the reason why Spotify started to acquire some

- Advertizers pay for having their message heard in podcasts. This monetization can work much better at scale as YouTube has proven in video streaming. As I argue below, audio-streaming platforms are sure to internalize and optimize this revenue model.

- Avid listeners pay directly for additional content. Sites like Patreon allow users to access additional content or merely support their favorite artists/ creators with small subscriptions. This can also work brilliantly at scale although the threshold to viability might be a bit higher than with an ad-supported model. While this is the most contentious move, I expect that platforms like Spotify will internalize this revenue stream at least in the medium to long term.

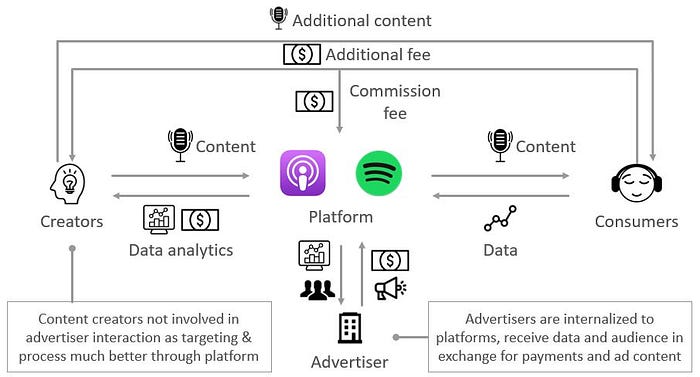

Given these three main monetization models podcasting is now moving towards a business model which looks something like this:

As platforms internalize revenue streams, external services will become redundant.

Whether direct payments and an extensive ad-network will coexists right away (or ever?) remains to be seen. However, we can see most stakeholders are better off when all aspects of the podcast business model are centralized:

- Creators spend less time and effort acquiring advertizers and have less friction when aiming to get direct payments since no external subscription is needed. Very popular creators will see riches similar to the most popular YouTubers while even smaller ones can survive on steady ad-revenues.

- Advertisers will get much better targeting and thus ROI as Spotify inserts ads dynamically and tailored to the individual listener and content being played. Digital audio advertizing will finally become better than radio as user data analytics is leveraged more efficiently (or as Google would say: “Welcome to 15 years ago!”).

- Consumers will benefit from more high-quality content as revenue opportunity attracts more creators who will spend more time creating content. Not unlike YouTube’s push to pay creators this will transform podcasting to on average more diverse and better produced content.

- Streaming platforms will increase revenue and margins as they can take commission on both ad-content and direct payments. Moreover, retention and growth could be fuelled as streaming makes another leap beyond mere music streaming.

- External revenue systems (like patreon) will be disintermediated by platforms like Spotify. As Spotify allows users to pay creators directly in the app for additional subscriptions Patreon will become less relevant to podcast creators. However, this part of the internalization is most contentious. YouTube also chose not to include such a model. Including additional

So (almost) everyone can win in this scenario — yay! But what is the bigger picture here? Let’s examine the potential long-term implications of this shift.

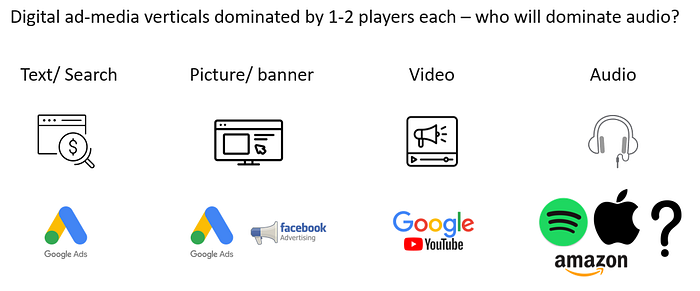

The end game: who will dominate audio advertizing?

The shift towards a more centralized business model for podcasting will mean no less than a fundamental shift of non-music audio advertizement towards the internet.

The advent of widespread digitization of non-music-audio makes advertizing a viable business model. While music streaming has horrendous gross margins and is thus mainly a subscription play, podcasting can be a viable advertizing business.

As such, podcasting can both improve ARPU for users on their advertizing product and attract both users and content providers from the $40B/year radio market.

First, let’s see what the potential of improving ad-profitability is:

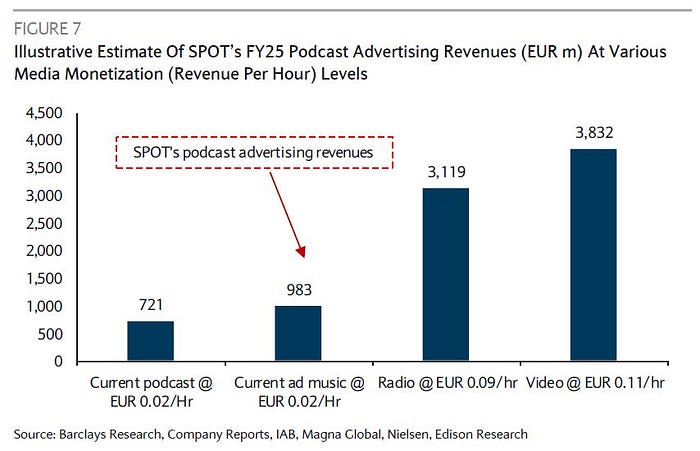

Currently, advertizing on e.g. Spotify generates 2 cents of revenue per hour listened. This is ~78% lower than on radio which has no targeting, no data analytics and no personal information on its customers. Players like Spotify, however, already have all this in place.

Thus it would even be conservative to assume that advertizing revenue can grow 4.5x only by making it a serious part of the podcasting distribution business.

Surely, some of this will have to be shared with the creators but even if 50% go to creators (as on YouTube) potential for players like Spotify is still 2.25x growth.

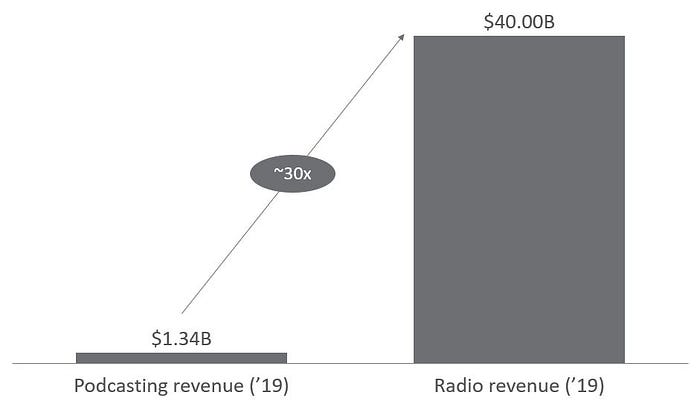

Second, let’s compare the global podcasting market to the radio market which players like Spotify will surely gain share from:

Globally, radio is a $40B industry. According to Barclay’s that is about 30x the size of global podcasting advertizement in 2019. Most consumers listen in cars or at home. As mobile data costs falls and connectedness in cars and at home increases users will shift towards digital audio streaming services.

As music is already widely streamed, other programming must follow to replace radio. Many radio stations already have their talk programs on streaming services in the form of podcasts. As the advertizing service on Spotify becomes better targeted, advertizers will skip radio channels and go directly to Spotify Advertizing as analytics and ROI are prone to be better.

Conclusion & a caveat

Podcast-providers are moving towards a centralized advertizing platform. In doing so they will overcome friction and inefficiencies for all stakeholders involved. At the same time, their business will grow and become more profitable than music streaming leading to a significant advantage for players like Spotify.

As for the future audio-advertizement a great part will be decided in the eCommerce space through players like Amazon or Apple with their voice-assistants. However, content remains king in audio which leaves a great deal of the pie for digital audio platforms. Exactly how this tension might play out in the future shall be discussed in another article.

Disclaimer: I wrote this article in my personal capacity. All opinions are my own and do not reflect the opinions of current or former employers or associates. None of the opinions expressed here should be taken as investment advice.