SYMMIO: the path to hyper capital- efficiency

SYMMIO’s pre-trade capital efficiency is unrivaled because streaming quotes do not require locking capital. With ACOs, post-trade efficiency will be elevated to match.

Summary

SYMMIO provides an intent-based, secure, and hyper capital-efficient infrastructure for on-chain derivatives trading, improving both traders and market makers’ experience:

- SYMMIO enables hyper capital-efficient market making, as traders’ required risk exposure can be fulfilled just-in-time without any pre-locked liquidity. Contrary to order books and liquidity pools.

- SYMMIO’s intents are “pre-solved”: market makers stream their quotes!

- SYMMIO expands the universe of synthetic assets tradable on-chain. The current PERPS offering is larger than with any competing on-chain infrastructure. More products will follow.

- On-chain cash settlement also means secured trading: traders benefit from the flexible offering of CEX and CFD brokers, without any FTX-type counterparty risk.

This paper explores the current state of development, the trade-off in contract designs, and how to bring next-level capital efficiency.

Post-trade, collateral management of isolated positions involves a trade-off between capital efficiency (minimizing margin) and gas costs. We argue that a class of operators called ACOs (Automated Clearing Operators) can radically improve post-trade capital efficiency by:

- acting as an additional insurance for traders

- enabling cross-positions ( optimising margin requirements, for instance netting long and short positions ) for market makers

Analysis

Pre-trade hyper-capital efficiency permits on-chain trading of arbitrary products with deep liquidity

Derivative trading protocols that depend on order books or liquidity pools face the challenge of having to rent and pre-lock liquidity for the markets they offer. This model is unsustainable as it leads to high trader costs and/or depletion of protocol or liquidity providers’ funds.

SYMMIO tackles this issue by introducing a revolutionary solution: just-in-time, on-demand liquidity. With SYMMIO, market makers have the ability to seamlessly stream their quotes across virtually unlimited assets without any cost of locking or “forking” their liquidity. This innovative approach eliminates the need for renting liquidity in advance, providing a more sustainable and efficient model for derivative trading protocols.

The issue: post-trade collateral management involves a tradeoff between capital efficiency and gas costs

Symmio’s core contracts are bilateral and fully collateralized, providing both individual and systemic security that is beyond question.

However, from the perspective of a market maker, there is a tradeoff between capital efficiency (which implies high leverage) and associated gas costs.

The solution: Automated Clearing Operators (ACOs)

This security/capital efficiency trade-off can only be solved by introducing a non-redundant party, ACOs, that provide the necessary guarantees to the traders while enabling market makers minimal margin.

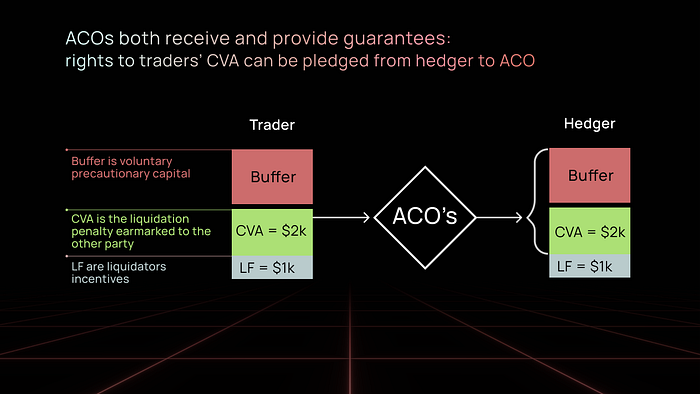

ACOs can act as insurance, providing capital (e.g. CVA + buffer) to the contract in lieu of market makers to ensure they avoid liquidation. In their relationship with the hedger, they can resort to traditional off-chain agreements (share of profits, rating of hedgers,…) as well as to on-chain guarantees.

In the core contract, LF is the liquidation incentive given to liquidators (in case of liquidation), while CVA is the liquidation bonus given to the other party whose risk profile is involuntarily changed.

In practice, market makers are much more seldom liquidated than traders; a market maker can thus benefit from ACO services, giving as a guarantee rights to the traders’ CVA in case of liquidation.

In this simple schema, ACOs are approved to add collateral to the hedger position; market makers, in turn, can pledge their rights to traders’ CVA as a guarantee. Market makers can pledge much more: borrow/funding, and the full sub-accounts!

Implementation choice: contingent vs hard capital

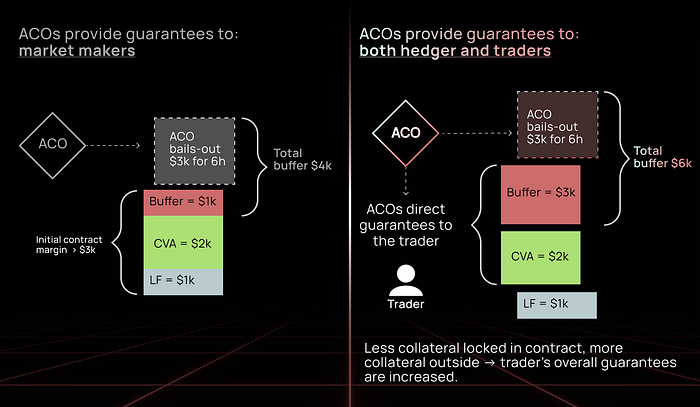

One of the most important design choices is whether an ACO solely guarantees the market maker it will provide additional capital to the contract (on behalf of hedgers), or whether it can directly insure traders (if they agree to substitute hedger CVA by greater ACO guarantees).

(L) On the left-hand side, the trader enters an unchanged contract; the ACO only gives the market maker guarantees that it will inject additional capital into the contract to avoid hasty liquidations, leaving them time to redeploy capital to the contract.

(R) On the right-hand side, the trader agree to replace some of the hedger guarantees (part of the CVA locked in the bilateral agreement) with even greater guarantees from the ACO.

(L) vs (R): A rational trader would accept substituting some guarantees if it leads overall to greater security and capital efficiency altogether.

Can we increase BOTH post-trade capital efficiency AND traders’ security?

A first-best contract maximizes expected value for both parties, trader and market maker.

Security results from two forces, margin requirements and external guarantees.

- Relaxing the strict requirement of constant over-collateralization introduces additional risk

- External guarantees from Automated Clearing Operators (ACOs) add to traders safety

In an initially overcollateralized contract, the primary risk is the failure to realize market gains.

Relaxing hedger margin requirements increases the risk for traders of not being able to realize their gains. Suppose a long BTC trader: in the event of ACO failure during a BTC bull run, the hedger subaccounts would be underwater faster.

ACOs, however, are expected to minimize the risk of hedger liquidation, giving traders greater assurance that they will be able to realize their gains. ACOs could indeed use their own funds on top of hedger cross-positions to maximize traders’ safety.

Conclusion

The on-chain derivatives market will only stand shoulder to shoulder with tradfi and centralized derivatives exchanges when it can provide market makers (“liquidity providers”) with superior capital efficiency.

SYMMIO’s implementation of the intent and Request for Quote (RFQ) architecture is hyper capital-efficient, more than traditional exchanges; we show that pre and post-trade capital efficiency can be optimized, and on-chain gas costs minimized.

Technical Appendices

Specification of trader’s ACO approval

While ACOs could act solely in the interest of the hedger, they maximize capital efficiency if they are able to provide valuable guarantees to traders and in turn lead to an overall reduced maintenance margin.

ACOs must naturally be approved by the traders when opening the positions; ACOs act as insurance for traders, and we expect few provenly robust ACOs to dominate the landscape.

The traders must agree on a maximal amount of ACO guarantees and thus on a reduced hedger margin. An arguably safe choice to set the hedger liquidation threshold just above LF (liquidators’ incentives), with ACOs paying traders at least the CVA bonus in case of hedger liquidation.

Technical design choices: verification of ACO guarantees:

- from a dev/contract design choice, the easiest is to require ACOs to post a bond to the contract to avoid hedger liquidations

- the most efficient is having contingent capital available on-chain, to many sub-accounts, acting as additional guarantees in case a hedger contract is underfunded (permitting withdrawing necessary funds possibly including a CVA bonus, depending on the agreed hedger liquidation threshold)

Specs: adding third-party rights to bilateral contracts

From a contract perspective, traders can enter into extended bilateral agreements with the additional optional characteristics:

- Initial collateralization: from fully collateralized in the sub-account, to partial external collateralization (cross-position pot)

- Allowance for reduced maintenance margin: in percentage and in time (e.g. allowance for 5% under collateralization for 2 hours)

- In turn, allowance to halt liquidation by providing a bond

- Access to pre-defined cross-position pots (hedger and ACO) — when a trader closes a hedger’s under-collateralized position, or when ACOs liquidate a hedger’s position

- Delegation (allowance to ACOs to manage hedger collateral, rebalancing from one sub-position to another, if the ACO also acts as a collateral manager)

- Transferable contract rights: traders’ CVA can be pledged to ACOs. In fact, ACOs can potentially size the full market maker position ( including the market maker lf, CVA, and additional buffers to be recovered when the trader close their positions )

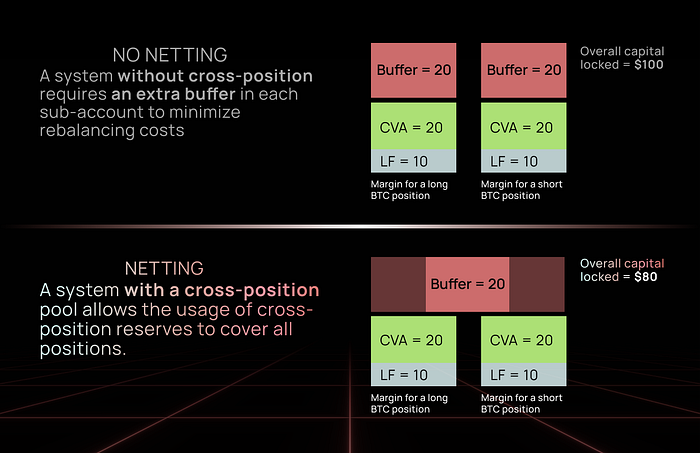

Netting via Automated Clearing Operators (ACOs)

Fully collateralized sub-accounts (aka isolated positions) maximize trader security and isolate the system from systemic risk (on bad position has no direct nor indirect bearing on others).

Risk isolation, however, diminishes capital efficiency, because positions that naturally offset (such as a long and short position) each require a margin.

One of the key benefits of ACOs is to permit isolated positions to be considered as cross-positions, leading to an overall reduced maintenance margin.

This sole feature is illustrated with a minimalist ACO, a simple cross-position buffer.