Part 1 of the MBA Guide to Dealing with Higher Mortgage Interest Rates

The economics of buying a house have changed dramatically since the end of 2021. Interest rates are going up for the first time in a long time. Rates have already gone up a lot as of June 2022…and it seems possible that they could continue to increase quite a bit more.

Related

• 4 Lessons on When to Sell $400,000 Worth of Stock in an Unpredictable Market

• When Is a Stock Market Crash Not Really a Stock Market Crash?

• When Is a Bear Market Not Really a Bear Market?

• MBA Guide to Higher Mortgage Interest Rates, Part 2 — How Much Money Will You Save?

Recent

• The Deafening Silence on Stock Buybacks from Centrist Democrats

• 2 Reasons Populations Are Collapsing in Developed Countries

• 3 Key Facts Everyone Is Missing About Biden’s Student Loan Debt Relief

Potential to Change the Way You Think

• Why Are Fundamental Human Values Critically Important for Successful, Enduring Brands?

• Life Expectancy vs. Healthcare Costs in the U.S. (and Japan, Germany, France, Spain, Portugal, etc.)

• (1a/9) “Top-Down” Makes More Sense Than “Left-Right” in the U.S.

This is Part 1 of a series of three articles on non-obvious ways of dealing with these high(er) interest rates as best as you can and decreasing the amount of mortgage interest you pay.

In this first of three articles, I’m going to:

- Cover some basics so we’re all on the same page as we go forward.

- Discuss at least one item that traditional mortgage lenders never spend time talking with you about — the total amount of interest you pay on a mortgage over the 30 or 15 years. This is central to the material in the second and third articles. That’s when we will discuss how you can put more of the money you’d otherwise pay your mortgage lender — potentially a LOT of that money — back in your pocket/bank account.

- Set the stage for Part 2 and Part 3. This is where I will offer some different ways of thinking about your mortgage payments that might just be “paradigm-shifting” for how you approach managing your mortgage.

First I’d like to invite you to subscribe to receive emails when I publish new articles — such as Part 2 and Part 3 of this short series over the next few days. I’ve been thinking about the topic of mortgages for 20 years now, and I have some original material that I look forward to sharing with you.

A few caveats up front:

- I’m not a licensed financial advisor. Do your own homework after reading this (but if you have questions I can answer or help guide you with, please post them in the comments section below.)

- I’ve never worked in the mortgage lending or banking industries. My interest in mortgages and how they work began about 20 years ago when my mom was refinancing her mortgage and had to make decisions about type of mortgage, etc. I created a spreadsheet for her that — as much as possible — would be in “regular person”-speak. I wanted it to be something where she could play with the numbers at a high level and get a real sense of how the money worked on this really big financial decision she was about to make. Fortunately I have enough of a quant background as an engineer and enough finance and economics experience from coursework in business school and professional experience over the past 25 years to be able to dive in deep, question a lot of the conventional wisdom around mortgage, and think creatively.

- I am not invested one way or the other in residential or commercial real estate or any housing/real estate stocks or other investment vehicles. It doesn’t matter to me if you buy a house or not — I do not benefit financially either way. My only goal is to help you make the smartest decision(s) you can so that you keep as much of your money in your own pocket as possible.

Buying a home is the largest purchase that most people make in their lives.

But nobody really helps the typical person buying a house understand the relevant numbers except in very shallow, superficial, less-than-useful ways.

Let’s change that now.

The first three sentences of this article are worth repeating:

- The economics of buying a house have changed dramatically since just the end of 2021.

- Interest rates are going up for the first time in a long time.

- Rates have already gone up a lot as of June 2022…and it seems possible that they could continue to increase quite a bit more.

The interest rate landscape has changed dramatically in the past year, particularly over the past 8 months. Higher rates have arrived, and they seem to be here to stay for a while. They may also go higher, but it is impossible to know that for sure.

We can’t predict the future of where interest rates will go with certainty…but let’s speculate a bit.

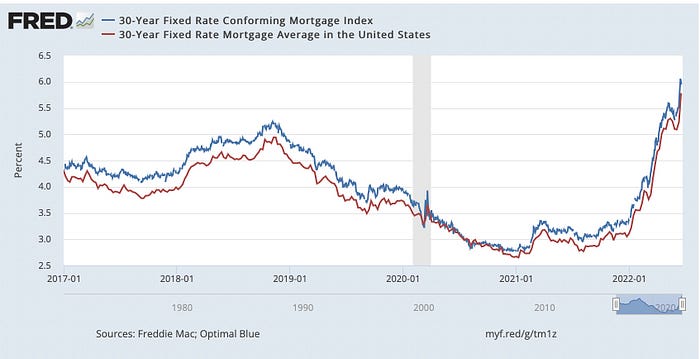

First, look at the 5-year chart below from the Federal Reserve Bank of St. Louis. This is a big jump in interest rates for 30-year fixed-rate mortgages, no question.

(Btw, if you’re ever looking for economic research and data, the FRED resource that the St. Louis Fed makes available online for free has excellent material.)

The 30-year fixed rate has roughly doubled over the past 8 months from 3.171% on Nov. 5, 2021 to 5.989% on June 16, 2022.

But when I look at this longer-term 50-year chart of mortgage rates, 5 things jump out at me:

- There WAS a 40-year long-term trend of decreasing mortgage rates that started back to the early 1980s. We have broken that trend.

- The “big jump” in interest rates over the past 12 months that looked so dramatic on the 5-year chart doesn’t look nearly as big on this 50-year chart, does it? It seems as though we might only be getting started with interest rates rising. Hmm….

- If I just eyeball the 50-year chart, the long-term average mortgage rate over the past 50 years looks as though it’s probably in the 8–10% range. So even though we are already up to the 6% level, we would still need to go quite a bit higher to get to what seems like the longer-term average.

- It also seems like a natural thing that in the process of getting back to a longer-term average level, we could perhaps OVERSHOOT the average. If so, we would go higher than the 8–10% range I mentioned earlier.

- The last time the Fed was trying to burn inflation out of the U.S. system by increasing interest rates — in the late 70s/early 80s — the Fed Funds Rate went up to a high of 20.61%, which helped cause 30-year mortgage rates to increase all the way up to 18.39% in late October 1981.

Whoa. People are screaming today about the inaffordability of buying a house with interest rates at 6%. And yet Boomers were somehow still managing to buy houses in the 1980–1985 timeframe when 30-year fixed rates stayed above 12.5% for almost that entire 5 years…?

I’m not trying to sound alarmist or apocalyptic about the possibility that interest rates could go as high as they did in the early 80s.

However, my sense is that because:

- the Fed and the federal government have pumped so incredibly much “free-ish” money into the system and also shot prodigious amounts of money over to Wall Street, etc. over the past 15+ years, and

- corporations, the government, people, politicians, etc. have all had decades now to get very, very used to unnaturally low interest rates,

it will be a much MORE difficult task getting rid of inflation today than it was back in the early 80s.

And it wasn’t so easy back in the early 80s, either.

That said, I suspect the political climate today will not permit the Fed to raise rates as high as Paul Volcker was able to get away with since he had President Reagan providing political support for high interest rates in the early 80s. I don’t see either Biden or Trump having similar political will and/or political desire as Reagan did during his first term.

We shall see.

The first “number” that the cable news networks and mortgage lenders NEVER discuss with you is “total amount of mortgage interest paid.”

Let’s start with “total amount of interest paid” over the course of an entire mortgage.

For now, I am less concerned about the actual interest rate — whether it’s 5.00% or 5.70% or 6.50% — than I am with “how much money total will I pay over the next 30 years just to cover the interest costs of the mortgage?”

While you probably already have a sense that the “total interest paid” number goes higher as the interest rate goes higher, you may not fully appreciate how much higher and how rapidly “total interest paid” increases as interest rates go up.

For instance, on a 30-year fixed-rate mortgage at 6.00% for a $500,000 home with a 20% ($100,000) downpayment, the total interest paid over 30 years will be $463,353.

When you add in the original principal amount of $400,000 for this 6% mortgage, that means you will be paying the mortgage lender a total of $863,353 over 30 years.

Back when the 30-year fixed-rate mortgage interest rate was only 4% — i.e., just a few months ago — “total interest paid” would have been only $287,478.

That means the 2% jump — from 4% to 6% — added almost $176,000 in total interest costs to what you’d be paying over 30 years. That is $176,000 that you won’t have for your retirement or your kid’s college tuition or for family emergencies.

Somehow this piece of information never — and I mean never — comes up in stories on cable news or in newspaper or magazine articles.

Today in late June 2022, 30-year fixed rates are around 6.00%, but as I said earlier, I can imagine us going substantially higher in the coming months and quarters.

So while you certainly need to be careful that your personal monthly cashflow can handle the monthly mortgage payment, it’s also important to be mindful of how much money in interest you are committing to pay your mortgage lender over the next 30 years.

For the average family in America, these extra hundreds of thousands of dollars that you are committing to pay your lender over the next 30 years would make a huge difference for retirement planning, college savings, and just having extra money for life’s pleasures and for life’s uncertainties.

For many families, that is money that would take them decades to save. Why would you give it away without doing some real thinking and planning to see if there are ways to save you at least some of it?

We are almost ready for Parts 2 and 3 of this short series where I’ll share approaches for carving substantial amounts of money out of what you would have paid your lender and putting it back in your pocket.

Again, please take a moment now to subscribe to receive emails when I publish new articles — such as Part 2 and Part 3 of this short series over the next few days.

Why doesn’t the mainstream corporate media focus on helping people minimize the interest they pay when buying a house?

One last thought here about why no one pushes you to think hard about the total dollar amount of interest you are committing to pay.

Seriously, nobody talks about this.

Think about every article and every interview you’ve ever seen on the topic of buying a house. The financial aspects of these articles and interviews alway start and stop with:

- Purchase price

- Whether housing prices are going up or going down.

- What the current interest rates are (…over the past several years, the focus has usually been on 30-year fixed-rate mortgages, although this may be about to change some.)

- What your monthly payment will be and how affordable it is or isn’t for the average person.

- And whether it makes more sense to buy or rent.

This recent article from CNBC by Michelle Fox is pretty typical of that. So is this other even more recent article from CNBC by Diana Olick.

It’s shallow writing. It barely qualifies as even being informative.

Even this article by BusinessInsider — “Home prices will start declining this year, senior economist says” — focuses only on high level economic indicators and metrics that really have nothing to do what would REALLY be helpful to working families trying to figure out how they can best afford to buy a house.

To the extent that media outlets like CNBC or BusinessInsider make you think that this is the info you need to make smart financial decisions for your family and you, they are doing you a disservice.

The whole situation reminds me of an old joke about Microsoft:

Lost Helicopter PilotA helicopter with a pilot and a single passenger was flying around above Seattle when a malfunction disabled all of the aircraft’s navigation and communications equipment. Due to the darkness and haze, the pilot could not determine the helicopter’s position and course to get back to the airport. The pilot saw a tall building with lights on and flew toward it, the pilot had the passenger draw a handwritten sign reading “WHERE AM I?” and hold it up for the building’s occupants to see. People in the building quickly responded to the aircraft, drew a large sign, and held it in a building window. Their sign said “YOU ARE IN A HELICOPTER.”The pilot smiled, waved, looked at his map, determined the course to steer to SEATAC airport, and landed safely.After they were on the ground, the passenger asked the pilot how the “YOU ARE IN A HELICOPTER” sign helped determine their position.The pilot responded “I knew that had to be the Microsoft support building, they gave me a technically correct but entirely useless answer.”

If you substitute “CNBC” or “Fox Business” or “Wall Street Journal” or “BusinessInsider” for Microsoft in the joke, then you’re half of the way toward updating the joke for the housing market in 2022.

Bottom line: you are not the media company’s customer.

You’re not the person paying the bills and the salaries at CNBC or for any of their mainstream corporate media competitors. Not for CNBC, nor for Fox Business, Wall Street Journal, NYT, Washington Post, MSNBC, CNN, etc.

That’s because:

- Corporate media news networks and newspapers generate revenues by selling advertising to corporations, many of whom are in the business of lending you money for a mortgage.

- You — the homebuyer — are NOT the person paying the bills for corporate media outlets. You are NOT the customer that these for-profit media companies serve.

- When it comes to content that cable news networks, etc. create about the consumer side of buying a house, the actual customers of the media companies are usually the financial services companies and mortgage lenders.

- So when corporate media networks slant their articles or they choose to cover — or not cover — certain topics, it’s likely going to be to the benefit of their advertisers…and to the detriment of you, the homebuyer.

Continuously ask yourself how these people and companies make money…and whether that makes their interests aligned with your interests…or run counter to your interests.

Do media companies — cable TV networks like MSNBC, Fox, CNN, CNBC and newspapers like NYT, WashPo, WSJ — generate ad revenues:

- by helping their advertisers extract MORE money out of you, even if you don’t benefit personally benefit from that additional “money extraction”…

- or by helping you make the best possible financial decisions for yourself even if it causes their advertisers to make less money off of you?

If I haven’t been clear up until now, I do have an opinion on which of the two options above is most often the case.

My mantra is “Objective, not neutral.”

Objectively — when you look at the facts on ground over a long period time and apply intelligence and common sense — it’s obvious that the people running these for-profit, corporate media companies act consciously and subconsciously in their own financial interests. Period. Full stop.

They behave this way even when you — the person consuming their “information” on TV or on the web on in a newspaper or magazine — get hurt financially (1) by the information they choose to cover and (2) by the information they choose not to cover.

It’s equally obvious when you look at how much money is at stake for the advertisers — the banks and mortgage lenders — that the people running those banks and mortgage lenders have a massive incentive to maximize the amount of interest money they “earn” from every single mortgage.

(I will discuss in detail in Parts 2 and 3 of this series how much money the banks and mortgage lenders and corporate media outlets are all grifting out of your pockets…and some very simple, relatively painless things you can do to slash the amount of money that they are taking from your wallets!)

Back to the banks and mortgage lenders for a moment.

I want to be clear about who you are dealing with when you get a mortgage.

When we look at how much documented history there is of senior-level and not-so-senior-level people at banks and financial institutions doing unethical and/or illegal things to maximize how much money they make — even when they are screwing over their own customers — I think it is foolish to take anything they tell you at face value.

Former Wells Fargo CEO John Stumpf is one great example of this, but as we know now through some great reporting by Matt Stoller, Wells Fargo was not the only banking industry screwing over their own customers…and it’s still going on today.

So if the banks are willing to screw you over directly (as Matt Stoller describes above), then we would all be foolish to think that management at these banks and mortgage lenders would not put pressure on CNBC, Wall Street Journal, et. al. to tell “news” stories in ways that benefit the banks even if consumers are hurt by it.

Be a skeptical consumer.

You have a lot of money riding on a decision like this.

Don’t make it easy for them to pull a three card monte scam on you and extract an extra couple hundred thousand dollars out of you…just because you let them.

Final reminder: please subscribe to receive emails when I publish new articles so that you don’t miss Part 2 or Part 3 of this short series over the next few days. That’s where the real insights and paradigm shifts are going to be.

Related

• 4 Lessons on When to Sell $400,000 Worth of Stock in an Unpredictable Market

• When Is a Stock Market Crash Not Really a Stock Market Crash?

• When Is a Bear Market Not Really a Bear Market?

• MBA Guide to Higher Mortgage Interest Rates, Part 2 — How Much Money Will You Save?

Recent

• The Deafening Silence on Stock Buybacks from Centrist Democrats

• 2 Reasons Populations Are Collapsing in Developed Countries

• 3 Key Facts Everyone Is Missing About Biden’s Student Loan Debt Relief

Potential to Change the Way You Think

• Why Are Fundamental Human Values Critically Important for Successful, Enduring Brands?

• Life Expectancy vs. Healthcare Costs in the U.S. (and Japan, Germany, France, Spain, Portugal, etc.)

• (1a/9) “Top-Down” Makes More Sense Than “Left-Right” in the U.S.

Want me to cover a topic? Please post suggestions in the comments, and I’ll use your input to help prioritize my writing and research.

If you appreciate my writing, please share it on social media.

Want unlimited access to all Medium articles? Become a member!

As always, thank you for reading, subscribing, clapping, and sharing — I appreciate you sharing your time and attention!