LEGAL REGULATION PROBLEMS OF CRYPTOCURRENCY DERIVATIVES

In the context of the transformation of the economy, attracting investments using traditional financial instruments is becoming more and more difficult — for most companies, the opportunity to attract financing through the use of classical instruments is limited or impossible (small and medium-sized businesses now have less access to bank lending, access to the exchange infrastructure, etc.) ). The main reasons are the tight regulation of the market, a large number of intermediaries, high costs of issuing and placing financial instruments. So, for example, to work with classic stock market instruments, the status of a qualified investor is required, it is necessary to comply with the regulatory requirements for the turnover of financial instruments, take into account the peculiarities of concluding transactions in the stock markets, take into account the peculiarities of the structure of transactions with foreign elements, etc. These problems can be seen in many international markets.

The transformation and “digitalization” of business leads to the need to “release” a new type of assets, and with the development of distributed ledger technology (blockchain technologies), as a solution to these problems, a new class of assets appears — crypto assets, as well as financial instruments — “cryptocurrency derivatives”, such like futures, contracts for difference (CFD), i.e. settlement futures transactions, options.

Cryptocurrency futures are standardized contracts that are traded on crypto exchanges with the intention of selling or buying an underlying asset (cryptocurrency) in the future for a specified price. Generally, futures are based on the spot (current) price and the difference between the current and future contracted price is the buyer’s profit or loss. A futures contract can be based on any asset, and it does not matter whether it is real or does not have any material characteristics but is simply a certain quantitative indicator, such as a percentage or an index.

Another example of a cryptocurrency derivative is the ZrCoin crypto token — a derivative financial instrument based on the real industrial production of synthetic zirconium dioxide, using “green” technologies. By purchasing ZrCoin tokens, investors finance the construction of a new production facility. Synth synthetic zirconium dioxide acts as a base active. Thus, the ZrCoin derivative is an option contract for the sale of zirconium dioxide in the form of an intangible asset ZrCoin, which includes an option (put option) to repurchase the zirconium dioxide at a specified time at an agreed price.

At the moment, it is known about several exchanges that have admitted to trading settlement derivative financial instruments, the underlying asset of which is bitcoin. For example, the Chicago Mercantile Exchange (CME) has allowed bitcoin-based futures to trade, the Cantor Exchange will offer bitcoin-based binary options to traders. A similar product is offered by the Cboe Futures Exchange (CFE).

At the same time, in many countries of the world, the turnover of cryptocurrency derivatives is not regulated by legislation, but the market demand for this is high. Due to public law and systemic risks, buying and selling altcoins for fiat money is highly risky, so the liquidity of altcoins is mainly provided by the possibility of withdrawing funds back to bitcoins. In this regard, as the altcoin market grows, the speculative bitcoin market will be transformed into a market for rights of claims and exchange obligations. Accordingly, regulation should be aimed at the legal regulation of the rights of claims, the object of which is cryptocurrency and tokens.

Bitcoin is currently the underlying asset providing value to alternative virtual currencies and derivative products. In this regard, it is a fair point of view that bitcoin is not a means of payment and exchange, but rather a measure of value. Given the use of smart contracts in this area, we note that a smart contract is not a new type of civil law contract, but in fact, a derivative, where the underlying asset is bitcoin, and the derivative part is determined by the market value of the token. So, the turnover of tokens is the turnover of financial derivatives.

In addition, some tokens with a high degree of probability can be recognized as derivatives if the price of tokens sold as part of the ICO is tied to financial products or is determined by market indicators at a certain time interval or events that should occur in the future.

In this regard, it is necessary to pay attention to the exchange regulation of the circulation of claims for a new class of assets and to revise the legal provisions on financial derivatives, as well as on corporate governance (within the framework of such quasi-corporate procedures, tokens appear), project financing and partnerships.

The development of the derivatives market was the result of active innovation in the financial market, which was associated with the expansion of investment of fictitious (financial) capital that does not function directly in the production process and is not loan capital. The immediate reason for the emergence of derivatives was the increased mobility of the rates of traditional securities, foreign currencies, and interest rates on borrowed funds. The emergence of derivatives was due to the need for economic entities to manage risks by creating mechanisms for hedging the risk of possible changes in prices for underlying exchange-traded assets and thus reducing their own financial risks.

In April 2004, the EU adopted the Markets in Financial Instruments Directive (MiFID, Directive 2004/39/EC) aimed at strengthening the legal framework for the regulation of investment services and financial markets and establishing fundamental principles for regulating the market for financial instruments, including general requirements for admission of derivatives to trading — the instrument must allow an adequate assessment of its value, and the derivatives agreement must contain an effective means of resolving disputes.

As a result of the 2008 global economic crisis, financial sector reforms were implemented, which tightened the requirements for transactions in the financial sector. In August 2012, Regulation 648/2012/EC of the European Parliament and of the Council came into force on OTC derivatives, central counterparties, and trade repositories.

In addition, the adoption of the new Directive 2014/65/EU of the European Parliament and of the Council on Markets in Financial Instruments (Directive 2014/65/EU) was a key stage in the reform.

One of the significant innovations was the requirement for the mandatory conclusion of a part of transactions with derivatives on regulated platforms, as well as the establishment of control by the competent authorities of the Member States, which have the right to impose administrative or criminal sanctions for violation of the relevant provisions of the Regulation or Directive, over the fulfillment of a trading obligation. Thus, a trading obligation was provided for transactions with derivatives, i.e. norms on the conclusion of contracts on one of the types of regulated sites (among such sites, regulated markets, multilateral and organized trading sites, as well as similar platforms registered in third countries were distinguished). In addition, information on all transactions in OTC derivatives carried out in Europe must be provided to trading depositories and will be made available to regulatory authorities, including the European Securities and Markets Authority (ESMA), in order to control derivatives turnover, and transactions in standard derivatives contracts must be made through an approved central counterparty.

In January 2018, the EU completed a major reform that brought into force two new, closely interrelated legal acts — the second Markets in Financial Instruments Directive (MiFID II) and the Markets Regulation financial instruments “(Markets in Financial Instruments Regulation — MiFIR). Western doctrine directly qualifies these legal acts as the “backbone of financial regulation”.

In accordance with Art. 2 of the Regulation on Markets in Financial Instruments “derivative financial instruments” means financial instruments as defined by Directive 2014/65 / EU, while the Directive uses a broad concept of a financial instrument, covering not only securities but also derivatives, as well as some other assets … According to the Markets in Financial Instruments Directive, the attributes of a derivative are:

- the corresponding type of contract (option, futures, swap, etc.);

- the presence of one of the underlying assets covered by MiFID II;

- settlement terms typical for financial derivatives (as a rule, financial derivatives are settlement ones, but under certain conditions, deliverable derivatives can be attributed to them).

Commodity financial derivatives can be deliverable, but they need to be traded in organized trading to qualify as financial instruments. At the same time, MiFID II and Delegated Regulation 2017/565 does not include services, currency, rights to real estate, intangible assets. Derivatives with these underlying assets are not financial and are not subject to MiFID II regulation. Accordingly, derivatives with underlying crypto-assets do not fall under the definition of financial instruments unless those crypto-assets themselves qualify as financial instruments.

Thus, products of online platforms selling digital currencies that are of interest to European regulators, such as binary options and contracts for differences (CFDs), are speculative contracts that do not have the main purpose of acquiring or disposing of cryptocurrencies, under which mutual requirements of the parties are determined by fluctuations in the exchange rate of the cryptocurrency, which is the underlying asset, where the main source is a cryptocurrency, and investors can bet on the result without owning the cryptocurrency itself, can be considered as derivative financial instruments.

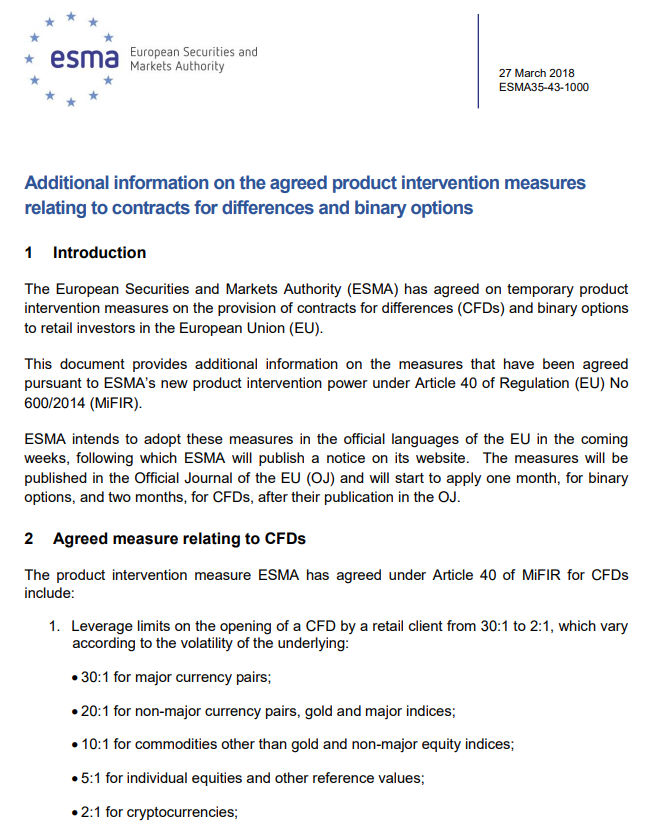

Due to the fact that cryptocurrencies as an underlying asset pose a particular danger to investors, since the market is in the process of formation, and the volatility of the exchange rate is too high, the European regulator, in order to protect the rights of investors, has established special requirements for the ratio of equity and borrowed funds when making transactions with cryptocurrency derivatives.

In France, the Autorite des marches financiers (AMF) is also committed to the position that financial products based on cryptocurrencies must be regulated as derivatives and that the circulation of cryptocurrency derivatives must comply with the European Union Markets in Financial Instruments Directive. Platforms offering such products must comply with authorization rules, as well as comply with requirements to prohibit advertising through electronic media. Despite the fact that cryptocurrency derivatives are not included in the MiFID list, the French regulator adheres to the position that “a cash settlement cryptocurrency contract can qualify as derivatives, regardless of the legal qualification of the cryptocurrency.” So, online exchanges offering cryptocurrency derivatives must comply with the MiFID directive and operate within the framework of the European Market Infrastructure Regulation (EMIR). In addition, such cryptocurrencies also fall under the jurisdiction of the French anti-corruption law.

The Financial Conduct Authority (FCA) of the United Kingdom considers the following cryptocurrency derivatives as falling under the definition of a financial instrument: futures, which are characterized as transactions with deferred execution, but at the price specified in the contract, and not current at the time of execution; contracts for difference (CFDs), i.e. settlement urgent transactions; options.

Crypto market participants are responsible for the lack of a license, so they must conduct an analysis of their activities for trading in derivatives. FCA points out that many trading platforms offer a special product — transactions with cryptocurrencies for difference (CFDs), which can become an object of circulation. FCA notes that transactions are structured in such a way that they can not only entail a complete loss of funds invested in cryptocurrency but also make the consumer a debtor to the company with which the CFD is concluded. In this regard, FCA indicates that trading in these instruments is subject to the requirements provided for by the legislation on the securities market, namely, entities offering CFDs must be licensed to conduct these activities. Consumers have the right to file a complaint with the Financial Ombudsman Service and are entitled to claim compensation under the Financial Services Compensation Scheme. In the case of trading in another jurisdiction, individual complaints should be directed to the services of the respective jurisdiction. In order to protect the rights of investors, the FCA has established requirements for persons offering cryptocurrency derivatives.

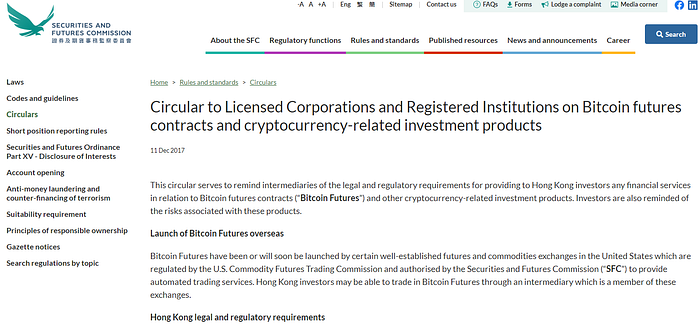

The Hong Kong regulator also acknowledged the possibility of trading bitcoin-based futures, pointing out that although the cryptocurrency is not a security and its circulation is not regulated by the rules on the securities market, futures of any kind are subject to securities market legislation (Securities and Futures Ordinance ). In this regard, this activity is subject to licensing. At the same time, the relevant requirements are of an extraterritorial nature — they apply to anyone who publicly offers such services to an indefinite number of persons in Hong Kong, in particular to cryptocurrency exchanges.

Thus, derivatives, the underlying asset of which is cryptocurrencies, can be qualified as financial instruments from the point of view of the European Union Markets in Financial Instruments Directive. As such, online exchanges offering cryptocurrency derivatives must comply with the MiFID directive and operate within the framework of the European Market Infrastructure Regulation (EMIR). Concluding transactions with derivatives, organizing their trading, consulting and other services may be recognized as activities in the securities market, and therefore may require a license.

Regulators are drawing investors’ attention to the high-risk nature of financial products such as binary options and contracts for difference (CFDs). Despite the fact that these instruments are a way of hedging risks associated with the high volatility of cryptocurrencies, as a rule, CFDs are offered on rather unfavorable terms. In this regard, regulators are taking measures to protect the rights of investors (requirements for securing contracts, experience with such instruments, and other requirements).

In the Russian science of business law, derivatives are considered in two aspects: in the narrow sense, derivatives are fixed-term contracts with special conditions for their conclusion and execution. In a broad sense, derivatives are any market instruments based on primary income assets, such as goods, money, property, securities. They are used to obtain the highest income at a given level of risk or to obtain a given income at a minimum risk, reduce taxation, and to achieve other similar goals put forward by market participants. In the latter case, the class of derivatives includes not only forward contracts but also any other new market instruments such as secondary securities in their potentially infinite variety, combinations of securities with forwarding contracts, etc.

Taking into account the presence of such high-risk instruments on the Russian markets, regardless of the legal status of the cryptocurrency, financial instruments using bitcoin, since such instruments fully comply with the characteristics of derivatives, should be considered as derivatives with special legislation applied to them, and measures must be protecting the rights of investors, including the establishment of requirements for the availability of financial guarantees for transactions with cryptocurrency derivatives. These measures will also increase the investment attractiveness, and hence the demand for the underlying asset and its price. This means that the global demand for bitcoin and market liquidity will increase significantly. Given the limited resource and the predictable emission of digital gold, these factors should significantly increase the price and at the same time reduce its volatility.

We believe that the conclusion of transactions with cryptocurrency derivatives, the organization of their trades, consulting, and other services should be recognized as activities in the securities market, and therefore subject to licensing. Given the actual position of cryptocurrency in international markets, if the Russian regulator recognizes it as an independent underlying asset for financial instruments, this will give an impetus for the development of structured financial instruments based on bitcoin. On the other hand, it should be taken into account that the use of derivatives for speculative purposes leads to the transformation of the derivatives market into a high-risk one. Thus, historical experience has shown that an additional factor of destabilization of the urgent, and ultimately the entire financial market is the use of high-risk instruments as a basic asset, which include cryptocurrency (bitcoin).

However, derivatives are used not only for speculative purposes. It should be noted that the most important function of the derivatives market is the function of informing all participants in economic relations about prices in the market. As R. Kolb notes, the conclusion of transactions in financial derivatives leads to the establishment of prices that can be monitored and valued by the entire society, and this provides information to market observers about the real value of certain assets, as well as the direction of future economic development.

In this regard, given the emergence of new instruments, financial markets require expertise aimed at minimizing risks, which, first of all, should create incentives for the introduction and development of innovative institutions, as well as guarantee the protection of the rights of consumers and private investors.

{kind=link}