High Hopes

Stock Price Performance in the 1st Year of a Corporate Venture Capital Program

Data from Insead shows that corporate venture capital (“CVC”) programs operate, on average, for only four years. With this short lifespan, it makes sense that corporate executives might experience trepidation when considering launching a venture capital effort. In addition to the capital, time, and other resources required to start an investment program, public company executives may also be concerned about the impact a venture capital program might have on the corporation’s stock price. Though venture capital investments rarely generate returns within the first year, we conducted research showing that the median corporation in our data set outperformed its listing index by 25% in the first year of its CVC program.*

Background

In May of 2017, we examined how stock prices of corporations with venture capital programs performed based on their vintage (the year they launched their venture capital units). In that analysis, we found that the stocks prices of public U.S. corporations with the youngest venture capital programs outperformed their indices by 95.9%, on average.

In the study mentioned above, we analyzed the 60 public U.S. based corporations on the Global Corporate Venturing (“GCV”) 2016 top 100 most active U.S. CVC list. The CVC units analyzed were between 1 and 30 years old, with about a third of them in existence for 5 or fewer years. These corporations compete in a variety of industries, including high technology (Intel), software (Google), energy (Chevron), financial services (Visa), waste disposal (Waste Management), and retail (Best Buy). The methodology for compiling the data is described in the first study in this series.

We sorted the corporations into three-year “bands” by the age of the venture capital program, and analyzed the median stock price change since the program’s inception to see whether stock price performance was correlated with the age of the program, and we were surprised to see the corporations with the youngest venture capital programs performed the best. There are twelve corporations in our data set whose venture capital programs are less than three years old and fell into “Band A”. As of December 31, 2016, the median compound annual growth rate of these companies’ share prices since the inception of their programs was 10.5% compared to the median exchange growth rate of 5.3% during the same period. This 5.1% gross improvement represents an outperformance of 95.9% versus the index. On average, these twelve companies’ stocks had the largest outperformance of the 60 we analyzed.

This data about the twelve corporations in “Band A” provided a signal that corporations’ stock prices may benefit from the launch of a CVC program in the first few years. To study this further, we expanded the data set to identify whether the performance of the “Band A” companies relative to their listing indices was attributable to market conditions between 2013 and 2015 rather than the launch of the CVC effort. In other words, was the effect we observed specific to the economic cycle of 2013–2015, or a potentially inherent benefit of launching a venture capital arm?

Analysis of the First Year of a Program

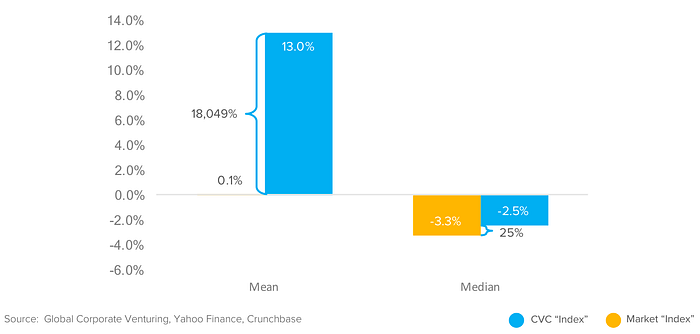

To explore whether market timing explains the performance of the “Band A” funds in our analysis, we analyzed performance in the first year of the venture program of all 60 public companies on the same GCV Top 100 U.S. CVC list. We noted each corporation’s stock price and listing index level at launch and one year after the program’s launch (from Yahoo! Finance) to find the stock and index performance. 34 of the 60 companies outperformed their indices with no detectable pattern in listing index, year of program formation, or industries. On average, the compound annual growth rate was 13.0% in the first year of a CVC unit, compared to 0.1% for the market indices. This represents a 18,049% outperformance. Because outliers skew these results, we identified the median corporation. Medtronic is the median company and had -2.5% stock price depreciation in 2000, the first year of its CVC program. Compared to the NYSE’s -3.3% return over the same period, Medtronic outperformed its listing index by 25%.

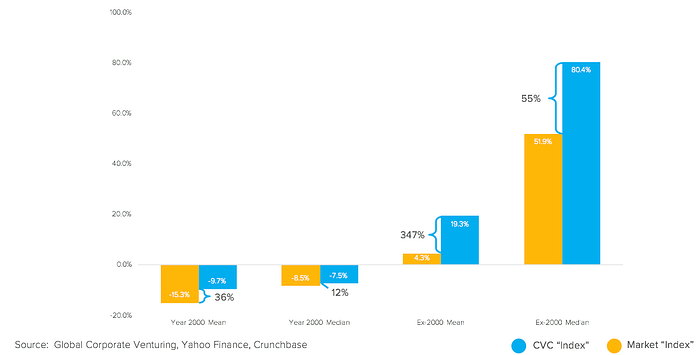

The mean index performance in our sample was impacted by the negative index performance in 2000, the year thirteen of the corporations in the study launched their corporate venture capital efforts. The “dot-com crash” in 2000 may have caused fundamentally different stock market behavior during that period. Therefore, we also decided to look at the 2000 vintage CVC parent companies separately from the other corporations to determine how those market conditions may have affected our results. On average, corporations that announced their CVC efforts in 2000 had a compound annual share price growth rate of -9.7% in the first year of their programs, compared to -15.3% for the market indices. This represents a 36% outperformance. The median corporation in this group was Coca-Cola, which had a compound annual share price growth rate of -7.5% in its first year, compared to -8.5% for the NYSE over the same period. Coca-Cola outperformed the NYSE by 11% in that year. The data from the 2000 vintage show that though absolute share price changes were negative over the course of that year, stocks of corporations with CVC programs still outperformed their indices during the first year of the effort.

For the 47 corporations that launched their venture capital programs from 1986 to 1999 and 2001 to 2015, the average and median firms also outperformed their indices over the relevant period. On average, corporations that announced their CVC efforts in these years had a compound annual share price growth rate of 19.3% in the first year of their programs, compared to 4.3% for the market indices. This represents a 347% outperformance. The median corporation in this group was Applied Materials, which had a compound annual share price growth rate of 80.4% in its first year, compared to 51.9% for the NASDAQ Composite Index over the same period. Applied Materials outperformed the NASDAQ Composite Index by 55% in 2003, the year the company announced its venture capital effort.

Commercial relationships with startups usually require more than a year to impact a corporation’s financial performance, and financial returns from venture capital investments typically cluster at six years or more (and the median institutional venture capital fund takes 14 years to liquidate). So why would a corporation’s stock benefit so quickly after announcing an effort when it might take over a decade to see how the portfolio turns out? We hypothesize that all else being equal, public market analysts may interpret a CVC program launch as a visible demonstration of the long-term orientation of the management team. Possible financial benefits from a venture capital effort are unlikely to show up in the company’s quarterly or annual results in the first year, but a management team that launches a VC effort is probably interested in learning about trends and preparing for the future, which could positively impact financial results in the future.

The outperformance of the stocks of corporations in the first year of a venture capital programs does not indicate a causal relationship between the program launch and stock performance. Many other factors could account for these results. These corporations may be successful already, and through good results in their core businesses, have generated the resources to start a corporate venture unit. Product launches, management changes, or other events unrelated to the investment program also could lead to superior stock performance. Also, only 34 of the 60 companies studied outperformed their respective indices. However, we believe this data requires ongoing study to quantify the potential public relations benefits that may accrue to corporations launching corporate venture capital programs.

*For each company in the data, we calculated the compound annual growth rate of the stock between the date of announcement of the CVC effort and the date one year later. We used the same methodology for the NYSE and NASDAQ for each pair of dates.

Liked what you read? Click 👏 to help others find this article.

Selina Troesch (selina@touchdownvc.com) is a Senior Associate at Touchdown Ventures, a Registered Investment Adviser that provides “Venture Capital as a Service” to help leading corporations launch and manage their investment programs. Touchdown’s President Scott Lenet contributed to this article.

This article includes information from third party sources believed to be reliable; however, we make no representations as to its accuracy or completeness. References to strategies are for illustrative purposes only and should not be relied upon as a recommendation to engage in any particular strategy or to invest in any particular security. Opinions expressed herein are based on current market conditions and may change without notice and we reserve the right to change any part of these materials without notice and assume no obligation to provide an update. Recipients are advised not to infer or assume that any securities, strategies, companies, sectors or markets described will be profitable or that losses will not occur. Any description or information regarding investment process or strategies is provided for illustrative purposes only, may not be fully indicative of any present or future investments and may be changed at the discretion of Touchdown. Past performance is no guarantee of future results.

The NYSE Composite Index is a float-adjusted market-capitalization weighted index which includes all common stocks listed on the NYSE, including ADRs, REITs and tracking stocks and listings of foreign companies. The NASDAQ Composite Index is a broad-based capitalization-weighted index of stocks in all three NASDAQ tiers: Global Select, Global Market and Capital Market. All indices used in this article are provided for informational purposes only and are provided for the purpose of making general market data available as a point of reference only. The performance and characteristics of an index used in this report is not an exact representation of any particular investment, as you cannot invest directly in any such index.