Will the Fed Pivot? The FOMC vs Data

Last weeks the markets lived with a hope of the ‘Fed Pivot’ once again, while the Fed officials were unable to provide any indication due to the standard FOMC media blackout.

Banks, analysts, and media jumped in to fill the void:

Morgan Stanley’s strategist, Michael Wilson, suggested the end of the interest raises was approaching, due to the yield curve inversion between 10-year and three-month Treasuries, a reliable recession indicator, which according o Wilson supported “a Fed pivot sooner rather than later.”

Meanwhile, Blackrock anticipated a “pivot language” at the FOMC meeting in November. That and ambiguous Tweets and WSJ articles by Nick Timiraos, called by some analysts “Nicky Leaks” or the unofficial Fed spokesman during the FOMC blackouts, were enough to send the markets into mini rallies ahead of the Federal Open Market Committee deliberations.

A yield inversion of the 10-year and 2-year Treasury bonds, another recession indicator, already happened in July 2022, reaching the worst numbers since 2000. And many central banks and economists, including the IMF, warned of a global recession and quickly cooling economies, which the markets think might force the Fed to pivot and restart QE earlier than it anticipated.

The November FOMC Meeting

On Nov 2, 2022, the FOMC made the 4th consecutive 0.75% rise, and the 6th rise in total, bringing the federal funds rate to a target range of 3.75% to 4%. A 75 bps hike was well communicated by the Fed weeks leading to the FOMC, with no striking inflation or labor data moves that could warrant a looser monetary policy.

But the real question became, what’s next for the Fed’s tightening and how long can the Central Bank keep it up without “breaking something” or triggering a financial crisis?

‘Dovish’ FOMC Statements

As the market participants dissected the FOMC press release and Jerome’s Powell speech and a media Q&A, multiple new narratives emerged. It was clear that the audience was desperately looking for any signs of dovishness or a pause. And it seemed they got it, although not in the form that they hoped for.

- “At some point, as I’ve said in the last two press conferences, it will become promote to slow the pace of increases to bring inflation down to our 2% goal.” — The Fed will consider a slower pace of rate hikes, probably as soon as the next meeting in December 2022.

- “ Our decisions will depend on the totality of incoming data and implications for the outlook of activity and inflation. We will continue to make our decisions meeting by meeting (…)” — The Fed will continue to assess hikes on a meeting-by-meeting basis and analyze a wide range of current data. The data releases will remain important to gauge the Fed’s next moves.

- “We will take into account the cumulative tightening of monetary policy and the lags with which monetary policy affects economic activity and inflation.” — The Fed will now also take into consideration wider economic metrics for the signs of cooling. It also admitted that some metrics are lagging indicators.

Ahead of the FOMC, many analysts, including Harvard Economics Professor Jason Furman and Economist Paul Krugman, pointed to the lagging indicators used by the BLS and BEA to calculate inflation and the rapid cooling of the commercial rent and car indexes.

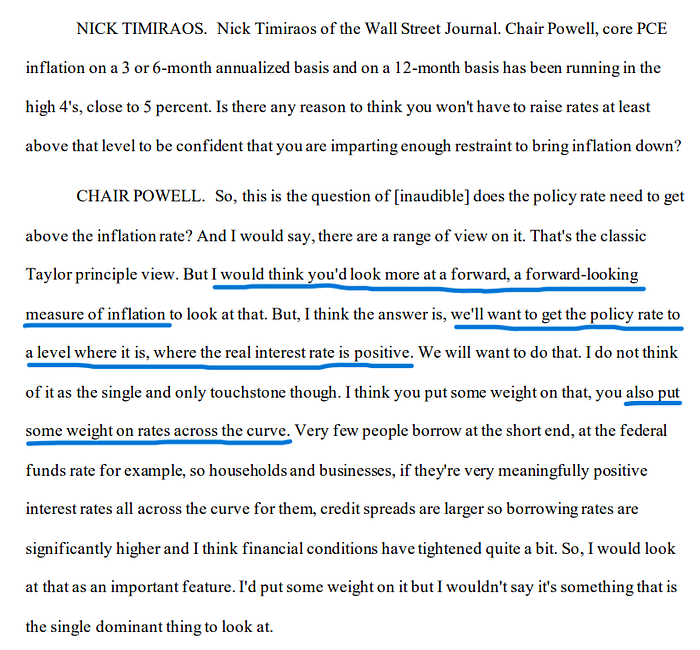

“Financial conditions have tightened significantly in response to our policy actions. We are seeing the effects on demand in the most interest rate sensitive sectors of the economy, such as housing. It will take time for it to be realized, especially on inflation.” Jerome Powell said, in one of many responses to suggestions, that the Fed might be overtightening and using delayed metrics.

Hawkish FOMC Statements

- The Fed will continue “the process of significantly reducing the size of our balance sheet, which plays an important role in firming the stance of monetary policy.”

- “Incoming data since our last meeting suggests that the ultimate level of interest rates will be higher than previously expected” — The final range of interest rate hikes will likely be higher than the 4.4–4.9% predicted at the September FOMC.

- “The historical record cautions strongly from loosening policy. We will stay the course until the job is done.” — Loosening the monetary policy too soon resulted in inflation coming back and staying for longer, historically. The Fed will err on the side of overtightening rather than pivoting too soon.

Conspicuous Omissions

- Jerome Powell did not reiterate that the hikes would stay “higher for longer”, but rather that they will likely reach a higher range. He avoided the answer on how long the hikes might stay up.

The Fed’s Favorite Metrics

This time the Fed promised it would look not only at inflation and the labor market but also at other unspecified metrics that could signal a cooling economy.

Inflation

As announced on Nov 10, the October CPI was 7.7%, down from 8.2% in September. The Core CPI was 6.3%, down from 6.6%. The MoM CPI was 0.4%, the same as in September. The Core MoM CPI was 0.3%, down from 0.6%. — The CPI is still relatively high and likely won’t sway the Fed to change its course.

The PCE for October will be announced on Dec 1, 2022. The PCE for September was 6.2%, the same as in August. The Core PCE was 5.1% in September, up from 4.9%. — Even if the PCE decreases similarly to the CPI in October, the Fed will likely wait for more releases before it pauses hikes.

Labor Market

Wages: “Real average hourly earnings for all employees decreased 0.1 percent from September to October. Real average weekly earnings decreased 0.1 percent. Real average hourly earnings decreased 2.8 percent, seasonally adjusted, from October 2021 to October 2022. The change in real average hourly earnings combined with a decrease of 0.9 percent in the average workweek resulted in a 3.7-percent decrease in real average weekly earnings over this period.” — Wages decreasing is a good news for the Fed. It blames higher wages for some of the persistent core inflation.

Job openings and hires: “On the last business day of September, the number of job openings increased to 10.7 million (+437,000).(…) In September, the number of hires edged down to 6.1 million and the rate changed little at 4.0 percent.” — More job openings enables the Fed to hike higher for longer to “soften the labor market.”

Jobs and Unemployment: “Total nonfarm payroll employment increased by 261,000 in October, The unemployment rate increased by 0.2 percentage point to 3.7 percent in October, and the number of unemployed persons rose by 306,000 to 6.1 million. The unemployment rate has been in a narrow range of 3.5 percent to 3.7 percent since March.” — Low unemployment leaves the Fed with plenty of space to hike the interest rates.

Forward-looking inflation metrics:

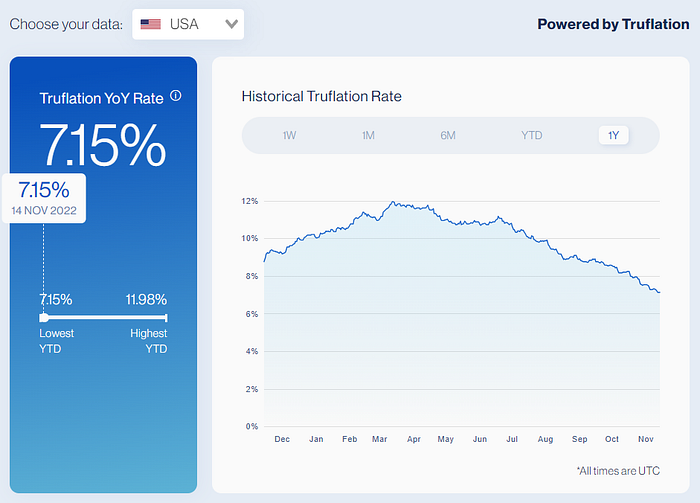

What Does Truflation Data say:

In our opinion, the Fed’s tightening is working well, and they may be at risk of over-tightening into a recession. According to our independent data, the YoY inflation rate in the US has dropped from 12% in March to 8.5% at the end of September and 7.5% at the end of October. As of Nov 14, 2022, Truflation rate was 7.15%.

Free daily inflation updates are available on our dashboard, including one year of historical data and price indexes of the categories contributing to our Consumer Price Index.

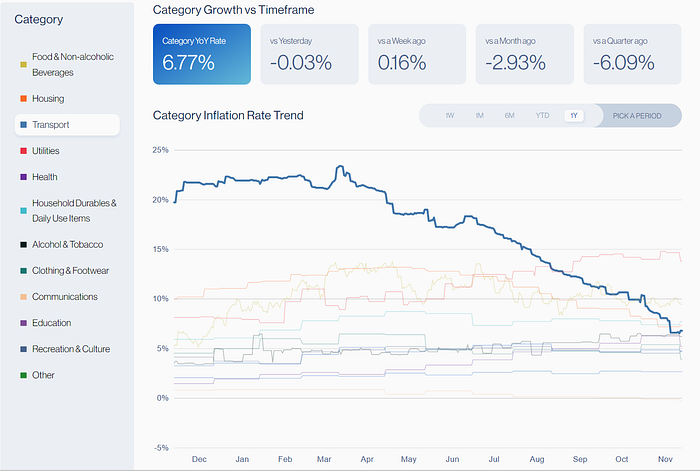

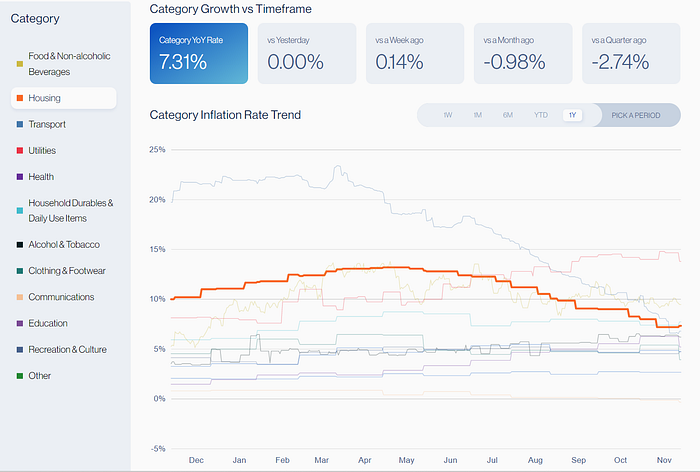

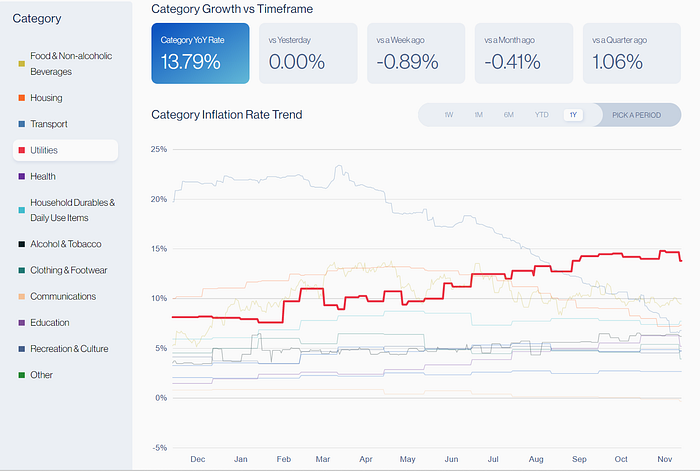

The main Truflation categories contributing to our index changes within the last 30 days were (as of Nov 13, 2022):

Transportation decreased by 2.9% vs a month ago, not only due to gasoline prices but mainly the used car indexes going down.

The Truflation Housing index, which includes rented and owned dwellings costs changes decreased by 1% vs a month ago.

Utilities declined by 0.9% vs a month ago

According to our data, Food and Non-alcoholic Beverages prices also slowed their pace of increases by 0.8%.

Clothing and footwear category decreased by 0.7% within the last 30 days (as of Nov 13, 2022)

Truflation also ran two internal forecasting models using our data, which predicted the BLS CPI to be 7.8–7.9%, as reported in our data insights, and 7.6%, according to another unshared model. The final CPI landed at 7.7%. Both our forecasts turned out to be more accurate than the market, banks, and the Cleveland Fed’s predictions.

Our models are not publicly or commercially available right now, but they are a strong indicator that the data, which are available via Chainlink oracles and custom subscriptions, could be used for predictions. Contact us for more information.

Summary

Despite the rapid cooling in the markets and seemingly decreasing inflation (October CPI), we think the Fed will continue tightening into minimum 50 bps.

The 7.7% YoY CPI inflation remains high, with lower but still positive monthly inflation levels of 0.4% for CPI and 0.3% for core CPI.

As communicated, the Fed is now asking three questions: how fast, how high, and how long, and the matter of speed is becoming less relevant, with lower rates potentially coming next month already. Despite that, the terminal interest rates will likely be higher than the predicted 4.9% and might be kept high until the Fed sees inflation and inflation expectations dropping substantially towards the 2% target.

We don’t quite know if the Fed can afford to wait for the core or headline CPI to hit 2% or if it will use some forward-looking metrics to gauge when the “underlying inflation” reaches below the interest rate hikes to obtain the positive real interest rates. The Fed might also look at the effective rates of mortgages and loans in the market to inform its decisions. Current mortgage rates in the US have reached 7.3% (as of Nov 13, 2022).

What we do know, is that the Fed can’t afford to stop hiking and will risk overtightening rather than the return of inflation, as mentioned by Jerome Powell. The central bank is prepared not to pivot in response to prolonged periods of slow growth (low or negative GDP) and the softening labor market (slower job growth, higher unemployment, etc.). It’s unlikely it will change course unless we see a significant economic crash or a dramatic disinflation or deflation.

That being said, the starved markets are ready to rally on any positive news and consider the next 50 bps hike a “Fed Pivot” as the term seems to take on alternative meanings.

(3) Magoo PhD on Twitter: “Fed Pivot Inbound. https://t.co/2BzblLEnoN" / Twitter

Written by Natalia Nowakowska

About Truflation

Truflation is an economic data aggregator serving independent, unbiased, real-time data on-chain and off-chain. Truflation’s goal is to help individuals, investors, companies, and institutions make more informed decisions by accessing independent and unbiased economic information.

Originally published at https://www.linkedin.com.