Consumer: Past, Present and Future

The Case for Investing in arfa by Christophe Bourque, Karolina Mrozkova and Max Johnson

TL;DR

● D2C brands have started to disrupt CPG conglomerates

● Limitations of scaling a D2C brand are becoming apparent

● D2C model is evolving to multi-brand platforms with innovative customer engagement

● arfa is the future of scalable D2C for Consumer Packaged Goods

● We invested in arfa

We at White Star Capital have been fascinated with the consumer-sector for years. Since investing in Dollar Shave Club’s Seed round in 2012, we have gone on to add companies from spending rewards app Drop, to ready-to-eat meal delivery Freshly, micro-mobility operator Tier Mobility and consumer health and wellness provider Parsley Health to our portfolio. Today, we’re only more optimistic about the future of the consumer sector — particularly in personal care.

Over the next decade, the world will gain the equivalent of 80+ Procter & Gambles in new enterprise value — this is the magnitude of growth anticipated in the consumer-packaged-goods (CPG) sector, which is expected to reach $14 trillion by 2025[1]. Additionally, the personal care and beauty market is expected to grow at a 7.2% CAGR over the next 4 years, over 4x the growth in US consumption.

However, established personal CPG brands are struggling to keep up with the modern consumer — the world’s largest personal care CPG conglomerates (Johnson & Johnson, L’Oréal, Henkel, etc.) were created 100+ years ago and are starting to get disrupted by the Direct-to-Consumer (D2C) model. Through social media, community-building, content creation, values-driven design and branding, and other sales mechanisms to push products directly to consumers when and how they want them, D2C companies are reshaping the consumer sector landscape.

The Rise of D2C

Nimble start-ups such as Dollar Shave Club, Glossier and Away have tapped into the needs and wants of consumers and created brands valued at over $1Bn. Plainly, Procter & Gamble’s brands and business practices were created to suit the lifestyles and mindsets of the Baby Boomer generation — however, a consumer generation with radically different values is quickly entering its earning prime: Millennials (with Gen Zers soon to follow).

Millennials, more than any prior generation, are driven to consume based on social value alignment — by seeing their own sense of ethics and social progressiveness reflected in the products they use or the clothing they wear. This means that today’s most successful consumer brands are those best tying themselves to trending social causes, as in the case of omnichannel clothing retailer, Everlane and the Honest Company.

Furthermore, an increasing emphasis on lifestyle as one’s source of value has made wellness and personal care an important focus for Millennial consumers. Brands advertising “aspirational lifestyles” via social media have built big businesses on everything from organic skincare to plant-based beverages (estimated to reach $48B and $20B markets, respectively, in the next five years[2]). See below how completely a modern consumer may integrate health and wellness into her daily lifestyle:

Driven by the demands of American Millennials, incumbent brands stand to increasingly lose market share year over year: 40% of US internet users expect D2C brands to account for 40% or more of their purchases within the next five years[3]. Additionally, D2C brands have already captured significant market share across categories — 20% in mattresses, 15% in shoes, and 12% in razors, for example[4].

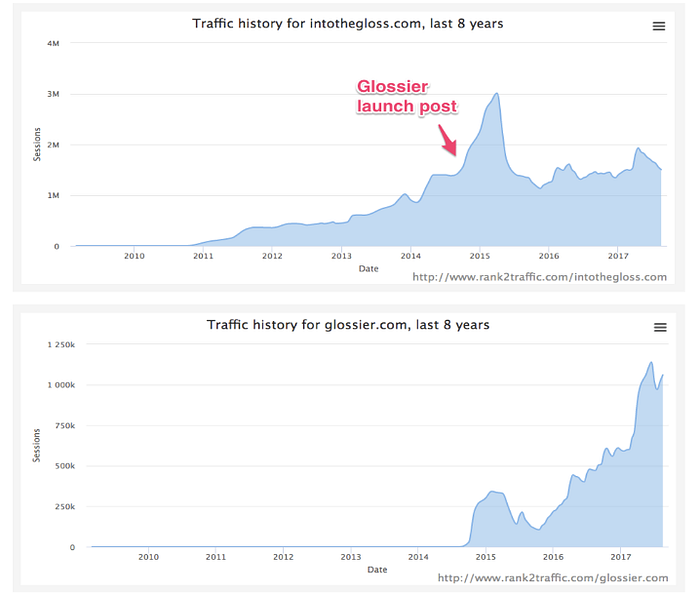

One of D2C’s greatest success stories, Glossier, demonstrates the power of consumer engagement, and the value of the data it provides. Glossier’s CEO Emily Weiss, prior to founding the company, launched a makeup blog called “Into the Gloss”, which grew quickly to a readership of over 1.5m followers. Eventually, Weiss took the leap into product by launching Glossier — “A total evolution of the same mission, but with tactile content,” in her own words[5]. Practicably, her mass-followed blog became a powerful top-of-funnel sales mechanism for her D2C cosmetics products — traffic on the Glossier product site would leap in response to new “Into the Gloss” content:

Yet, blog-conversion alone did not enable Glossier to blitz scale — product research informed by extensive, up-to-date data analysis on customers (via intimate customer engagement methods) was crucial to creating highly successful products. For example, after analyzing 400+ blog comments (customer creative input), the Glossier team came to a product formulation they thought would be a hit with their customer base, and one that was in a large part invented by the very customers they would sell it to. In short, community building and customer co-creation in this manner then propelled their product lines into growing 600% YoY in revenues[6]. By leveraging methods like these and other new practices, D2C products challenge traditional CPG and serve consumers better.

However, as many well known D2C companies mature, we are witnessing the onset of major barriers to growth.

Current D2C Limitations

Many D2Cs launched and grew exponentially under favorable market conditions that lowered barriers to entry, such as ample access to capital, arbitrage opportunities within digital and social media advertising, and flexible supply chain. The result was the rise of the long tail, where instead of relying on third-party sales channels to achieve scale, D2C brands used the spread achieved by bypassing traditional retail models to invest in driving audiences to their e-commerce sites.

However, many D2C brands, especially those with high VC investment, also rely heavily on direct channels, are mono-brands, focused almost exclusively on Millenials, and have very limited opportunities to drive cost efficiency or vertically integrate — growing becomes difficult and expensive once your core “hero product” has reached peak efficiency.

The most high-profile case study of these effects is the D2C mattress company, Casper. Aided by $422 million in marketing spend in the past four years alone, the company showed in its IPO prospectus survey that 31% of the U.S. population is aware of its brand; however, Casper has yet to turn a profit despite growing revenues. A swarm of new entrants into the sleep market, namely Purple Innovation Inc. and Leesa Sleep LLC, have made the online-advertising market more competitive and costly. As Sam Bernards, former CEO of Purple, attests, the D2C sleep companies are “all competing for the same keywords on Google, and the same on Facebook … [it’s] just economics 101. The more competition, the higher the spending.”

With ad costs rising, the marketplace flooding, and growth plateauing, only the D2C brands with sustainable operating models and favorable underlying unit economics — namely Customer Acquisition Cost (CAC) and Lifetime Value (LTV) — will survive. This pressure is resulting in fundamental evolutions around how D2C companies are structured and how they engage with their consumers.

D2C Evolution

We believe that pressure on the very concept of D2C brands is leading to two fundamental transformations:

● Creating D2C Bundled-Platforms

New business models will evolve toward D2C brand-bundling to regain leverage, in the form of new holding companies, or brand-led consortiums, that help drive long-term efficiency. This notion has begun, in its early stages, to show proof of concept in companies like Mavely, a new multi-brand D2C retail platform, which asserts that its brands have been able to acquire customers for 30–50% less than Instagram via its own intra-community cross-selling and promotion[7]. This acquisition cost reduction will be crucially important for the next wave of D2C companies, as advertising on Instagram, Facebook, Google and other digital platforms becomes increasingly more expensive and undifferentiated.

● Innovating Customer Engagement

D2C brands have learned to use go-to-market tactics like brand advocate programs, second-party data co-ops, and product launch waitlists to gain new types of data on consumers and “build humanity” online. But digital alone isn’t enough — millennials feel digital marketing is increasingly anonymous and desire a relationship that extends more intimately into their physical lives as well. Going forward, successful D2C companies will need to reimagine physicality, using the intimate behavioral and psychographic data they have on individual consumers to build differentiated, lifestyle-driven offline experiences and consumer touch points like community-powered digital and print magazines and blogs, highly personalized mobile concierges, and real-life events.

It is precisely this set of trends that makes us so excited to announce our investment in arfa, the future of brands in our everyday lives.

Introducing arfa: Why We’re Excited

With a team of experts in branding, community, and marketing, arfa is creating a platform for the creation of new CPG brands and products that they will make in collaboration with the very customers they seek to serve. The unique and scalable customer engagement model will allow them to build multiple relevant brands, reaching into demographic and psychographic groups beyond the Millennial confines that most of D2C have found itself in up until now.

So far, the company has already demonstrated its ability to develop brands quickly — arfa currently has several categories productized, which we had the chance to test at White Star Capital’s office in New York. We are looking forward to seeing them launched and the reception from customers very soon.

More than anything, we have the utmost faith in arfa’s incredible management team. arfa’s founder and CEO, Henry Davis, was previously a part of the pre-launch team at Glossier, as President & COO. Henry was instrumental in growing the business to well over $100m in revenue and raising nearly $300m in VC funding at a valuation that now exceeds $1.2bn. arfa’s CTO, Bryan Mahoney, was Glossier’s CTO and co-founded Dynamo, a digital studio that built the back and front end of many successful brands, including Flatiron Health (acquired for $1.9bn by Roche), Blue Bottle (valued at $800m+), and Lola (raised $35m+ to-date). arfa was also co-founded by Ariel Wengroff, the company’s Chief Content Officer and former executive at Vice Media and publisher of Broadly, Vice’s site dedicated to covering gender and identity, as well as Shabdha Chigurupati, the company’s VP Business Development and Finance and former Chief of Staff at Glossier. Moreover, the founders have attracted some of the industry’s top professionals such as Marie Audier (former Head of Marketing at Coach) as Chief Customer Officer, Jose Larios (former Head of Supply Chain at Henkel) to lead operations, and Sophia Aledenoye (ex-Unilever and L’Oreal) to head growth marketing. This team is arguably one of the top founding teams in the D2C space globally.

In summary, we are very excited to be participating in the evolution of CPG by co-leading the investment in arfa with Index Ventures, and investing alongside Forerunner, Thrive Capital and Northzone.

About White Star Capital

White Star Capital is a global multi-stage technology investment platform that invests in exceptional entrepreneurs building ambitious, international businesses. Operating out of New York, London, Paris, Montreal, Tokyo, and Hong Kong, our presence, perspective, and people enable us to partner closely with our Founders to help them scale internationally from Series A onwards.

Find out more about how we venture beyond at www.whitestarcapital.com or follow us on LinkedIn, Twitter or Facebook.