Spotify and Ek’s Parlay (Part I)

At a crossroads where platform meets proprietary ambitions

Recode recently reported that two of the three major record labels had started selling their equity stakes in Spotify:

“Last week, Sony, the music label with the biggest stake in Spotify, announced that it had sold about half of its shares, for about $750 million…

“Today, Warner Music Group says it has sold 75 percent of its Spotify shares, for about $400 million…

“Warner, along with Sony and Universal Music Group, captures the bulk of the revenue Spotify generates…”

How else can you read this but to infer that the major labels feel pretty secure about their leverage over Spotify come time for royalty rate renegotiations?

The major labels’ equity stakes in Spotify (~14% combine before these liquidations) were definitely both an investment and a hedge. However, I never viewed their interests as solely bargaining chips with respect to royalty rates; I also saw them as mutually assured destruction that structurally prohibited Spotify from launching its own label. Regarding the latter, it strikes me as a strategic error for incumbents to divest — almost welcoming the opportunity for Spotify to experiment with its own label akin to Netflix producing its own original content.

We’ve been here before, as I last discussed the idea of an upstart record-label-cum-VC in “SoundCloud Could Have Been the AngelList of Music”. Crucially, Spotify should not necessarily be signing proven talent that it has to poach from its suppliers, the labels. The channel conflict there is too brazen. Instead of such inorganic cross-selling, Spotify could fund organic, up-and-coming talent.

While far less defiant, that strategy would require a deft touch nonetheless. Netflix was able to thread-this-needle in the streaming video industry, wherein cutthroat movie and TV enforcers are as infamous as the music industry’s.¹

Back when I first proposed this “AngelList of music” approach, the most common refrains were as follows:

- ‘The labels will crush Spotify if it tries to compete with them’;

- ‘Spotify’s equity in artists doesn’t benefit Spotify as a distributor if they don’t have exclusivity’;

- ‘The Netflix playbook won’t work for Spotify because music listeners don’t subscribe to multiple services’;

- ‘The Netflix playbook won’t work for Spotify because music listeners want the entire back-catalog’

I’ll address each of those items now, including a pretty thorough analysis of Spotify’s competitive dynamics — yesterday, today, and hereafter…

#1: The labels would crush Spotify

Since collusion is illegal, the major labels cannot band-together to crush Spotify. Absent collusion, record labels face a bit of a prisoner’s dilemma in dealing with streaming services. More on that later, but for now, let’s just say that a single label, acting unilaterally, can not mortally wound Spotify. It’s conventional wisdom that Spotify would lose its users were it to lose a major label’s catalog, but that’s theoretically and empirically unfounded.

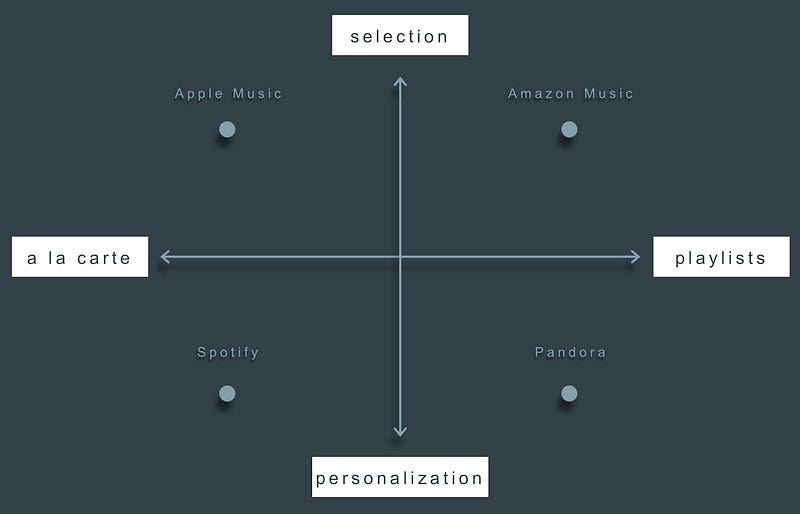

First, to understand the theoretical part, you have to evaluate consumer preferences:

- Either people want to listen to songs a la carte,

or people want to outsource their music selection to curated playlists; - Either listeners are free agents seeking the biggest selection of tracks,

or listeners are locked-in to platforms due to accumulated usage data that differentiates their experience through personalization

Were a label to remove all of its content from Spotify, it would have the most severe impact upon the app’s business if listeners purely preferred both the a la carte and selection options (as opposed to playlists and personalization). Of course, in reality, the consumer basket is neither that homogenized nor polarized. Not only do we all have different preferences from one another, but most of us aren’t strictly set in our ways — sometimes we press pause on our playlists to listen to that hot new single (and vice versa).

Given the infinite shades of grey among consumers’ preferences, the only economical way for major streaming apps to stake-their-claims was to cater to broad market segments in each of four, distinct quadrants:

While there are a few other platforms whom you can arguably add to that graphic — like Google Play Music, YouTube Music, and Tidal — this framework fits somewhat² neatly with what I discussed in “The Four Winds of Modern Media”:

“If you’ve already won with either huge scale or niche focus, you can then try to creep down or up in scale to grow… But, you cannot start in the middle of [any] spectrum and grow out, because your competitive disadvantages let your rivals squash you from the outside-in.”

In fact, you can argue that upon its launch Apple Music seized the void left by Amazon and Google in the a la carte wing of the selection hemisphere. One of Apple’s competitive advantages was — and remains — its users’ preexisting libraries, which have been trapped in the Apple ecosystem for more than a decade. Over as much as 15 years, listeners had accumulated albums and tracks by purchasing them via Apple’s legacy iTunes business, and now those “sunk costs” are an incredibly persuasive hook to rein-in consumers whose preference is to manually curate their music diets.

Similarly, Spotify was able to enter the game by filling the corresponding a la carte void opposite Pandora in that personalization hemisphere. Listening to discrete singles on Pandora involved a lot of friction — so much so that it almost felt like a feature, rather than a bug, given their niche as “The Music Genome Project”. Whereas Pandora’s fully-automated recommendation engine was only conducive to wholesale, serial consumption, Spotify’s answer unbundled the listening experience by making the song a more modular component again.³

So, if you lob “the labels could crush Spotify” at me, then this is my longwinded way of volleying “no they cannot” back at you. Succinctly, the labels cannot crush Spotify because the selection that record labels control is not a central component of the app’s value proposition.

That said, consumer demand isn’t binary or linear; it’s nuanced and convex. In other words, if X is the entire catalog of songs on a platform, which amounts to 30 million in Spotify’s case, then [X - 1] won’t send subscribers fleeing from the app; but [X - 1,000,000] might start an unnoticable trickle; and [X - 10,000,000] might start an exodus.

That dynamic is due to the elasticity of Spotify’s demand. Spotify has proven that its demand curve is both highly and increasingly inelastic thanks to its users’ increasing dependence on playlists. If you take that to the most cynical extreme (i.e. playlists are undifferentiated and perfectly substitutable among competing platforms), then personalization becomes the preeminent point of differentiation — in which case Spotify’s demand would be even more inelastic, since users’ sunk costs accrue as time passes.

My use of “sunk costs” there is deliberate, because it alludes to the aforementioned “incredibly persuasive hook [that Apple Music used] to rein-in consumers”. That gives you an idea of how sticky sunk costs are unto customer relationships.

I’d go as far as to say that if Warner Music hypothetically pulled its catalog (~15% marketshare) from Spotify, I genuinely don’t think I’d notice or care — as long as Spotify kept feeding me highly targeted tracks in my playlists. I got siphoned-off of Pandora and on to Spotify years ago because the latter let me curate my own playlists. Now, whether I’m commuting or entertaining, I always defer to playlists. I legitimately don’t have the time to curate my own tracks, and even if I had the time, Spotify knows me better than I know myself — especially considering the overwhelming amount of music to choose from.

But that’s anecdotal and highly subjective. So, as a more objective testament to the aforementioned demand inelasticity, Apple Music boasts 45 million songs — a significant 50% more than Spotify — but the effects of users switching are not manifest in Spotify’s user data, which has accelerated on an exponential curve amidst Apple Music’s gatecrashing the scene. (Tidal has even more, claiming 50 million in selection!) That’s the “empirical” part I mentioned at the top:

Finally, per Spotify’s F-1, their “Digital Distribution Agreements” with the major labels all mature in 2019, with the respective expiration dates laddered throughout the year: April (Universal), July (Sony), and August (Warner). If Universal were to walk in April 2019, then Sony and Warner would enjoy a big revenue bump almost immediately. That’s the aforementioned “prisoner’s dilemma”: If Universal were to pass on a grand bargain with Spotify in April 2019, then Sony and Warner would effectively get to divvy-up UMG’s revenue share on Day 1 ante bellum. Will Universal displace that lost revenue with incremental revenue gains from other platforms? They certainly won’t on Day 1. If Universal’s absence were to eventually trigger a user exodus from Spotify, UMG might start clawing-back up to its prior run-rate, but its competitors, Sony and Warner, would be ahead of the game — benefitting from all of the incremental royalties that Universal had ceded on Spotify while participating in lockstep with Universal everywhere else.

The question is not whether those royalty rate renegotiation dates are sufficiently laddered for Spotify’s benefit; the question is how sustainable that revenue bump would be for the remaining labels. Again, that comes down to the (in)elasticity of Spotify’s demand — specifically what minimum quantity and quality of content is required to keep Spotify’s convex demand curve beyond its price corner (i.e. in the inelastic portion).

#2: Without exclusivity, equity in artists doesn’t help Spotify signup new users

Second, Spotify’s equity in artists, sans exclusive rights to content, simply maximizes the opportunity's IRR. Yes, streaming video platforms maintained exclusive rights to their own original productions, but at the time, Netflix and Amazon Studios had other priorities: hedging against supply chain risk and monetizing their data assets. In such a way, equity-without-exclusivity not only benefits Spotify’s bottom line, but it also creates a moat for the core business.

The difference in exclusive rights between music and movies is partially due to the nature of each medium. You listen to the same song repeatedly, but you only watch the same movie once or twice. So, of course, the music industry wants to get paid-per-play and the movie industry wants a fixed licensing fee. Therefore, music platforms are predicated on abundance — maximizing impressions via reach — whereas movie streaming services are predicated on scarcity — maximizing revenue-per-impression via exclusivity.

By definition, it almost always follows that abundant content is commoditized and scarce is differentiated. Accordingly, given a business model predicated on abundance, this music industry’s content can not be as differentiated as conventional wisdom once thought it was. After all, Tidal was probably the most differentiated music streaming app, thanks to the scarcity it tried to engender via exclusive releases, yet its subscriber numbers topped-out around a mere 4.5M vs Spotify’s 70M! (In fact, amidst recent fraud allegations against the app, researchers have suggested that Tidal subs might have been as low as 1M.) Given Tidal’s underwhelming success, the most educated guess anyone can make today is that songs are not extremely differentiated — qualitatively nor quantitatively — and exclusives are not strong enough of a value proposition. You need something else!

While there’s plenty of reason for Spotify to turn-down exclusive rights, why would Spotify actively opt-in to non-exclusive arrangements? Well, Spotify [allegedly] has a meaningful information advantage, so it stands to reason that they’d have an unusually high hit-rate and ROI as a seed-stage investor in nascent artists. For Spotify, these home-grown musicians would be a hedge against incumbent labels — not to mention the best use of Spotify’s capital.

The ROI of a widely-distributed artist is worth much more than the ROI of an exclusive artist. Non-exclusivity would allow Spotify to effectively levy a tax on revenues throughout the music industry, both on and off its own platform, from pay-per-play royalties to other revenue streams like concerts and merchandise. That far exceeds the LTV of incremental subscribers wrought from exclusive perks.

With that in mind, read the following comment made by Spotify CEO Dan Ek’s on the company’s Q1 earnings call:

“…we do think that there is huge inefficiencies in the way that [artists] are being taken to market today and the amount of money that labels and the whole ecosystem have to invest in creating viable artists. Because Spotify already sits on the data, sits on consumers, sit on the preferences, we think we can play a huge role in connecting more artists with more fans and thereby obviously capture a big share of that too. So we are excited about the area.” (I had this highlighted and saved thanks to Annotote)

The history of modern music proves that labels can make or break stars by brute force, because discovery has always been one of the biggest variables predicating stardom. “Discovery” once meant shelf-space at a record store and airtime on a radio station — all of which labels heavily influenced. Today, “discovery” means inclusion in a Spotify playlist. So, not only does Spotify have agency in picking winners and losers, but it also has data that explain the other variables predicating stardom.

Given all of that, Ek’s parlay in the excerpt above seems to be his offering Spotify’s kingmaker services to labels. Those who accept will win marketshare; those who dissent will suffer at the hands of the playlist; and Spotify can legitimately attribute dissenters’ demise to “huge inefficiencies” that could’ve been optimized had they accepted Spotify’s cutting-edge insights. In the meantime, Spotify can build its own portfolio of grassroots artists — perhaps a combination of solo investments and co-investments alongside cooperative labels. And, if you’re a Spotify user, you’re going to hear these nascent stars before everyone else — even without Spotify having exclusive distribution rights — because Spotify will have identified, signed, and promoted these Next Big Things before anyone else.

#3 and #4: The Netflix playbook doesn’t apply

Let’s delve right into a direct comparison of Netflix and Spotify…

Businesses are built around access to some sort of scarcity. Super-simplistically, Facebook monetizes access to finite attention; Facebook users grant it their finite attention due to its superior user experience — specifically its network effects.

Similarly, by the time Netflix got around to monetizing access to streaming, that solution was highly valued by a handful of early adopters due to its superior user experience vs linear TV. But, eventually, streaming got commoditized by new entrants who had all procured the same catalogs, so Netflix moved-the-goalposts again by producing its own originals. That not only re-introduced scarcity to its product, but also maintained a critical mass of attention such that 3rd party suppliers couldn’t leave.

Netflix could’ve sat on its hands and done nothing, hoping that inertia would keep its userbase paying month-after-month; or Netflix could’ve gone out and tried to compete on the basis of selection, hoping studios would cooperate in letting it aggregate all of their content. Ultimately, Netflix chose a third option — one which they could control, rather than one that they couldn’t. That resulted in Netflix Originals, the success of which was as highly likely as it could have been, given Netflix’s unique data assets.

This gets around to the reason why Spotify could succeed as a seed-stage investor in nascent artists. While it certainly could continue to enjoy the status quo, Spotify would be far more secure in a future it can control, rather than one it cannot.

Today, the songs themselves are no longer the scarcity that Spotify was once monetizing access to; songs are now a commodity available on a number of other alternatives. The competitive field has caught up to Spotify — much like Netflix at T=1. Compare the companies’ strikingly similar marketshare and competitive landscapes:

Also, compare the consolidated supply chains from which each has had to procure its content:

While that all amounts to Netflix and Spotify having a lot in common, their differences actually strengthen the case for Spotify launching a label…

I’ve already discussed how consumer preference is changing and listeners have far less need for access to the entire back-catalog — unlike MVOD subscribers. Statistically, a full 99% of songs that are streamed come from a mere 10% of the total catalog!

Another stark contrast to Netflix’s subs is the fact that “most music listeners only subscribe to one app” actually helps Spotify, who at this point in the game has its critical mass of subscribers (and now its free tier) locked-in due to accumulated usage data. There are those “sunk costs” again.

Taken together, those two differences provide even more evidence as to the resilience of Spotify’s demand.

Insurmountable network effects

Having secured their turf in their respective quadrants, along with the lionshare of industry usage, Apple Music and Spotify are now “re-bundling” their services, so to speak, creeping into the playlist territory occupied by their respective counterparts:

That’s one way for Spotify to monetize access to its own superior user experience — a positive feedback loop much like that achieved by other supermassive aggregators.

Sure, Pandora could wake-up³ and try to defend its turf against Spotify’s attack, but it’s probably too late, since Spotify has reached the flow-state known as “network effects” — one of the most implacable forces in modern business.

During the Cambridge Analytica mess earlier this year, it became even more clear that Google and Facebook’s dominance is predicated by their superior user experiences, not their superior data. Their user experiences — not their data — start the virtuous cycle of network effects that attract users (demand), webpages (supply), and advertisers (payors). Data is just one of the byproducts spun-off from those information transactions.

As seen with Google open-sourcing datasets or Facebook trading data with 3rd parties, competitors can’t rival the duopoly even were they given equal data assets, because Google and Facebook already have an insurmountable scale advantage that makes the opportunity costs of any constituent switching to rival platforms too large — whether that be users, websites, or advertisers seeking alternatives. So, even if everyone were to have the same data for targeting — perfect competition on that plane — social media’s incumbents would still have more attention. And it appears that Spotify, with its industry-leading 70M subscribers, has reached that echelon.

While playlists are explicitly the vehicle toward Spotify’s future, the business has reached a crossroads where it has to decide what kind of a platform it wants to be: Leverage its network effects toward either proprietary means (a record-label-cum-VC) or 3rd party ends (an intelligence backbone for incumbent labels). It appears that “Ek’s parlay” is to start with the latter, then pivot to “The AngelList of Music” approach to the former, if necessary.

Herein, I’ve merely affirmed the hypothesis that Spotify could launch a record-label-cum-VC — the AngelList of Music — without cannibalizing its core business.

Annotote is the most frictionless way to get informed and inform others. For all the knowledge you need, every time you read. Come leave your mark >>>

¹ For example, compare Powerhouse: The Untold Story of Hollywood’s Creative Artists Agency to Hit Men: Power Brokers and Fast Money Inside the Music Business.

² N.B. Unlike news media, the supply procured by these music streaming platforms — albeit abundant — is neither free nor infinitely replicable. Since aggregators need to license most albums and tracks from record labels, among other factors, the music industry isn’t subject to the same zero barriers-to-entry conditions as the rest of digital media. And, as with all media, highly differentiated dragon kings do exist among musicians — the kind of creators who are standalone destinations unto themselves — such that they warrant DTC relationships. While they do not change the ~normal distribution of artists in aggregate (i.e. Taylor Swift falls pretty far out on the right tail), they technically are not suited for disintermediation at the hands of aggregators over the long term. For example, the inelasticity of such seasoned musicians’ rabid fanbases give such artists wholesale transfer pricing power (WTPP) that allows them to make up for any marginal unit volume (listeners) they may lose by dissenting from platforms like Spotify (or record labels) with higher unit prices fetched by going direct-to-consumer (or independent). These exceptions-to-the-rule don’t really affect Spotify, for reasons discussed above (e.g. “consumer demand isn’t binary or linear; it’s nuanced and convex”), but Spotify could offer a powerful partnership for such go-it-alone artists (i.e. providing much-needed services for independent musicians per the “AngelList of Music” auspices).

³ It’s worth mentioning that the weakest competitive positions on this chart are the quadrants that Amazon and Spotify occupy. For Amazon Music, depth of selection is inferior to personalization when the end product is playlists. For Spotify, personalization is inferior to selection when the value proposition is a la carte. Ideally, a business would want to occupy the strategic moat on the diagonal between Apple Music and Pandora. But, as discussed above, Spotify was able to thrive on that low-ground (and now lay siege on the high-ground) because of Pandora’s singular focus on its technology with almost complete disregard for its business — particularly its product-market fit.

⁴ The dates on these graphics differ wildly, but I wanted to show two charts that were easiest for the eye to compare. The point is not to quibble over marginal percentage points, but rather to note the supply consolidation among very few firms. If anyone can find better graphics, by all means reply herein.

{kind=link}