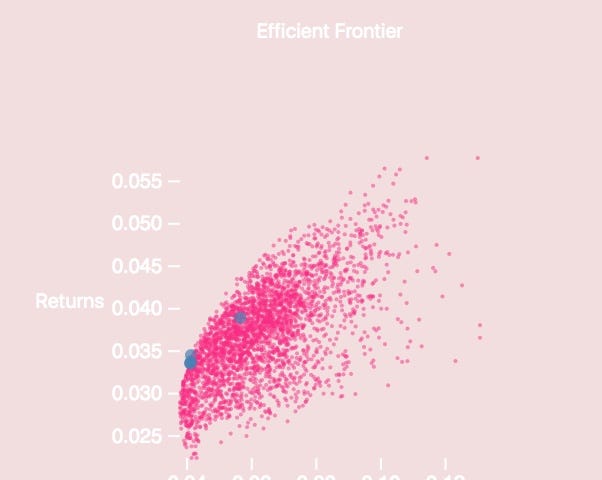

Expected Shortfall in Python

[Post is also available at quaintitative.com]

Google VAR and you will find lots of criticisms on VAR as a measure of market risk. And you will inevitably see Expected Shortfall (ES) being put forward as an alternative.

These were the top 10 stories published by quaintitative in 2018. You can also dive into monthly archives for 2018 by using the calendar at the top of this page.