Rethinking policies to remove secrecy

Putting the IFF agenda into action at the country level. Part 7 of 9

Illicit financial flows (IFF) became an international concern in the late 2000s and are now an established policy concern in the development context. Still, policymakers have yet to address important questions about putting anti-IFF programmes into practice. This seventh blog post discusses secrecy and alternatives to advance anti-IFF policies to remove secrecy.

Other posts in this series

- IFF definitions–crucial questions

- IFF: What losses for international development?

- IFF and country level legitimacy

- The blind spots in anti-IFF strategies

- Strategies for effective anti-IFF efforts

- Coordinating an attack on secrecy

- This post:Rethinking policies to remove secrecy

- Expanding the role of corruption in IFF

- Country-level IFF research for counter-IFF support

Fredrik Eriksson is a lawyer with extensive experience from private sector research, policy analysis, evaluations, strategy development, and consultancy work — mostly on anti-corruption and governance issues. He leads the U4 Innovation Lab and private sector research.

The solution of sorts

Efforts to implement integrity standards in the international financial system have so far not shown great results. This is clear from Financial Action Task Force evaluations of how states and industry-actors implement the formally required framework. We need to rethink how to best remove secrecy.

Other ways of measuring secrecy with a larger scope, such as the Financial Secrecy Index, expose considerable problems with secrecy in advanced countries like Switzerland and the United States (Findley et al.). Improving transparency in these nations is not a matter of technical capacity, or limited access to financial resources to govern. It is primarily a matter of whether there is a political interest or not to remove it. So how can we understand that lack of progress and interest in removing secrecy? In light of the persistent presence of secrecy, are there any plausible alternatives?

The fundamental idea is that transparency will make it more difficult to enjoy the proceeds of illegal acts.

As discussed in previous posts in this series (see IFF definitions–crucial questions and The blind spots in anti-IFF strategies), the main focus of anti-IFF policies is to remove secrecy with relevance for cross-border transactions of funds. The fundamental idea is that transparency will make it more difficult to enjoy the proceeds of illegal acts — as preventive measures will be able to stop international transactions. Examples are:

— National corporate registries requiring identification of beneficial owners of corporations.

—Due diligence required by financial institutions and other designated actors when accepting customers.

— Requirements to control the origins of funds to be transferred.

When prevention fails, having good transparency as regards actors behind cross-border flows will help law enforcement go after the responsible culprits.

Thwarting secrecy could be easier and more cost effective in reducing crime levels and illegal acts than trying to prevent them in the first place.

If the idea is effective, thwarting secrecy could be easier and more cost effective in reducing crime levels and illegal acts than trying to prevent them in the first place. The idea is based on the assumption that much illegal activity leading to IFF is motivated by gaining economic returns. Conversely, when illegal acts result in little or no material benefit, fewer may be motivated to engage in illegal activities.

Definitions and disruptions

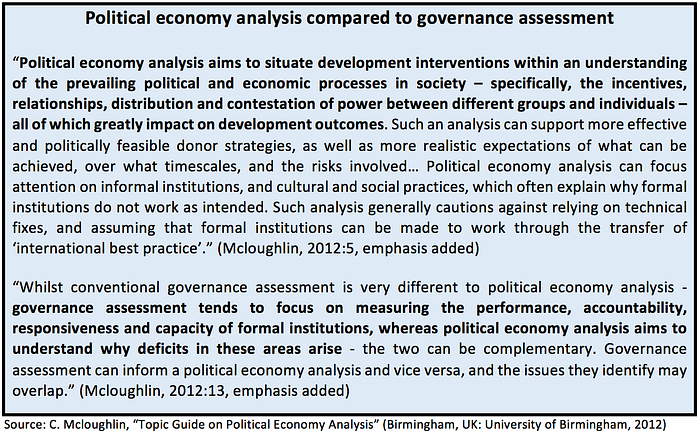

We need a few definitions and premises to analyse the lack of progress against secrecy relevant for IFF, and explore plausible alternative approaches. In this series, I have continuously referred to the political economy of various reforms: who benefits from maintaining status quo and how are those actors connected to the political system at the concerned governance levels. Knowing that global progress in removing secrecy has been slow, it makes sense to consider this connection as a possible explanation for weak progress. The box below clarifies what is meant by political economy analysis and how it compares to a governance assessment.

When we analysed the two dominant definitions of IFF (see IFF definitions—crucial questions), it became clear that anti-IFF measures can relate to a chain of events, i.e. the “IFF chain.” Although the analysed definitions offer no clarity, what eventually qualifies a cross-border flow of money as IFF depends on what parts the IFF chain consists of, and what parts of that chain that need to be illegal according to the definition used.

Anti-IFF measures can relate to a chain of events, i.e. the “IFF chain.”

Looking at the IFF chain, the type of transfer indicates that not all cross-border transfers are the focus of IFF. Only cross-border money transfers are relevant value transfers — not the contracts, goods, or services — whether legal or not. The source of funds refers to illegal and legal acts that generate money, which eventually will be transferred across a border, or that is used for payment of a loan of some kind that has already been transferred as money across a border. The cross-border transfer mechanism concerns the illegal or legal means to make that cross-border transfer happen. Finally, in some IFF definitions, whether the transferred funds are used for illegal activities can also define a cross-border transfer as IFF.

Regardless of what current IFF policies advocate, based on current IFF definitions, we can consider that IFF may be disrupted by measures targeted at:

- Reducing illegal acts (incl. criminal acts) as a source of funds

Current anti-IFF measures:

—Reduce international tax evasion and international bribery through prevention and law enforcement.

— Recovery of “stolen assets”, i.e. funds of criminal origins involved in cross-border transfers. - Reduce illegal acts (incl. criminal acts) that use funds transferred across borders

No current anti-IFF measures exist. - Making it more difficult to make cross-border transfers of money generated from illegal acts, via legal transfer mechanisms

Current anti-IFF measures:

— Anti-money laundering (AML) regimes through implementing the FAFT Recommendations. - Make cross-border transfers using illegal transfer mechanism more difficult

Current anti-IFF measures:

— Potentially stop or make hawala/IVTS transfer systems more transparent, see IFF definitions–crucial questions.

How does secrecy relate to these options for disruption?

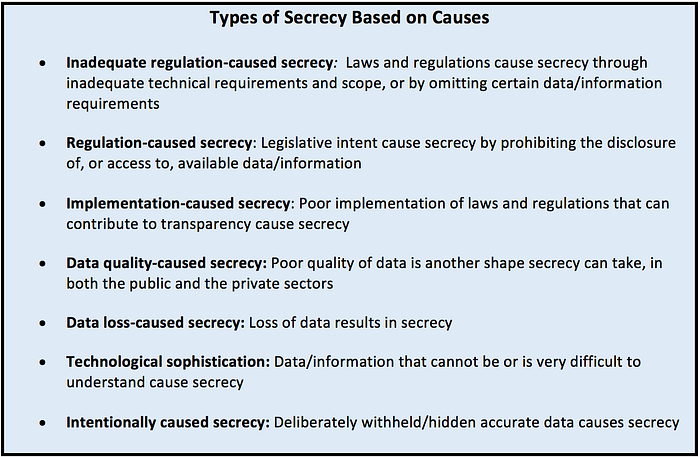

Types of secrecy

Secrecy can take many different shapes. Through greater disaggregation, it is easier to see how secrecy relates to IFF and the various reasons that give cause to it. The following types of secrecy offer a non-exhaustive illustration of various types based on their causes:

Reasons for secrecy

Inadequate regulation

The explanatory reasons behind the various causes are not always obvious. Starting with secrecy caused by inadequate regulation, this can for example be explained by a lack of technical capacity in government or parliament. It may also be explained by having become obsolete due to social and technological change, or deliberately created or maintained as inadequate to satisfy certain interests—including illegal or morally ambiguous ones. The latter would imply representation of such interests within the political sphere, preventing improvement (Reuter; Gilman).

Regulations

Looking at regulation-caused secrecy, we can find secrecy relating to the legal and medical professions, intended to protect the interests of individuals and corporations in having their legal rights defended and realised. This type of secrecy also contains bank secrecy or corporations for which no owner needs to be registered (bearer share companies). Such secrecy may be motivated by a need to protect personal integrity, as well as more dishonest reasons. But there are also politically pragmatic considerations too.

Not all countries can compete with the same attractive factors for various reasons.

In the previous post, we discussed secrecy as an incentive to attract international capital flows (Braun and Weichenrieder; Johannesen and Zucman; Hanlon et al.; Bloningen et al.). In competitive international markets for FDI and private portfolio investments, not all countries can compete with the same attractive factors for various reasons (World Bank, 2018; Carter). While there are several ways to explain how (through what mechanism) various policies spread internationally, competition for global capital has the most pronounced effect (Simmons et al.; Gilardi). The competition for global capital is also a far more powerful motive than trade, while the existence of global norms have a limited effect on how policies spread (Simmons and Elkins). Another mechanism by which policies spread is by learning from a country’s sociocultural peers, reflecting governments’ search for appropriate models for economic policy (Simmons and Elkins). In other words, the spread of secrecy could be explained by understanding secrecy as a means to attract global capital and as an appropriate economic policy if sociocultural peers use it.

Implementation

Implementation-caused secrecy may be explained by a lack of implementation regulations, capacity (resources and the degree of professionalisation of bureaucratic staff) and autonomy of regulators to comply with laws and regulations, or to implement them effectively (Fukuyama). One such missing capacity can concern weak integrity, which may facilitate the buying of secrecy through bribery when needed. However, for developing countries, there are more compelling explanations that have to do with the actual governance regime type (see Strategies for effective anti-IFF efforts) in a country (North et al., 2012; Mungiu-Pippidi).

Where the rule of law is not yet established, governance follows different norms that exist in parallel to the formal rules.

Although capacities and resources surely are scarce, where the rule of law has not yet been established, governance follows different norms that exist in parallel to the formal rules (Andrews et al.; Hadfield and Weingast; Grindle; Unsworth; World Bank, 2017). Person-based rules emanating from patrons dominate over impersonal formal rules, contrary to the rule of law. Secrecy is a consequence of such governance rules, which are not fixed, universally applicable, published and publicly accessible. Ineffective and inconsistent application of non-transparent informal rules as well as of transparent formal rules causes secrecy. Where regulation falters and norms of transparency cannot be upheld, knock-on effects on regulated subjects should be expected. This situation appears to be the most serious problem for the anti-IFF policies seeking to establish disruptions of IFF through effective governance based on formal rules.

Adopting transparent formal regulations likely has no effect on secrecy-levels in places where secrecy exists because power-holders only implement regulations in their own interest. It is possible that the weak results of the implementation of the FATF Recommendations to remove secrecy in financial systems is directly related to this.

Data quality

The reasons behind secrecy caused by poor data quality may be found in that it is incomplete, incomprehensible, based on poor assessment, biased judgment, or representing something else than intended. There are many instruments that seek to remedy this problem, such as laws on bookkeeping, external audits and public financial management (PFM). At international level, there are also bodies that establish international standards for data such as the United Nations Statistical Division (UNSD), International Organisation for Standardisation (ISO), International Labour Organisation (ILO) or World Health Organisation (WHO) (Hancock). Various professional standards equally establish qualitative requirements that seek to address the risk of inadequate data quality. The International Financial Reporting Standards (IFRS) have been issued by the International Accounting Standards Board (IASB) stating how particular types of transactions and other events should be reflected in financial statements. There are also the Generally Accepted Accounting Principles (GAAP), which refers to a set of rules, standards and practices used in the accounting industry for preparing and standardising financial statements issued outside a company. The goal of the IFRS is to provide good information, whereas the standards offer guidelines on achieving that goal.

Data quality is a primary concern in the attempts to prevent the misuse of corporate vehicles for criminal or illegal purposes.

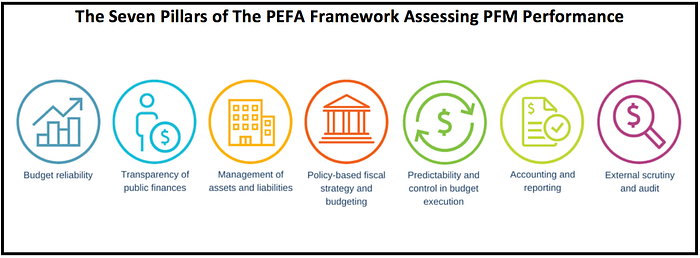

Data quality and transparency are also primary concerns in the PEFA framework. PEFA is a methodology for assessing the extent to which PFM systems, processes and institutions contribute to the achievement of desirable public budget outcomes. PEFA identifies seven pillars of performance that are essential to achieving such outcomes. The seven pillars thereby define the key elements of a PFM system, which are assessed in relation to specified standards. Where data quality-caused secrecy exists, it is easy to see how it facilitates IFF.

Whereas data quality standards are not a common policy component of anti-IFF policies (see The blind spots in anti-IFF strategies), data quality is a primary concern in the attempts to prevent the misuse of companies for criminal or illegal purposes. The demand for corporate registries that are able to register the beneficial owners of companies depends on reliable data (van der Does de Willebois et al.). Data in such registries that is incomplete, incomprehensible, or represent someone else causes secrecy. Also, if identification documents contain such poor data that they are easy to forge, or to claim to be someone else, the consequence is secrecy.

Data loss

The vulnerability of technology is another reason that explains secrecy caused by data loss. As more and more data is digitised, the threats against data and the integrity of data are also increasing. In the developing world, we still see much data contained in paper folders, sometimes piled in corridors vulnerable to physical misplacement, flooding, mold, fire, rodents and theft. Globally, not all governments will have the same capacities to protect data, resulting in secrecy.

Technological sophistication

Technological development and sophistication is a well known reason for secrecy. Compare the difference between having data that cannot be understood and data that does not exist. For the purpose of transparency, there is no immediate utility beyond the existence of data, unless it can be understood. Examples where technological sophistication may cause secrecy is advanced software coding, new financial innovations that bundle or distribute risks using advanced risk assessment models, or some technical specifications that few people understand.

Other times, it can be a multitude of reasons converging that explain the causes of secrecy. For example, new social movements that question state authority in response to austerity policies may converge with technological progress resulting in increasing secrecy. EUROPOL recently voiced its concerns over “[a]lternative cryptocurrencies with anonymity as their core feature,” which “will make transactions practically untraceable, heavily facilitating the trade in illicit goods online” (EUROPOL, p. 27).

The secrecy that follows from technical sophistication make intellectual property rights suitable as an instrument for fraudulent transfers of funds across borders.

Secrecy caused by factors contributing to data loss as well as technical development and sophistication can facilitate IFF. Consider the payments for cross-border sales of intellectual property rights between companies that are part of a multi-national corporation (MNC). According to the arm’s length principle (see Article 9 of the OECD Model Tax Convention), a transfer price should be the same as if the two companies involved were two independent companies. But if the concerned intellectual property is very complex, it will be difficult for a tax authority to assess the contents of the right sold, and whether the price is therefore reasonable, a bad deal, or fraud intended to transfer profits. Of course, bespoke or unique intellectual property rights may not be possible to compare the price of, which makes it next to impossible to determine the arm’s length price. Consequently, the secrecy that follows from technical sophistication make it suitable as an instrument for fraudulent transfers of funds across borders.

Intention

Finally, we have the reason that is most commonly related to IFF, notably that corporations and individuals intentionally choose to not comply with formal requirements. That can be explained by these actors having criminal intent to evade taxation, to avoid getting caught, to ensure the enjoyment of the proceeds of crime, or any other reasons to seek secrecy. Another explanatory reason is directly related to implementation-caused secrecy: if there is general societal disregard of formal rules on transparency, why should we expect individuals to have an intention to comply? Doing so may inflict a high social cost at a personal level that few can afford.

Intentionally-caused secrecy is the main type of secrecy that the current anti-IFF policies aim at.

Regardless of the reasons for having an intention to not comply with formal transparency demands, intentionally-caused secrecy is the main type of secrecy that the current anti-IFF policies aim at. They do so by seeking to strengthen regulators like tax authorities, but also law enforcement and crime prevention by implementing AML regimes, enlisting the efforts of private sector actors (see The blind spots in anti-IFF strategies).

As the examples above suggest, all these types of secrecy can facilitate IFF along the various parts of the IFF chain. To address these various types of secrecy could—depending on what is contextually relevant — disrupt IFF. However, the current anti-IFF policies have a much more limited scope.

To improve the scope of anti-IFF policies at country level there are a range of assumptions that first need to be considered when chosing between reform options. For instance, there is little point in seeking to establish improved data quality when the more fundamental problem concerns a governance problem resulting in implementation-caused secrecy.

Assumptions for removing secrecy

When we wish to remove secrecy to prevent IFF, there are a number of assumptions made for how to do that. These provide valuable information about factors and dynamics to consider when choosing effective approaches for specific goals. In the case of removing secrecy to prevent IFF, at least eight assumptions are made:

- Behavioural change in a society can be achieved through the instrument of government.

- The government has the responsibility and capability of establishing various instruments that affect behavioural change, whether the behaviour is exceptional or part of communal social norms.

- Should the government not have that capability, it can and wants to acquire capacities needed.

- The government has interests aligned with establishing anti-IFF policies.

- Should the government not have such aligned interests, it is receptive to influence to eventually have that.

- The available means to influence such alignment are effective.

- The problem of secrecy in the international community is a collective action problem.

- Once there is alignment of interests, global collective action among nations against secrecy is possible and effective (see Coordinating an attack on secrecy).

The problem of secrecy in the international community is a collective action problem.

The question is then: What do these assumptions require of the solutions to be effective in removing secrecy? And are these assumptions correct?

Tricky bits

The assumptions of capability, interest alignment, receptiveness to influence and the means to influence will have different relevance in different countries. That is because countries have different governance regime types (see Strategies for effective anti-IFF efforts), but also because the relationship between secrecy types and the various components of governance regimes types is different (Fabre; Dick).

Where patronage is dominant, the rule of law takes a back seat relative to person-based rules.

Consider a developing state with systemic levels of corruption measured in relation to what the formal laws and regulations require. Where corruption is common, the rule of law cannot be strong. Equally, where patronage is dominant, the rule of law takes a back seat relative to person-based rules (see Strategies for effective anti-IFF efforts; North et al., 2009; Unsworth). In this context, capability is certainly an issue that needs addressing for secrecy to be removed. But there is also the question of interest alignment, which is directly linked to the nature of the political economy, i.e. the relationships between economic activities and the components (political and other) of the governance regime. Should the links to IFF-related economic activities be very strong, it is clear that there is also limited interest to remove it.

The next question is therefore if the government is receptive to influence, even if it has limited capability and interest to address secrecy. In the previous blog post, we discussed the possibility of identifying an inducement big enough to compensate for the cost of giving up secrecy, should alternative approaches fail. The idea is that it would offer a way forward to achieve interest alignment and thereby make international collective action by states effective, such as the non-binding FATF Recommendations to prevent abuse of the global financial system. But even if there is interest alignment, the incentives for effective collective action between nations are tricky to get right.

Even if there is interest alignment, the incentives for effective collective action between nations are tricky to get right.

Imagine a country in which the economy benefits from the provision of secrecy by attracting global capital. Collective action by countries to remove secrecy is based on the premise that all will eventually be better off by removing secrecy as a factor to compete for global capital. It is easy to see the harm caused by secrecy by facilitating illegal activities and the enjoyment of its proceeds. But if the main harm caused by secrecy is perceived to occur elsewhere, while bringing considerable flows of global capital to its own economy, the benefits of such collective action is not immediately apparent in economic terms. If countries can anticipate that the benefits of transparency will vary with the characteristics of the economies that participate, it may be difficult to get countries to commit. On an “even playing field” of factors that are acceptable to compete for FDI and private portfolio investments, nations that lack attractive attributes will lose out from the benefits of transparency (World Bank, 2018; Dick). The benefit from removing secrecy is therefore not equally distributed across the countries that are part of such collective action.

Another issue concerns the size of the potential benefit from transparency relative to the number of competitors for it. Once secrecy is removed through collective action among nations they all compete to attract the part of global capital that require transparency. The larger the group, the smaller the benefit from transparency (Olson). In other words, the strength of the commitment to transparency will differ considerably between countries (see IFF and country level legitimacy).

Once secrecy is removed through collective action among nations they all compete to attract the part of global capital that require transparency.

In the EU, collective action towards greater transparency has been improved with the introduction of Directive 2014/107/EU based on the 2014 Global OECD Standard for Automatic Exchange of Financial Account Information in Tax Matters. Its scope covers not only interest income, but also dividends and other types of capital income as well as required common due diligence procedures to be followed by financial institutions, while still excluding shadow banks (see The blind spots in anti-IFF strategies). The Directive requires that jurisdictions obtain information from their financial institutions and automatically exchange that information with other jurisdictions on an annual basis.

The EU has also made efforts to extend this standard to third countries, like Switzerland, Monaco and San Marino. Through those measures, the EU is actively engaging in a lead role for expanding the membership in the collective action against secrecy. At the same time, the EU is stepping up its intolerance of those who choose to not cooperate through the publication of its new blacklist of non-cooperative jurisdictions, including the promotion of “defensive measures” (sanctions) by its member states. While any blacklist issued by a political organisation will always suffer from weak credibility regarding impartial application of rules of qualification, its very existence is a clear signal of increasing intolerance.

The EU is actively engaging in a lead role for expanding the membership in the collective action against secrecy.

Nevertheless, the varying degrees of commitment to transparency between nations is a real concern. Previous experiences from seeking to address harmful secrecy through the OECD have been described as disappointing. The refusal by the USA to commit undermined effective collective action both against secrecy and harmful tax regimes (Sævold). The lack of genuine commitment was also evident from other nations that formed part of a collective action initiative against secrecy: “Every time a political opportunity arose, all states failed to deliver on their promises to amend their laws” (Sævold, p. 117, author’s translation). The fact that the world’s largest economy still has no interest to commit (Shaxon) indicates a need to consider whether the possibility of a global level playing field is utopian.

Perhaps all that can realistically be hoped for are groups of like-minded countries with regimes of varying degrees of transparency in financial transactions.

Given the status of global governance and the centrality of Westphalian sovereignty as a principle of international law, perhaps all that can realistically be hoped for are groups of like-minded countries with regimes of varying degrees of transparency in financial transactions (transparency + transactions = transpaction). As an incentive to comply with demands for greater transparency, such transpaction groups may choose to establish various security-motivated barriers to trade (Yeong Yoo and Ahn; WTO) and to the free flow of capital should transparency demands not be met. Assessing the assumptions concerning interest alignment, receptiveness to influence and the means to influence may indeed lead us there.

An economic perspective on secrecy

The issue of varying commitment to transparency has a direct impact on the assumptions concerning receptiveness and the means to influence. Transnational norm diffusion happens when decisions in one country are influenced by the international context. Examples of such influence concern ideas, norms, and policies displayed or even promoted by other countries and international organisations (Gilardi).

For norm diffusion to occur, emulation is a mechanism that explains how policies diffuse, together with coercion, competition and learning about alternative ideas, norms and policies and their consequences (Simmons et al.; Gilardi). Those are all mechanisms that describe how transparency may spread, but they do not explain when there is receptiveness to change through those mechanisms.

If economic competition for global capital is a strong mechanism for economic policy diffusion, it makes sense to think about secrecy from an economic perspective.

If economic competition for global capital is a strong mechanism for economic policy diffusion (Simmons et al.; Simmons and Elkins), it makes sense to think about secrecy from an economic perspective. As we are exploring receptiveness to influence, politics is a necessary consideration when looking at influencing factors for such receptiveness.

Geoeconomics is the “use of economic instruments to promote and defend national interests, and to produce beneficial geopolitical results; and the effects of other nations’ economic actions on a country’s geopolitical goals” (Blackwill and Harris, p. 20). The instruments used are trade policy, investment policy, economic sanctions, the cybersphere, aid, monetary policy, and energy and commodity policies. Many of these instruments are used transparently by nation states, but far from all (Dick; Blackwill and Harris). Some uses of these instruments add to the demand for secrecy, directly undermining the idea of a transparent global economy.

By looking at basic market dynamics, we may better understand when such receptiveness for policy change can be expected to occur.

That perspective brings us to the question of considering supply and demand for secrecy. By looking at basic market dynamics, we may better understand when such receptiveness for policy change can be expected to occur (McConnell et al.). If the supply of secrecy had no value, it would be easy to influence a government in favour of transparency as there is nothing to lose. But where there is a demand for secrecy, there are revenues to collect, which may have linkages to the components/actors of the governance regime. If a demand for secrecy is “elastic” it means that demand drops dramatically for even a small increase in the price for enjoying secrecy. However, if it is “inelastic”, the consumers of secrecy will keep “buying” the same amount of secrecy even if there are big increases in the price (Krugman and Wells).

Now consider the demand for secrecy. Is it elastic or inelastic? Given the real risk of losing freedom or economic assets, a suggestion is that it is inelastic. This has two immediate consequences. Firstly, even if it is possible to considerably increase the cost of using secrecy, it would probably not reduce the actual demand in terms of volume (Johannesen and Zucman). Secondly, a large increase in the price, following the partially reduced supply due to collective action against secrecy, means that the value of the remaining markets for secrecy increases.

A large increase in the price of secrecy, following the partially reduced supply due to collective action against secrecy, means that the value of the market for secrecy increases.

Subsequently, a partly successful removal of secrecy should produce some interesting results in relation to the compensation cost for removing secrecy (see Coordinating an attack on secrecy). If we compare before and after a partial reduction in secrecy, we would need to meet a substantially increased compensation cost for removing the secrecy that remains (inducement to influence) and make a country align with global collective action against secrecy. The increased value of the market for secrecy also creates a greater risk for defection from collective action should the return from transparency be limited.

In conclusion, given the difficulties of effective global collective action against secrecy (Marquette and Peiffer; Ostrom), to attack the supply of secrecy suggests that the value of the remaining markets for secrecy will increase. For that reason, to remove the supply of secrecy with relevance for cross-border financial transactions alone appears ineffective. If the demand for secrecy is inelastic, addressing the activities that create the demand, on the other hand, can theoretically reduce both the volume of flows that depend on secrecy as well as the value of the markets for secrecy.

Conclusion

That brings us back to the initial questions asked: how can we understand the lack of progress against secrecy and are there any plausible alternatives?

It appears that the current anti-IFF approach to remove secrecy by focusing on the supply-side is ineffective.

As this review has suggested, removing secrecy that facilitates IFF is complex. The types of secrecy that are relevant differ from context to context and so do the reasons that explain its persistence. Greater transparency in the reasons behind the various types of secrecy will provide valuable knowledge of how to prioritise any efforts to remove it. Being clear about the assumptions for how secrecy can be removed sheds light on the realism of the current anti-IFF policies to be effective in removing the different types of secrecy. Furthermore, greater clarity in relation to the factors and dynamics that explain why some countries maintain secrecy is valuable to develop better approaches. From that perspective, it appears that the current anti-IFF approach to remove secrecy by focusing on the supply-side is ineffective. Instead, seeking to address the activities that create the demand for secrecy can theoretically reduce both the volume of flows that depend on secrecy as well as the value of the markets for secrecy.

EU’s Forest Law Enforcement and Trade programme achieves interest alignment – combining economic incentives for governments and those actors they depend on.

For future policy improvements, and in line with the demand-side thinking, an interesting policy instrument is the model of the EU’s Forest Law Enforcement, Governance and Trade action plan (FLEGT). The model consists of having the EU as a large market to assist partner states in developing their timber tracking and licensing systems, as well as improving their governance capacity. Producers and traders that qualify for a so called “FLEGT license” can access the EU markets, which creates a strong economic incentive to attain that license. The approach is specifically constructed to align with WTO rules, which allows for consensual non-tariff barriers between countries (Iben et al.).

By combining economic incentives for governments and those actors they depend on, FLEGT achieves interest alignment while overcoming the difficulty of precision in targeted economic sanctions (Kaempfer and Lowenberg). Furthermore, through bespoke and co-creative approaches to overcome the relevant types of secrecy at country level, this model could be a considerable improvement to the current anti-IFF policies. It aligns with the idea of having groups of like-minded countries striving for common transparency ideals (transpaction groups), while making use of various security-motivated or other non-tarriff based barriers to trade and the free flow of capital as an incentive to comply. Through its unique collective action compliance mechanism for EU member states (Tallberg), the EU is well placed to lead this type of “economic inducement policy for transparency” while seeking to advance its transparency agenda.

Other posts in this series

- IFF definitions–crucial questions

- IFF: What losses for international development?

- IFF and country level legitimacy

- The blind spots in anti-IFF strategies

- Strategies for effective anti-IFF efforts

- Coordinating an attack on secrecy

- This post:Rethinking policies to remove secrecy

- Expanding the role of corruption in IFF

- Country-level IFF research for counter-IFF support

References

Andrews, M.; Pritchett, L. and Woolcock, M., “Escaping Capability Traps through Problem-Driven Iterative Adaptation (PDIA)” CGD Working Paper 299 (Washington: Center for Global Development, 2012)

Blonigen, B.; Oldensky, L. and Sly, N.,“The differential effects of bilateral tax treaties,” American Economic Journal: Economic Policy 6, no. 2 (2014): 1–18

Braun, J. and Weichenrieder, A. J., “Does Exchange of Information between Tax Authorities Influence Multinationals’ Use of Tax Havens?,” Discussion Paper no. 15 (ZEW — Centre for European Economic Research, 2015)

Carter, P., “Why do Development Finance Institutions use offshore financial centres?,” Report, October (London: ODI, 2017)

Dick, H. “The Shadow Economy: Markets, Crime and the State” in Wilson, E. (ed.), Government of the Shadows: Parapolitics and Criminal Sovereignty (London: Pluto Press, 2009): 97–116

EUROPOL. “Exploring tomorrow’s organised crime” (Brussels: EUROPOL, 2015)

Fabre, G. “Prospering from Crime: Money Laundering and Financial Crises” in Wilson, E. (ed.), Government of the Shadows: Parapolitics and Criminal Sovereignty (London: Pluto Press, 2009): 90–96

Findley, M.G.; Nielson, D.L. and Sharman, J.C., Global Shell Games: Experiments in Transnational Relations, Crime and Terrorism (Cambridge: Cambridge University Press, 2014)

Fukuyama, F. “What Is Governance?.” CGD Working Paper 314 (Washington, DC: Center for Global Development, 2013)

Gilardi, F. “Transnational diffusion: Norms, ideas, and policies” in Walter Carlsnaes, W., Risse, T. and B. Simmons (eds) (2012), Handbook of International Relations, (Thousand Oaks: SAGE, 2012): 453–477

Gilman, N. “The Twin Insurgencies: Plutocrats and Criminals Challenge the Westphalian State” in Matfess, T. and M. Mikaucic (eds.), Beyond Convergence: World Without Order (Washington: Center for Complex Operations, 2016)

Grindle, M.S., Jobs for the Boys: Patronage and the State in Comparative Perspective (Cambridge, M.A.: Harvard University Press, 2012)

Hadfield, G.K. and Weingast, B.R., “Microfoundations of the Rule of Law” Annual Review of Political Science; Stanford Law and Economics Olin Working Paper, no. 453 (2013)

Hancock, A. “The Role of International Standards for National Statistical Offices.” ESA/ST A T/AC.267/8 (New York: United Nations Department of Economic and Social Affairs Statistics Division)

Hanlon, M.; Maydew, E. L. and Thornock, J. R., “Taking the Long Way Home: U.S. Tax Evasion and Offshore Investments in U.S. Equity and Debt Markets,” The Journal of Finance 70, no. 1 (2015): 257–287

Iben, N.; Pilegaard Hansen, C.; Cashore, B.“Timber legality verification in practice: Prospects for support and institutionalization.” Forest Policy and Economics 48 (2014): 1–5

Johannesen, N. and Zucman, G., “The end of bank secrecy? An evaluation of the G20 tax haven crackdown,” American Economic Journal: Economic Policy 6, no. 1 (2014): 65–91

Kaemper, W.H. and Lowenberg, A.D., “The Political Economy of Economic Sanctions,” in Handbook of Defense Economics. Volume 2. Sandler, T. and Hartley, K. (eds.) (Amsterdam, Netherlands: Elsevier B.V., 2007)

Krugman, P. and Wells, R. Microeconomics. Fourth edition. (New york, NY: Worth Publishers, 2015)

Marquette, H. and Peiffer, C., “Corruption and Collective Action,”Developmental Leadership Programme Research Paper. (Birmingham, UK: University of Birmingham, 2015)

McConnell, C.R.; Brue, S.L. and Flynn, S.M. Economics: Principles, Problems, and Policies. 21st edition (New York: McGraw-Hill, 2017)

Mcloughlin, C., “Topic Guide on Political Economy Analysis” (Birmingham, UK: University of Birmingham, 2012)

Mungiu-Pippidi, A., The Quest for Good Governance: How Societies Develop Control of Corruption (Cambridge, UK: Cambridge University Press, 2015)

North, D.; Wallis, J.; Webb, S. and Weingast, B. (eds). In the Shadow of Violence: The Problem of Development for Limited Access Order Societies (Cambridge: Cambridge University Press, 2012)

North, D.; Wallis, J. and Weingast, B. Violence and Social Order (New York: Cambridge University Press, 2009)

Olson. M. The Logic of Collective Action (New York: Shocken Books, 1965)

Ostrom, E., Governing the Commons: The Evolution of Institutions for Collective Action (Cambridge, UK: Cambridge University Press, 1990)

Reuter, P., Draining Development? Controlling Flows of Illicit Funds from Developing Countries (Washington, DC: World Bank, 2012)

Sævold, K. “En skattepolitisk konfrontasjon med skatteparadiser.” Masteravhandling (Bergen: UIB, 2012)

Shaxon, N. “Loophole USA: the vortex-shaped hole in global financial transparency.” TJN website (Chesham, UK: TJN, 2017)

Simmons, B. A.; Dobbin, F. and Garrett, G., The Global Diffusion of Markets and Democracy (New York: Cambridge University Press, 2008)

Simmons, B. A.; Elkins, Z. “The globalization of liberalization: policy diffusion in the international political economy,” American Political Science Review 98, no. 1 (2004): 171–189

Tallberg, J. “Paths to Compliance: Enforcement, Management, and the European Union.” International Organization 56, no. 3 (2002): 609–643

Unsworth, S., An Upside Down View of Governance (Brighton: IDS, 2010)

van der Does de Willebois, E., Halter, E. M., Harrison, R. A.; Park, J. W. and J. C. Sharman, The Puppet Masters -How the Corrupt User Legal Structures to Hide Stolen Assets and What to Do About It (Washington, D.C.: The World Bank, 2011).

World Bank, World Development Report 2017: Governance and the Law (Washington, DC: World Bank, 2017)

World Bank, Global Investment Competitiveness Report 2017/2018: Foreign Investor Perspectives and Policy Implications (Washington, DC: World Bank, 2018)

WTO. “Article XXI -Security Exceptions.” WTO website (Geneva: WTO, 2017)

Yeong Yoo, J. and Ahn, D., “Security Exceptions in the WTO System: Bridge or Bottle-Neck for Trade and Security?” Journal of International Economic Law 19, no. 2 (2016): 417–444

About U4

The U4 Anti-Corruption Resource Centre at CMI works to identify and communicate informed approaches to partners for reducing the harmful impact of corruption on sustainable and inclusive development.

Follow us

Disclaimer

All views expressed in this post are those of the author(s), and do not necessarily reflect the opinions of the U4 partner agencies, or CMI/U4.