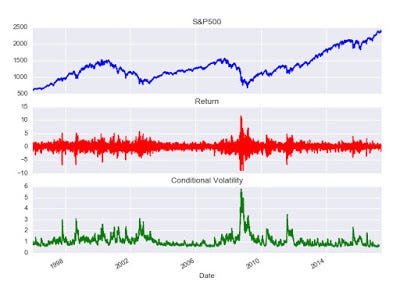

Volatility Modeling Using GARCH

Generalized Autoregressive Conditionally Heteroskedastic (GARCH) เป็นอีกโมเดล ที่ใช้ในงาน time series…

These were the top 10 stories published by cw-quantlab in October of 2018. You can also dive into daily archives for October of 2018 by using the calendar at the top of this page.