RSR Analysis Sunday — Edition 22

Opportunity for RSV in Crypto & RSR Valuation

Happy Monday Rangers! And sorry, I know it’s not Sunday. It’s Monday. But it took a while to piece together this week’s analysis comparing the market opportunity for RSV as it relates to the dominant stable coins in the crypto ecosystem, and what that means for RSR. We are also closing May today, after a tumultuous month and tenuous recovery. But June is looking up, and the general market structure is still bullish. Stack RSR while it’s still cheap, and read up on the adoption taking place in Venezuela. As always, feedback is welcome — enjoy!

We’ve discussed many times about the adoption potential of RSV, Reserve’s stable coin solution. A recent Reddit post does a great job explaining how RSV will be used by real world people, not just crypto people.

So the “beachhead” if you will, for Reserve, is to begin by driving real life use cases. As an ERC-20 stable coin, however, it can be used by “real” people, but also by “crypto” people.

The stable coin space is still in its infancy, but in total constitutes over $100B in value across the crypto ecosystem.

You can use stable coins to trade, and earn yield, and move between fiat and crypto rails (in some cases).

This takes us to two big questions:

- What does the business model look like for existing stable coins?

- What is the opportunity for a newcomer like RSV?

The Big Four (Stablecoins)

There are many stable coins, but as most power law distributions go, there is one big one, another smaller one, and another one that is smaller still. Then there are whole bunch of others. For the sake of simplicity, we’ll focus on USD stable coins, and the four biggest ones within that category.

The four that probably matter most in crypto today are:

- Tether, or USDT, issued by Bitfinex

- USD Coin, or USDC, issued by Circle

- Binance USD, or BUSD, issued by Binance

- Dai, or DAI, issued by the MakerDAO Foundation (multi-collateral DAI)

These are also the largest, in terms of market capitalization, which is a close proxy for the total issuance.

You can see how small other stable coins are in comparison:

And how significant these four stable coins are to the overall crypto ecosystem — comprising 95% of the entire market. We’ll come back to this table in a bit.

But first — let’s dig a little deeper on each of these. How they started, why they exist, and how they make money.

Bitfinex’s Tether

The stable coin everyone loves to hate, since 2015. Tether was the first predominant stable coin, and naturally has faced countless FUD since its inception. Fractional reserve FUD, bitcoin price manipulation FUD, regulatory FUD, and much more. It’s still the most prolific and most often used stable coin in the crypto ecosystem though, with many pairs on many exchanges. Despite a serious lack of trust (anyone remember “Bitfinex’ed”?) it is still predominant and a cornerstone of crypto, with over $60B in circulation.

Essentially, the model is similar to USDC and BUSD — you can deposit dollars from your old bank account with the friendly folks at Bitfinex, and in exchange you get shiny new USDT. Then you go YOLO them at memecoins or whatever.

Of course, Bitfinex charges 10 basis points (0.10%) on deposits for the luxury of converting dollars to USDT.

So, what does Bitfinex do once it has your dollars? In short, they invest it to generate a return for themselves.

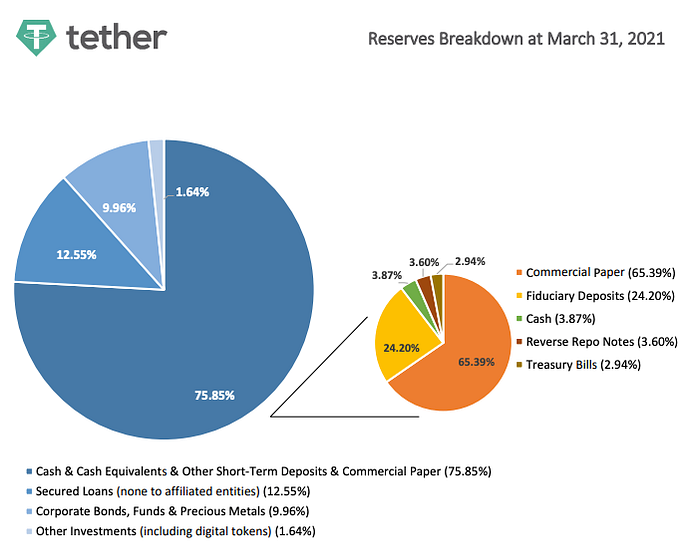

And, lucky for us, they recently gave us some insights via a pie chart. They also publish a “transparency update”.

So why not just keep the dollars they get…in dollars? Well, the entire business model is based on putting those dollars to work, just like most financial institutions.

Typically, a “risk-free” rate is defined as the 10 year Treasury Bond, issued and backed by the friendly and always liquid US Government. These don’t pay much, call it 1.5% annually. This is considered a highly liquid and safe instrument. So the least they should make on every $1B on deposit is around 1.5% of that, or $15M. Not a bad business model.

But they want more. Which is why you see things like “commercial paper” comprising [75.85%*65.39%] of their assets under management (AUM). In other words, your USDT is earning the Bitfinex team a commercial paper rate (usually high-ish quality debt — think select municipal bonds, or AAA-rated corporate bonds) on about half of the deposits. Probably in the 4–6% range, but potentially higher, for every $500M of each $1B on deposit. Even better business model.

Circle’s USD Coin

Circle began in 2018, and employs a similar business model to Tether. Its real claim to fame is the fact that you can buy USDC with your Coinbase account and swap between fiat USD at a 1:1 rate, making it an increasingly popular option in the US. The Circle team is also more trust-and-compliance focused than Tether, enabling them to gain share over the past several years to nearly a quarter of the overall market.

Circle offers a suite of options for utilizing USDC, and recently raised $440M to expand its services. In the stable coin game, distribution is key, and Circle is doing a good job getting their token into the market and building trust as it expands its deposits with financial institutions and integrations with Signature Bank and the Visa network, among others.

They offer attestation reports from auditor Grant-Thornton, LLP. While they don’t disclose exactly how the dollars are re-invested, it is safe to assume they employ a similar but perhaps slightly more risk-averse strategy to Tether when generating income from reserves. At a mid-range between the 1.5% “risk-free” rate and a more aggressive rate, assuming 3.5%, they would be earning $35M annually from each $1B on deposit. Again, not a bad business model at all.

Binance’s …Binance USD

Think of it like Eurodollars…but through Binance, I guess. BUSD uses Paxos as its custodial provider, and again in a similar way to USDT and USDC enables easier fiat-to-crypto swaps. This is essentially a white-labeled stable coin, that has grown primarily due to Binance’s dominance in the exchange space. Paxos manages the attestations for both their own stable coins, PAX and PAXG, as well as for BUSD. I assume there is a revenue sharing agreement in place (undisclosed) but it is safe to say Binance and Paxos also employ similar models to both Tether and Circle when it comes to making money on user deposits.

MakerDAO’s Dai

Reserve has a great article written about MakerDAO’s Dai stable coin, so I encourage you to read it. I’ll keep the initial explanation short.

Essentially, users can deposit various forms of collateral into the MKR platform, and receive DAI like they would USDC or USDT. If their collateral falls below a certain threshold, the collateral is liquidated in order to maintain the peg of 1 DAI per 1 USD. Fees are generated on the platform through normal usage, which are accrued and used to buyback and burn MKR. This is similar in a broad way to the approach that Reserve will take with RSR (think MKR) and RSV (think DAI).

Multi-collateral DAI is becoming more reliant on USDC as recent market volatility presses its debt ceiling (essentially a cap on profits for MKR holders) higher and higher. The community proposal can be found here, with a summary below:

Sort of scary right? The largest decentralized stable coin…is using USDC as a primary collateral type (to be fair, there are not that many options for stable underlying collateral, but still). So if you’re a MKR holder, you must also be wondering…how do I make the most money on this…if Circle is already making money on USDC? And DAI doesn’t have established fiat rails, so new entrants to the DAI ecosystem are (essentially) limited to the crypto and DeFi-savvy.

In terms of business model, the burn mechanism is transparent, as we’ve come to expect in DeFi, which makes it easy to see where earnings are landing as a % of DAI. MKR trades at a forward P/E of ~20, based on the profit generated and used to burn MKR tokens (or essentially redistribute as revenue via buybacks to holders of MKR). This puts the earnings rate on DAI “under management” at around 3–3.5%.

Let’s Bring It All Together

USDT, USDC, BUSD, DAI

So, we’ve got $100B in stable coin assets, slushing around the crypto sphere today. Back-and-forth between TradFi and DeFi. What does it all mean? What does it mean for Reserve? Let’s see if we can make some projections:

The table on the left should look familiar from earlier. The table on the right adds in our assumptions on yield based on the outstanding market cap for each stable coin we reviewed, bolded for the section most likely based on our assessment. ~6% for USDT, 3.5% for the rest. You can see we get fairly close with our assumption on DAI, given we can more or less backtest since we know the profit projections of $144M; the 3.5% level is pretty close. Again, not a bad business model. Based on this analysis, between $3B and $6B in revenue is generated by the top four stable coins.

P.S. — If you have other data sources to add, please let me know — would love to continue to refine and tweak these assumptions.

RSV & RSR

Key assumptions

- 3.5% is a reasonable rate of return on a stable coin asset

- 10 to 50 forward Price/Earnings (PE) ratio is reasonable

- RSV can reasonably take between 5% and 25% of the overall stable coin market for a crypto-centric audience — this part is key

Note: when calculating RSR Market Cap at % Share, we only use Base returns (bolded). Other scenarios (Bear/Bull/Wild) are shown as a reference.

You can see below that we provide a range for both PE and % Share. For example, at a PE of 20 and a market share of 10%, RSR market cap should be in the $7.2B range if we use our base return rate of 3.5%. At a PE of 30 and a share of 15%, the market cap for RSR would be $16.2B (again, at a 3.5% annual return rate).

These are healthy and reasonable valuations. Given the drawbacks outlined above for the dominant stable coins in the market, RSV will have a strong competitive advantage, especially vs. USDT and DAI. Therefore a 5% — 15% take should be achievable. Note: this analysis is conservative, in that it assumes the overall stable coin market stays flat at $100B — which is not reasonable, as it should continue to grow steadily, however we can save overall growth of the pie assumptions for a future analysis.

BUT WAIT, THERE’S MORE!

This table is ONLY FOR THE CRYPTO MARKETS. Remember how Reserve is building real products, for real people? Well, the product will work in our crypto bubble too. And Reserve is hiring someone specifically to work on growing share of RSV, from zero to 5% to 25% and beyond. The distribution mechanism for USDT is crypto investors, and they had first mover advantage, but lack trust. For Circle, USDC uses Coinbase and institutions. BUSD uses Binance. For DAI, the distribution mechanism is niche DeFi. For RSV, the distribution mechanism can be ALL of these, as well as users in countries fighting hyperinflation. To build a comprehensive model of the potential market cap of RSV (and therefore potential of RSR) we need to add the “crypto” opportunity with the “real world” opportunity. More on this in future articles, but suffice to say, the opportunity is massive, even if you focus on the opportunity to build a better decentralized stable coin in the existing crypto market landscape.

Technical Analysis — Week of May 31st

Monthly Timeframe — USDT Pair

The May 2021 close will be above January at $0.035, still generally constructive and bullish, though as mentioned last week will need at least several weeks to recover from the recent purge. I still remain optimistic for our longer-term targets (gray and orange are Delphi Digital’s targets for each given year, less bullish than my own predictions in blue).

Weekly Timeframe — USDT Pair

Nice bounce this past week from lows — I do expect us to return to the general trend, however the blue long term channel was broken on the weekly, so will need time to recover. If the prior ~75% retrace from ATH in March 2020 is to be believed a repeat, then we have a roughly 20x from here in the coming 12–15 months, which would mark us around the $0.70 level, well within our predictions for end of year from January 2021. So bullish in general construction, though again I am not rushing to add to a position…yet.

Daily Timeframe — USDT Pair

We can see a reversal beginning to take shape, with strong resistance at $0.030. MACD crossover will be bullish, and set us up for a strong June. However, adding to positions over the next week or two slowly to cost average lower is still advised, as the market in general is crabbing sideways and up. I’m looking for daily closures over $0.05 to confirm a rebound; but these prices are so good that I can’t imagine they’ll last long.

Daily Timeframe — BTC Pair

The 115 and 130 levels are significant for RSR/BTC pair; unfortunately the break below Channel 1 shown below will need another week or two to recover, in a similar vein as above. I do think we will form a nice structure around the100 sats level that will serve as a base for moving higher as crypto markets find their footing in June.

Previous Editions of RSR Analysis Sunday

Edition 21 — May 23rd, 2021

The Humbling

Edition 20 — May 16th, 2021

Monday is Confirmed

Edition 19 — May 9th, 2021

Reserve is Building Real Products, Used by Real People

Edition 18 — May 2nd, 2021

The Future is DAO

Edition 17 — April 25th, 2021

The Age of Crypto

Edition 16 — April 18th, 2021

What the FUD? | Thoughts on RSV

Edition 15 — April 11th, 2021

Reserve & Network Valuations

Edition 14 — April 4th, 2021

Reserve, Bitcoin, & Time Scarcity

Edición Especial de Abril — April 1st, 2021

FruityChain Implementation

Edition 13 — March 28th, 2021

Successes from Marzo (App Rollout)

Edition 12 — March 21st, 2021

Scaling The Team & The Importance of User Experience

Edition 11 — March 14th, 2021

Reserve Adoption — It’s Happening

Edition 10 — March 7th, 2021

Welcome to Medium

February 2021

All Reports from February (originally shared in Telegram)

January 2021

All Reports from January (originally shared in Telegram)

DISCLAIMER: “RSR Analysis Sunday” is for entertainment and informational purposes only and is not meant to be construed as financial advice of any kind. All investments carry risks.

“RSR Analysis Sunday” is not endorsed or supported by the Reserve Team, or any of its affiliates.